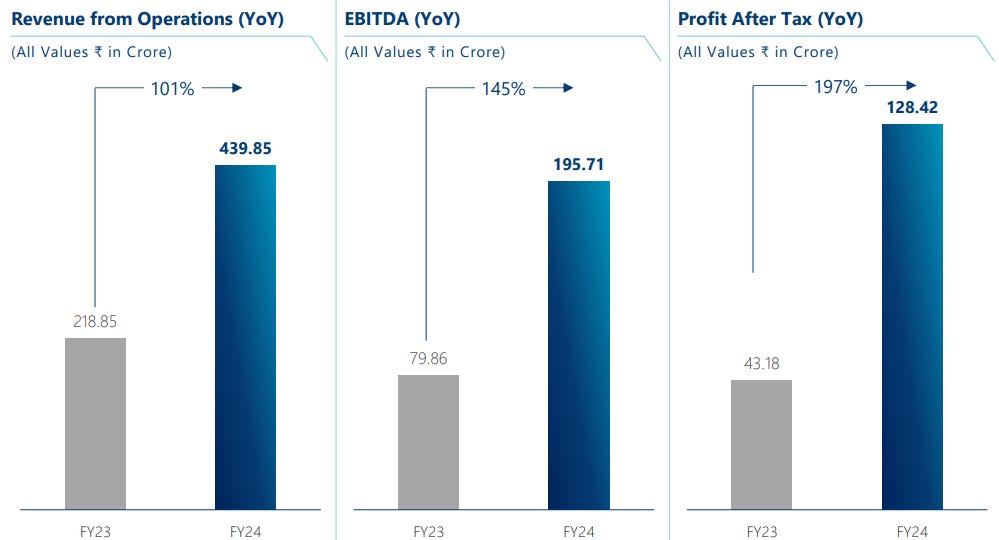

Zen Technologies: PAT growth of 197% & Revenue growth of 101% in FY24 at PE of 67

100%+ growth in FY25 supported by a strong order book. Revenue CAGR for FY25-27 at 50% to drive revenue to Rs 2,000 cr by FY27. Guiding for EBITDA & PAT margin of 35% & 25% respectively

1. Defence training & anti-drone solutions provider

zentechnologies.com |NSE: ZENTEC

2. FY20-24: PAT CAGR of 22% and Revenue CAGR of 31%

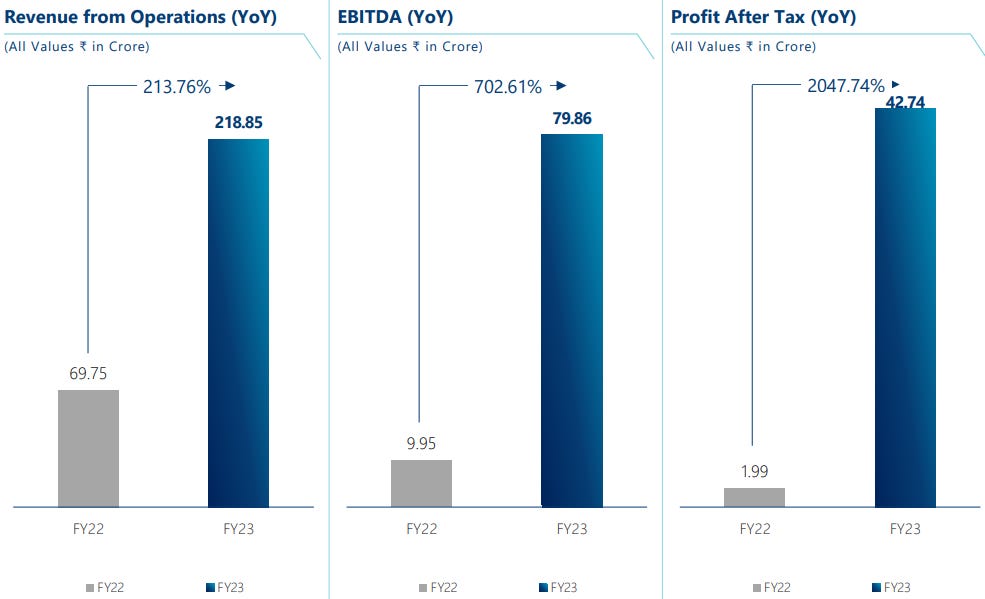

3. FY23: PAT up 2048% & Revenue up 214%

4. Strong 9M-24: PAT up 247% & Revenue up 143% YoY

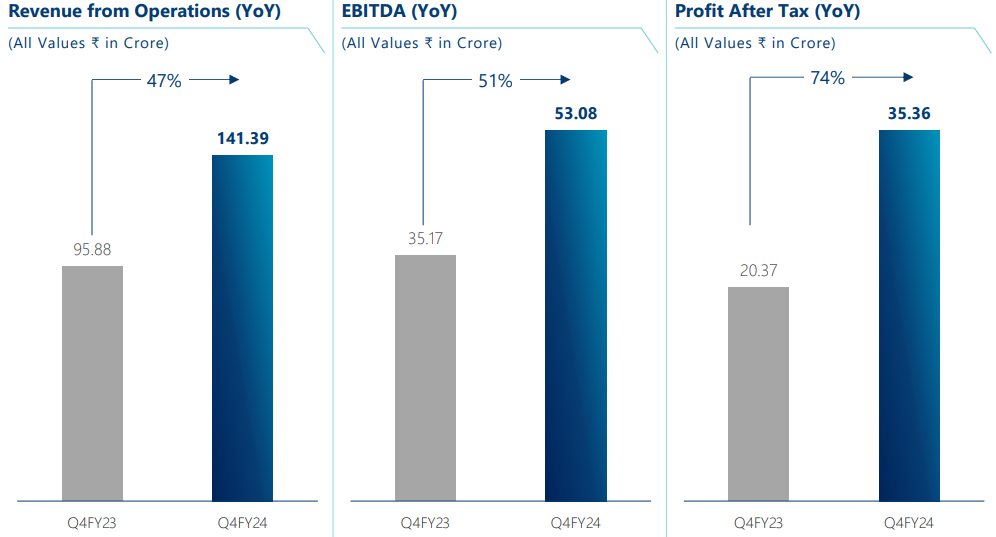

5. Strong Q4-24: PAT up 74% & Revenue up 47% YoY

6. Strong FY24: PAT up 197% & Revenue up 101% YoY

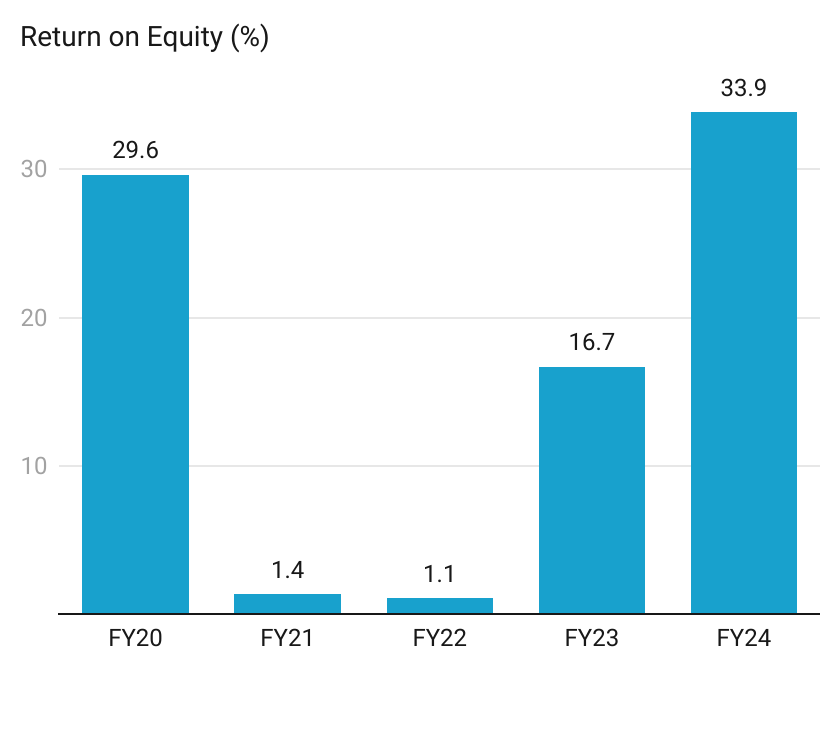

7. Business Metrics: Return Ratios improving strongly

8. Outlook: 100%+ revenue growth in FY25

i. FY25: Revenue growth of 100%+

Revenue to more than double from Rs 440 cr in FY24 to Rs 900cr+ in FY25

With a robust order book exceeding ₹1400 crores as of March 31, 2024, we are poised for sustained growth in FY25, aiming to surpass the ₹900 crore sales mark.

iii. FY25-27: Revenue CAGR of 50%+

iii. Strong Order book: Revenue visibility for FY25

Oder book to be replenished in Q3 and Q4 of FY25

9. PAT growth of 197% & Revenue growth of 101% in FY24 at a PE of 71

10. So Wait and Watch

If I hold the stock then one may continue holding on to ZENTEC.

Coverage of ZENTEC was initiated after Q1-24 results. The investment thesis has not changed after a strong a strong FY24

The outlook for ZENTEC is strong in FY25 with a guidance of 100%+ top-line growth on the back of a strong order book.

One needs to keep a watch on the margins expected to reduce from 43% in FY24 to 35% in FY25

One can continue to ride the business momentum in ZENTEC.

11. Join the ride

If I am looking to enter ZENTEC then

ZENTEC has delivered PAT growth of 197% & Revenue growth of 101% in FY24 at a PE of 67 which makes the valuations fair in the short term.

ZENTEC is guiding for a revenue growth of 100% to reach Rs 900+ cr in FY25 from Rs 440 cr in FY24 at PE of 67 which makes the valuations reasonable in the medium term.

ZENTEC is guiding for a FY25-27 revenue growth of 50% to reach Rs 2000 cr in FY27 from Rs 900+ cr in FY25 at PE of 67 which makes the valuations quite reasonable in the long term.

Previous coverage of ZENTEC

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer