Zen Technologies: PAT growth of 247% & Revenue growth of 143% in 9M-24 at PE of 57

100%+ growth guidance in FY24. 100% growth guidance in FY25. 50% growth guidance for FY26. Order book is 1.5X+ FY25 expected revenue. Possibility of inorganic growth kicking in from FY26

1. Defence training & anti-drone solutions provider

zentechnologies.com |NSE: ZENTEC

2. Growth picking up in FY23

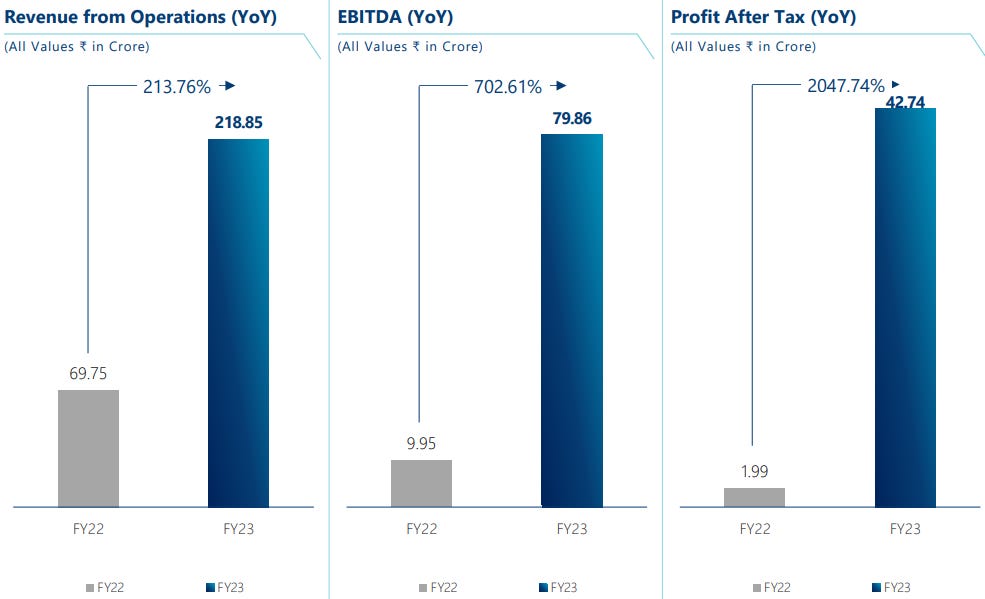

3. FY23: PAT up 2048% & Revenue up 214%

This year has been a strong one, as we achieved our highest-ever revenue.

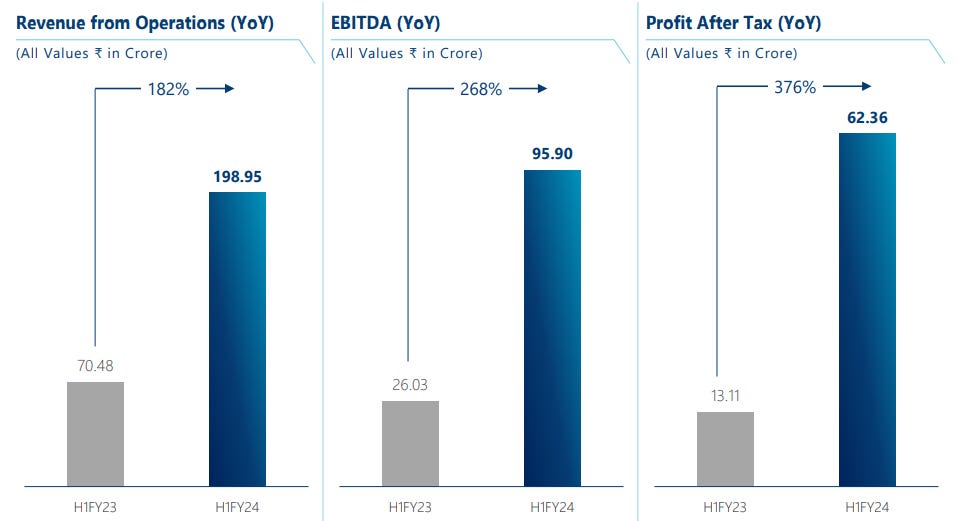

4. Strong H1-24: PAT up 376% & Revenue up 182%

5. Strong Q3-24: PAT up 22% & Revenue up 90% YoY

6. Strong 9M-24: PAT up 247% & Revenue up 143% YoY

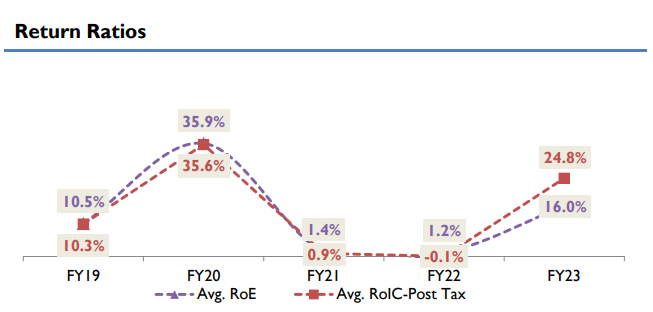

7. Business Metrics: Return Ratios improving strongly

8. Outlook: 134% CAGR growth between FY23-25

i. FY24: Revenue growth of 100%+

we remain on track to achieve our revenue target of ₹450+ crores for FY24.

ii. FY25: Revenue growth of 100%

Building on this momentum, we are confident in our ability to achieve a turnover of ₹ 900+ crores in the next financial year

iii. FY26: Revenue growth of 50%+

we could be easily talking 1,500 crores in FY26, based on the strength of the thing that we are getting now, but till we actually get the orders in hand, we're not able to tell that but 1,500 crores looks like a safe prediction, very safe prediction I feel.

iii. Strong Order book: Revenue visibility till FY25

9. PAT growth of 247% & Revenue growth of 143% in 9M-24 at a PE of 57

10. So Wait and Watch

If I hold the stock then one may continue holding on to ZENTEC.

Coverage of ZENTEC was initiated after Q1-24 results. The investment thesis has not changed after a strong Q3-24, while Q2-24 was not that strong. The management is on track to deliver a strong FY24

the company's best ever 9-month performance in its history

FY24 is on course to become the most successful year to date in terms of financial performance and new order wins for the company.

We remain on track to achieve our revenue target of ₹450+ crores for FY24.

We expect the fourth quarter to be very heavy

The order book remains robust, and we are optimistic about securing additional contracts.

Export markets continue to offer significant growth opportunities, which the company is actively pursuing with its competitive product offerings.

11. Join the ride

If I am looking to enter the stock then

ZENTEC has delivered PAT growth of 247% & Revenue growth of 143% in 9M-24 at a PE of 57 which makes the valuations fair.

ZENTEC is guiding for a revenue growth of 106%+ to reach Rs 450 cr in FY24 at PE of 57 which makes the valuations reasonable.

ZENTEC is guiding for a revenue growth of 100% to reach Rs 900+ cr in FY25 from Rs 450+ cr in FY24 at PE of 57 which makes the valuations reasonable.

ZENTEC is guiding for a revenue growth of 50% to reach Rs 1500 cr in FY25 from Rs 900+ cr in FY25 at PE of 57 which makes the valuations quite reasonable.

On the flip side the margin for error is small. One bad quarter and the asking rate will become quite high. This aspect becomes important given that Q2-24 was weak on QoQ basis.

The potential for future organic growth will provide roadmap for growth from FY26 onwards. We are assuming that the growth to Rs 900+ cr revenue in FY25 will be driven by the order book and not the potential for inorganic growth

Zen is also looking at opportunities to expand inorganically through acquisition. To support this path of probable growth, we have passed an enabling resolution to raise funds. This resolution allows for the raising of funds up to an aggregate amount of ₹ 1,000 Crores.

Previous coverage of ZENTEC

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

Perspectives may change based on evolving understanding of the company.

Focus is on identifying potential stock ideas for long-term market-beating returns.

Content does not constitute explicit stock recommendations.

Investors should conduct thorough stock research and seek professional advice.

Information is for educational purposes and not financial advice or a call to action.