Bank of Maharashtra FY26 Results: PAT up 27%, Steady Guidance for FY27

Solid guidance for FY27 after out-performance in FY26 with ROA and NIM above guidance. Strong execution against FY26 guidance. Valuations leaves room for re-rating.

1. Public Sector Bank

bankofmaharashtra.bank.in | NSE: MAHABANK

Products & Services

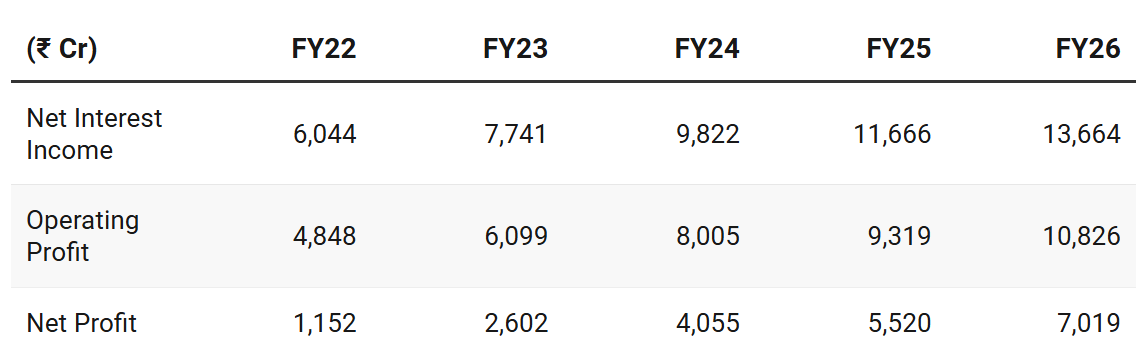

2. FY22-26: PAT CAGR of 57% & Net Interest Income CAGR of 23%

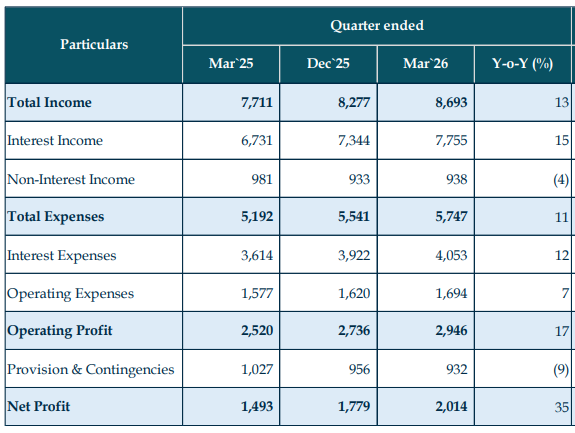

3. Q4-26: PAT up 35% & Net Interest Income up 19% YoY

PAT up 13% & Net Interest Income up 8% QoQ

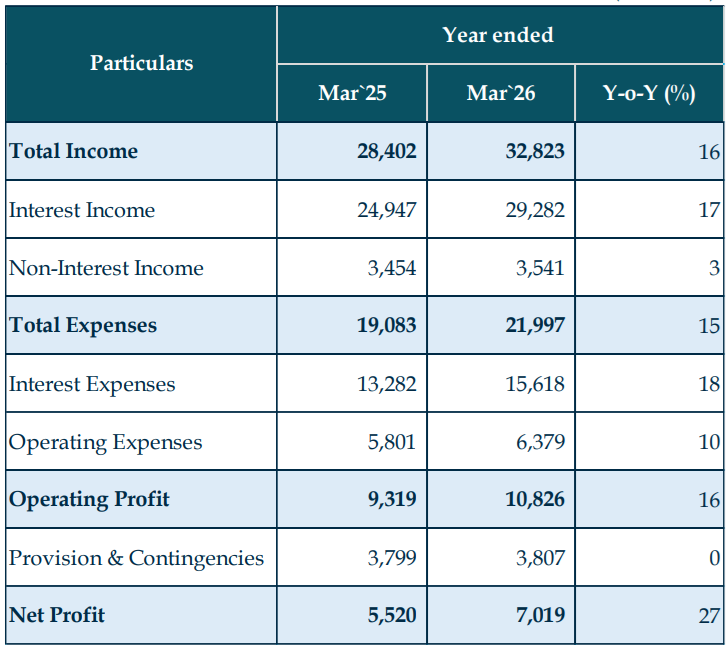

4. FY 26: PAT up 27% & Net Interest Income up 17% YoY

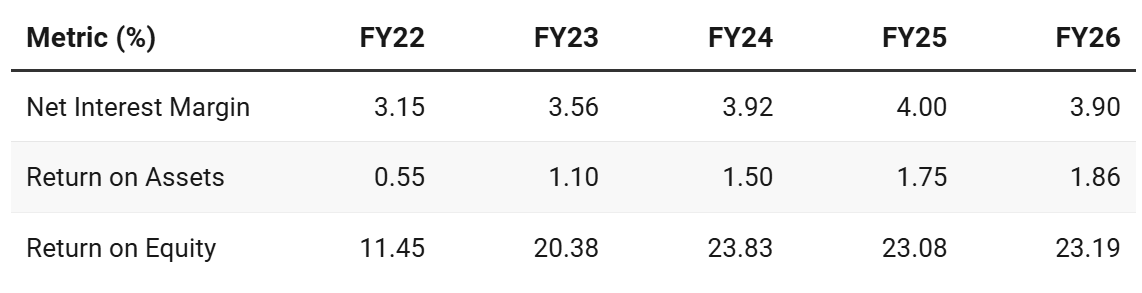

5. Business metrics: Strong Return ratios

For a bank, the real valuation driver is not just profit growth. It is ROA and ROE durability.

FY27 Guidance:

We have said that guidance for this year ROA will be 1.80.

ROE, while we did 23% plus for this year, we want to maintain a guidance of 20% and more

6. Outlook: Mid-teen growth

6.1 Management Guidance

FY27 is a continuation of FY26 guidance. Even though MAHABANK did better than FY26 guidance, the FY27 guidance was not raised. Overall the FY27 guidance looks conservative against FY26 performance

So total business this year, we plan to grow at 16% to 17%, within which

Advances will grow at 18%

Deposit to grow at 14% to 15%.

CASA, we will maintain around 50%.

RAM book will be growing at 18%.

RAM corporate, the ratio 60-40 plus/minus 2%.

Net interest income is to grow at 15%.

NIM, the guidance for this year is 3.75%.

Non-interest portion to grow at 10%.

Cost to income, we will continue to maintain as last year, below 40%.

ROA, we want to keep a guidance of 1.80%.

ROE, while we did 23% plus for this year, we want to maintain a guidance of 20% and more.

GNPA will remain within 2%.

NNPA within 0.25%.

Slippage will be maintained below 1%, and credit cost will be around 1%.

PCR at 98%

CRAR to be maintained at 18%.

7.FY26 Performance vs FY26 Guidance

Most of the ratios are now among the top 3 in the industry.

In terms of profitability, asset quality, we rank in position 1, 2, 3 on the critical ratios when we compare ourselves with the industry.

So we would like to not go down on a single ratio.

So the mantra for growth was it should be a growth, but it should be a profitable growth — Then there is no compromise on the quality.

Outperforming FY26 Guidance

NIM — Outperformed — 3.9% vs 3.75 guidance

ROA — Outperformed — 1.86% vs 1.75 guidance

Advances Growth — Outperformed — 21.74% vs 17 guidance

Deposit Growth — Outperformed — 14.14% vs 14 guidance

Cost-to-Income — Outperformed — 37.08 vs below 40 guidance

Credit Cost —Outperformed — 0.97 vs below 1 guidance

GNPA — Outperformed — 1.45% vs below 2 guidance

CASA — On-track — 50+ vs above 50 guidance

CRAR — Below — 18.36 vs about 18 guidance

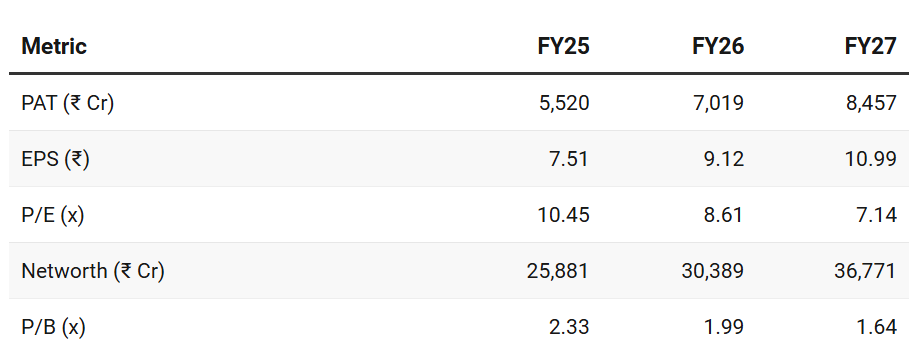

8. Valuation Analysis

8.1 Valuation Snapshot — Bank of Maharashtra

Current Market Price — ₹78.5

Market cap — ₹60,328.5 Cr

That is not extremely cheap on P/B because the stock already trades around ~2× book, but it is still reasonable on FY27 P/B if the bank can grow profit in double digits.

Guidance in-place for Net interest income growth of 15%.

FY27E = 7.1× P/E & 1.6× P/B

If FY27 guidance is delivered, there is scope for multiple re-rating based on FY26E numbers:

P/B of ~2× (if the business of performance of FY26 continues into FY27)

This would imply valuation upside without requiring redefinition of fundamentals.

8.2 Opportunity at Current Valuation

NIM’s guidance is conservative — Profitability could surprise

The guidance is conservative on profitability, NIM, ROA, ROE and asset-quality ratios. It is less conservative on deposit growth, CASA retention, fee income growth and slippage control.

This guidance looks deliberately set up to be achievable. Management is likely building in buffers for:

NIM moderation,

deposit competition,

West Asia / crude / currency risks,

possible MSME stress, and

normalisation after a very strong FY26.

Optionality from Re-rating

If current metrics hold, P/B could re-rate to ~2×+ in Fy27.

Re-rating does not require exceptional performance — continuity of FY26 into FY27

Limited Downside

Valuations are not demanding — provide protection against a weak quarter

8.3 Risk at Current Valuation

Geopolitical risk can hit MSME and corporate borrowers

MAHABANK has made some additional provisions regarding geopolitical risk. One needs to keep a watch how the situation evolves in Q1

So we call it global geopolitical uncertainties provision INR200 crores to begin with in this quarter, I have created.

Deposit mobilisation risk

MAHABANK itself referred to a “real war for deposits.”

Loan growth at 18% is guided higher than deposit growth of 14-15%. If deposits become expensive or CASA falls, NIM can come under pressure. For a bank growing advances at 18%, deposit quality matters as much as loan growth.

Guidance execution

Can MAHABANK grow advances at ~18%, maintain CASA near 50%, keep NIM around 3.75%, and still keep slippages below 1%?

That is the core risk investors should track.

Previous coverage of MAHABANK

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer