Bank of Maharashtra Q1 FY27 Results: PAT up 27%, Steady Guidance for FY27

Solid guidance for FY27 after strong performance in Q1 FY27. Strong execution against FY27 guidance by MAHABANK. Premium valuations for a public sector bank

1. Public Sector Bank

bankofmaharashtra.bank.in | NSE: MAHABANK

Products & Services

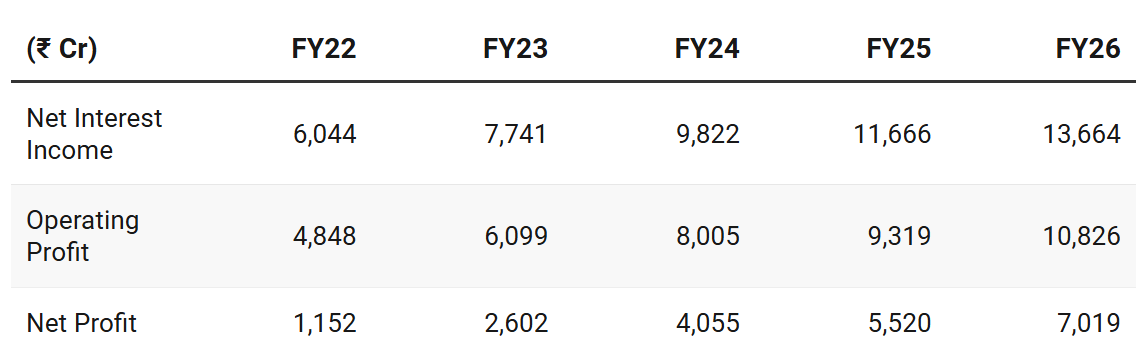

2. FY22-26: PAT CAGR of 57% & Net Interest Income CAGR of 23%

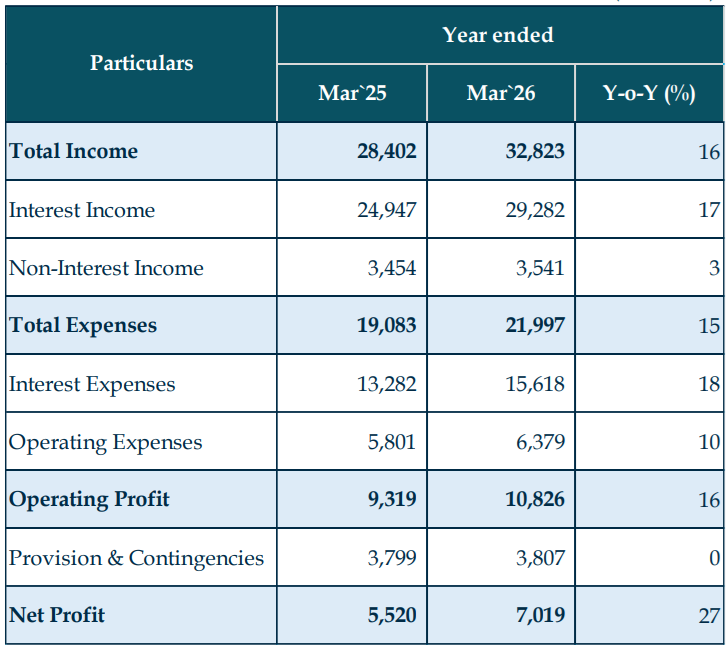

3. FY 26: PAT up 27% & Net Interest Income up 17% YoY

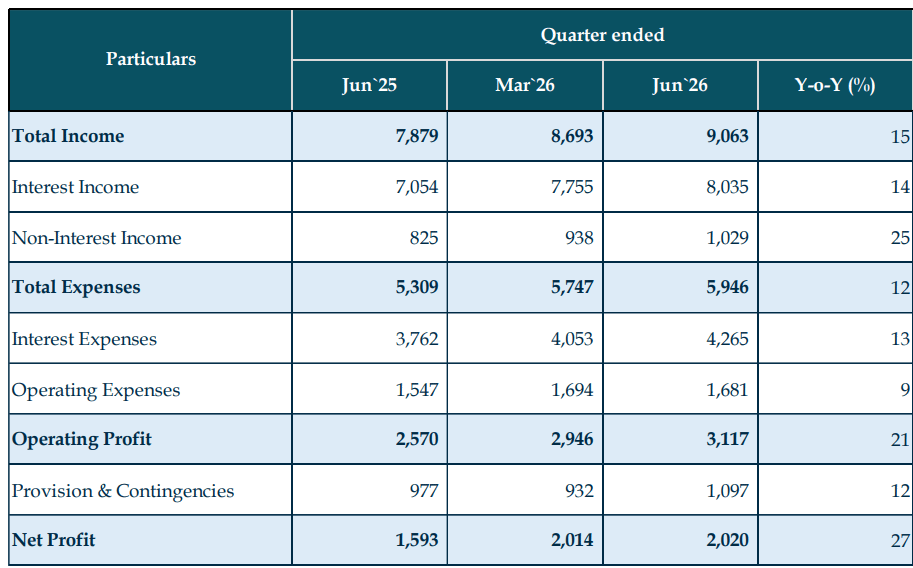

4. Q4-26: PAT up 27% & Net Interest Income up 15% YoY

PAT & Net Interest Income flat QoQ

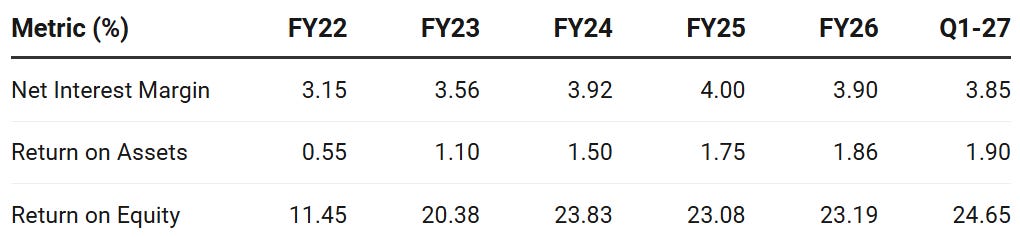

5. Business Metrics: Strong & Improving Ratios

6. Outlook: 15% NII growth

6.1 Management Guidance

Optimistic yet cautious outlook — Emphasizing profitable growth with zero compromise on asset quality rather than mindlessly chasing top-line expansion.

Growth and Profitability Targets

Loan Growth: Despite 27% year-on-year advances growth in Q1 — not to revise initial full-year loan growth guidance at 18%

Net Interest Income (NII): Committed to guidance of 15% NII growth.

Net Interest Margin (NIM):

NIM guidance is set at 3.75%, though bank outperformed Q1 with 3.85%

Expects yields on advances to potentially go up

53% their loan book is repo-linked and they have recently approved MCLR hikes, both of which will benefit the bank during upcoming interest resets.

Asset Quality and Strict Underwriting

NPA Guidance: Gross NPA below 2% and Net NPA below 0.25%.

Credit Cost: below 1%

Underwriting Benchmarks: Halting lending to individuals with a TransUnion CIBIL score below 681. All recent sanctions strictly within the prime and super-prime categories.

Operational Expansion and Capital Strategy

Cost-to-Income Ratio: below 40%

Branch Expansion: Aggressively expand physical footprint by opening 200 new branches annually

Capital Raising: To fund double-digit credit growth — to raise up to ₹5,000 crores in equity

Waiting on government approval

Intends to execute this raise at an opportune time during FY27

Deposit Strategy and Outlook

Resource Mobilization: Structural shift of retail funds from banking deposits to alternative assets like mutual funds and SIPs

Avoiding reliance on high-cost bulk deposits.

Leaning heavily on refinance options (which carry a blended cost of 6% to 6.5% and have no CRR/SLR requirements) to fund credit growth while protecting profit margins.

Upcoming Catalysts: Maharashtra Debt Waiver Scheme Expects a government agricultural debt waiver scheme to materialize within FY27, which could provide a major boost to the bank.

Out of an eligible portfolio of ~₹3,500 Cr, the maximum expected haircut to the bank is ~₹450-500 Cr.

Potential loss is heavily buffered, as the bank already holds ₹1,700 Cr in provisions and has a ₹1,100 Cr technical write-off (TWO) book against these accounts.

As a result, recoveries from this scheme will incrementally boost operating profits,

Government’s incentive of ₹50,000 for prompt-paying farmers is expected to bring a significant influx of savings account (CASA) balances into the bank.

7.FY26 Performance vs FY26 Guidance

Q1 FY27 largely outperformed the full-year guidance targets

Slight miss on NII, deposit growth and CASA ratio

Areas of Out-performance (Beating Guidance)

Advances Growth: Grew by 26.90% vs guidance of 18%.

Total Business Growth: Grew by 19.10% vs guidance of 16-17%.

Net Interest Margin (NIM): 3.85% exceeding the guidance of 3.75%

Return on Assets (ROA): 1.90% beating the targeted 1.80%

Return on Equity (ROE): 24.65%, well above the target of 20% or more.

Asset Quality:

Gross NPA fell to 1.45% and Net NPA to 0.13%.

Both beat the guidance of keeping GNPA below 2% and NNPA below 0.25%

Efficiency (Cost-to-Income Ratio): 35.04%, vs guidance of below 40%

Capital Adequacy (CRAR): 18.64%, vs the 18% target

Provision Coverage Ratio (PCR): 98.55% vs the 98% guidance.

Areas Where Guidance Was Met

Credit Cost: At 0.99%, line with the guidance of keeping it below 1%.

RAM vs. Corporate Ratio: At 63:37, in line with guidance of a 60:40 (+/- 2%).

Areas of Slight Underperformance (Missing Guidance)

Deposit Growth: 12.93% vs the guidance of 14-15%.

Attributed to avoiding high-cost bulk deposits and Certificates of Deposit (CDs) to protect margins, opting for cheaper refinance alternatives instead.

CASA Ratio: 48.51% below the target of ~50%

Net Interest Income (NII) Growth: Grew by 14.53%, lagging the target of 15%

8. Valuation Analysis

8.1 Valuation Snapshot — Bank of Maharashtra

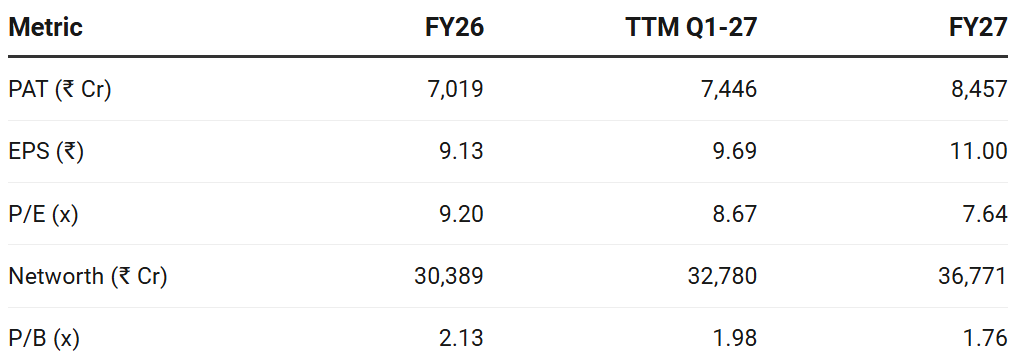

Current Market Price — ₹84

Market cap — ₹64,865.7 Cr

Not extremely cheap on P/B because the stock already trades around ~2× book, but it is still reasonable on FY27 P/B if the bank can grow deliver on 15% NII growth and profitability supported by

Valuations are entering Private bank territory.

MAHABANK is trading at premium valuations compared to other public sector banks.

The premium valuations are justified given its preformance relate to its peer

8.2 Opportunity at Current Valuation

NIM’s guidance is conservative — Profitability could surprise

The guidance is conservative on profitability, NIM, ROA, ROE and asset-quality ratios. It is less conservative on deposit growth, CASA retention, fee income growth and slippage control.

Corporate PipelineStrong — providing growth visibility

Undisbursed corporate sanction pipeline of roughly ₹34,500 crore, ensuring high visibility for continued double-digit corporate credit growth.

Upcoming Catalyst: Maharashtra Debt Waiver Scheme A major near-term upside lies in the anticipated Maharashtra state agricultural debt waiver scheme.

Recoveries from this scheme will directly and incrementally boost operating profits.

The government scheme also includes a ₹50,000 incentive for prompt-paying farmers, which will be credited directly to their savings accounts. The bank estimates this will bring a massive influx of low-cost CASA (Current Account Savings Account) deposits—calculated at roughly ₹775 crores—into the bank.

8.3 Risk at Current Valuation

Premium Valuations — Similar to top private sector banks

Raises the bar of performance for MAHABANK. Valuations now demand significantly superior performance compare to its public sector peers

Macroeconomic and Geopolitical Headwinds — West Asia crisis is a significant risk.

Bank took a proactive and prudent step by creating a specific “global geopolitical uncertainties provision” of ₹200 crores in Q4 FY26.

MAHABANK warned that the fallout of these geopolitical shocks could begin impacting the loan book in subsequent quarters.

The “War for Deposits” and Funding Constraints

Management acknowledges an “irreversible” structural shift where household savings are moving away from traditional bank deposits into alternative asset classes like mutual funds and SIPs.

Elevated CD Ratio: Because of this deposit squeeze, the bank’s deposit growth (12.93%) significantly lagged its stellar credit growth (26.90%) in Q1 FY27. This mismatch pushed the Domestic Credit-Deposit (CD) Ratio to an elevated 86.58%.

Declining CASA Ratio: The bank’s CASA ratio dropped from 52.51% at the end of FY26 to 48.51% in Q1 FY27.

Reliance on Refinance: To fund loan growth while avoiding expensive bulk deposits, the bank is relying heavily on alternative refinance options (utilizing roughly ₹19,000 crores).

If these refinance avenues become more expensive or dry up, the bank could struggle to fund its aggressive credit expansion without sacrificing profit margins.

Pockets of Asset Quality Stress

Agriculture NPAs: The Gross NPA in the agriculture portfolio remains notably higher than the rest of the book, standing at 7.58% in Q1 FY27.

MSME & SMA Bumps: In Q1 FY27, Gross NPAs in the micro, small, and medium enterprise (MSME) segments saw a slight quarter-on-quarter increase.

Equity Dilution

Shareholder approvals to raise up to ₹5,000 crores in equity.

Impending capital raise leads to near-term equity dilution for existing shareholders.

Guidance execution

Can MAHABANK grow advances at ~18%, maintain CASA near 50%, keep NIM around 3.75%, and still keep slippages below 1%?

That is the core risk investors should track.

Previous coverage of MAHABANK

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer