Yatharth Hospital FY26 Result: PAT up 30%, Strong FY27 Guidance

Guides for 36%+ revenue CAGR for FY27 with stable margins. Strong outlook of increasing capacity to 5000 beds. Yatharth available at reasonable forward valuations

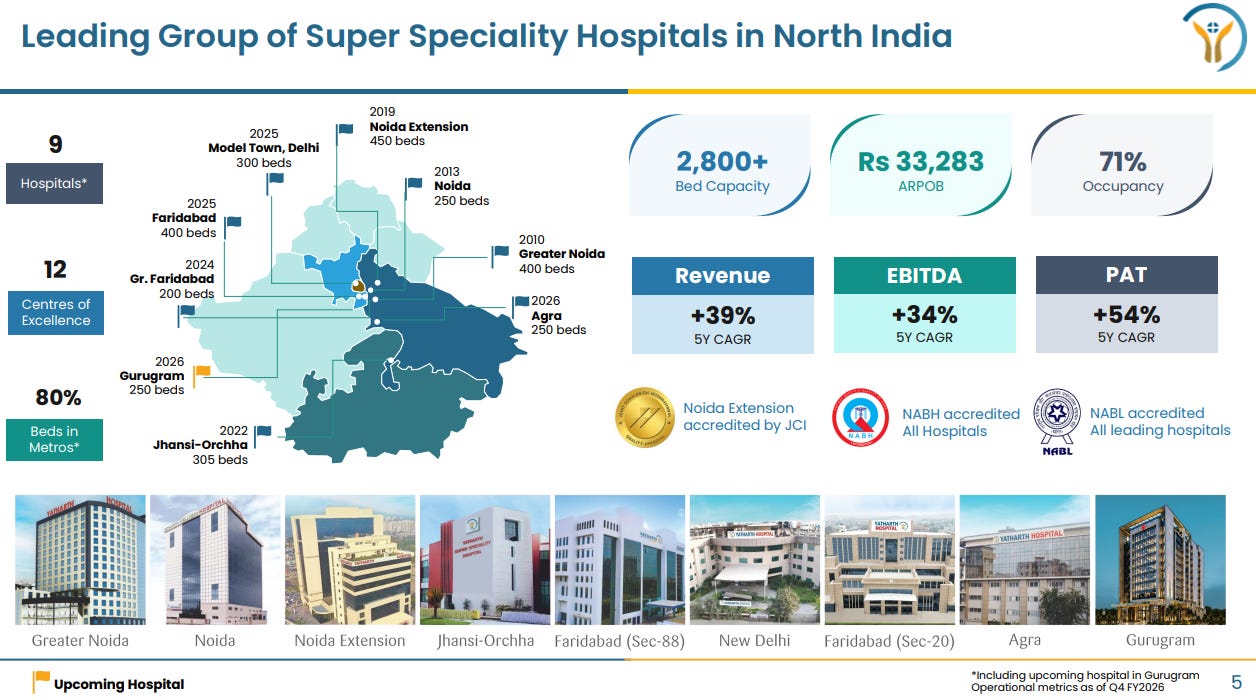

1. Super specialty hospital chain

yatharthhospitals.com | NSE: YATHARTH

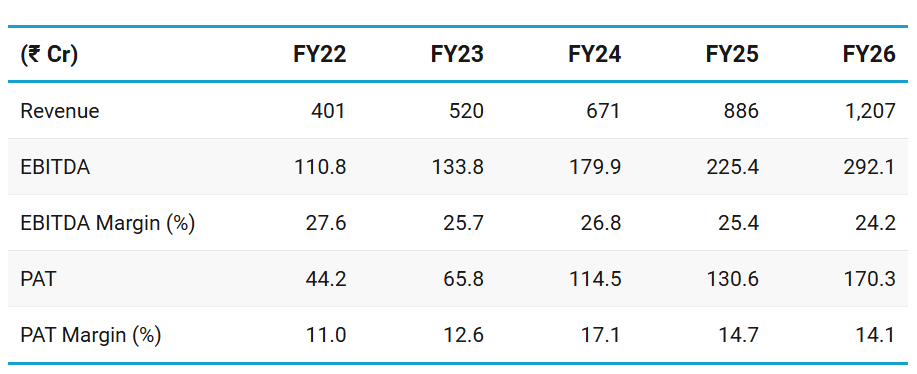

2. FY22–25: PAT CAGR 40% & Revenue CAGR 32%

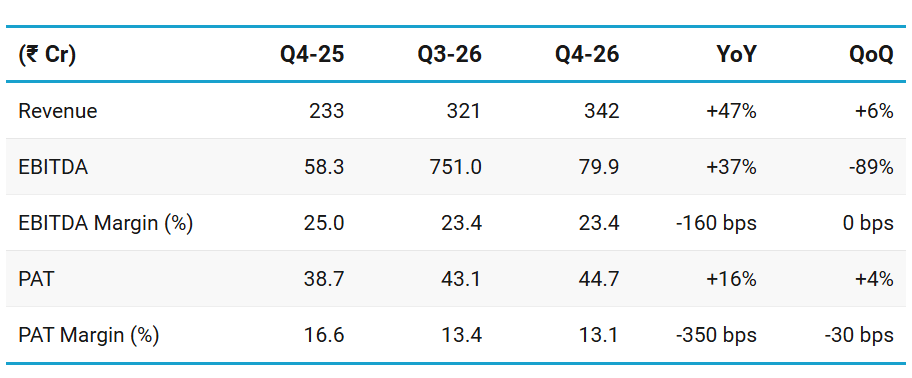

3. Q4-26: PAT up 16% & Revenue up 47% YoY

PAT up 4% & Revenue up 6% QoQ

4. FY26: PAT up 30% & Revenue up 36% YoY

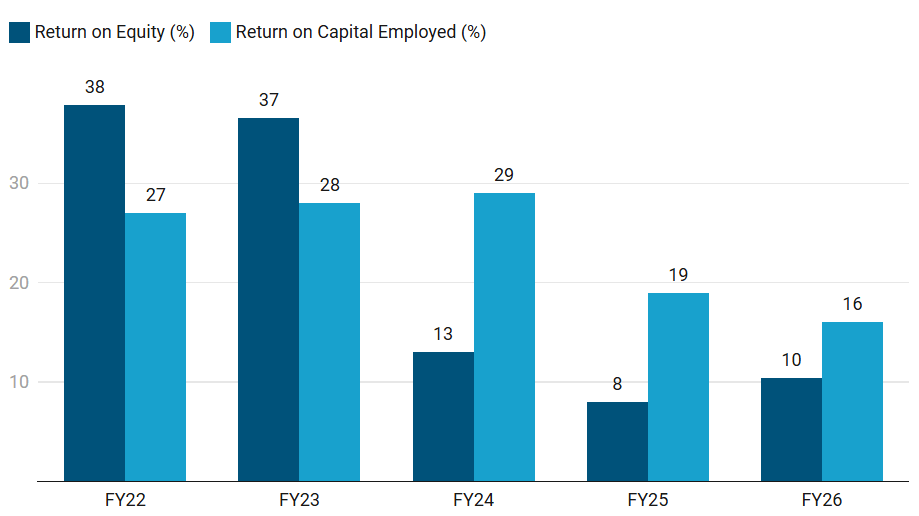

5. Business Metrics: Weakening Ratios — Impacted by Expansions & Acquisitions

Yatharth is in a heavy expansion phase.

Fixed assets including goodwill increased, borrowings rose and the company has acquired/started multiple hospitals.

Denominator of ROE/ROCE has increased before the full profit contribution has come through.

That is not necessarily bad.

But it means FY27/FY28 must prove that the capital deployed can earn strong returns.

6. Outlook: 36%+ Revenue Growth; Stable Margin

6.1 Outlook for FY26 — Yatharth Hospital

For next 3 years, we do expect 8% to 10% ARPOB growth clearly.

FY27:

Our guidance remains the same, as we have always maintained that last few years the company has grown close to around 30%. I think in the upcoming years also, including this year, we remain on track for that.

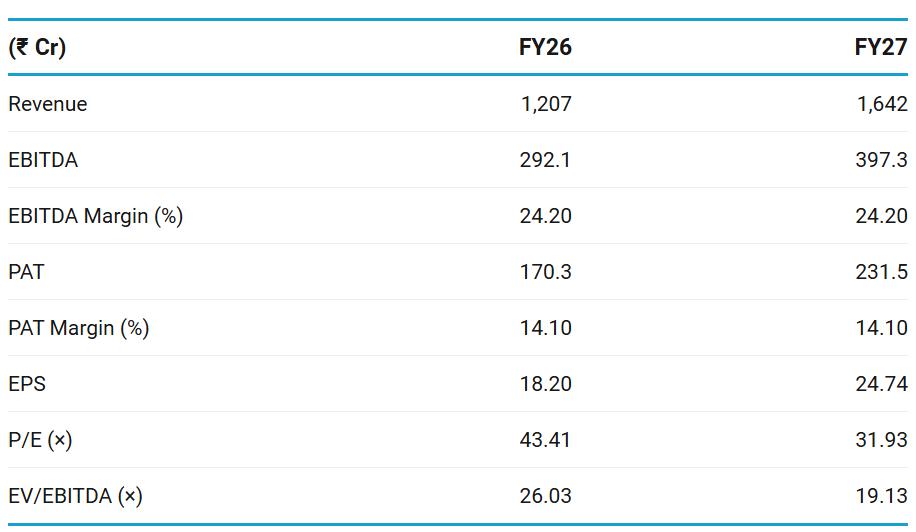

FY27 revenue growth — growth should surpass FY26 growth of 36%.

EBITDA margin — continues to guide for 24–25% consolidated EBITDA margin

FY27 EBITDA should be better than FY26, despite new hospital ramp-up.

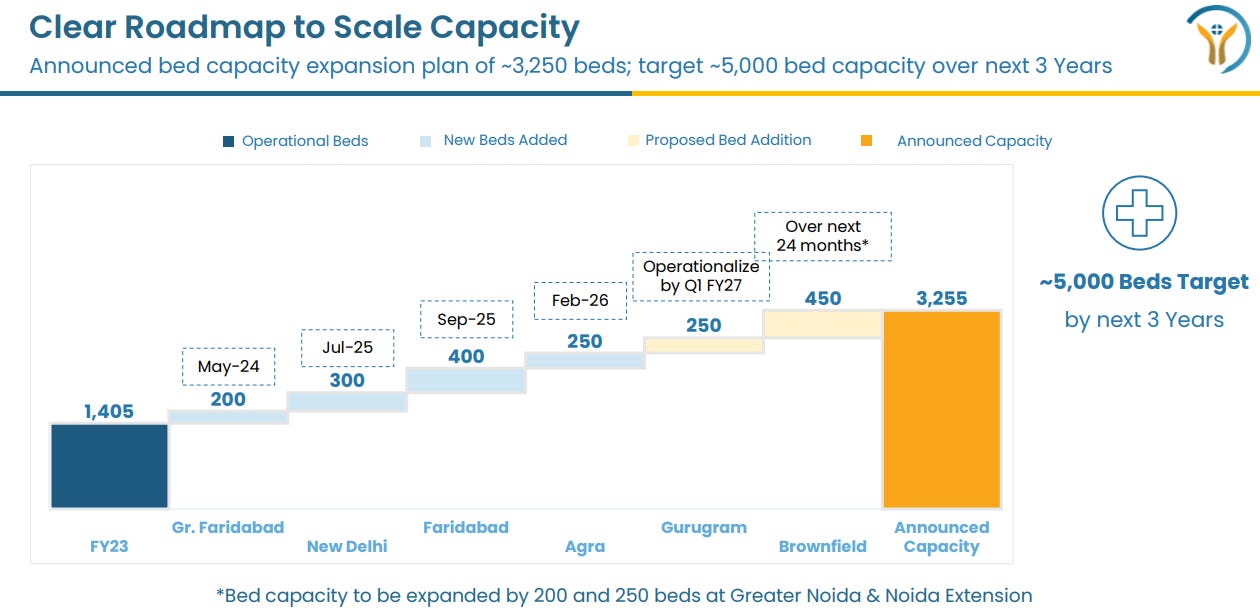

Bed expansion — target of 5,000 beds over next 3 years

May reach this target earlier.

70% of future bed additions may come through acquisitions and around 30% through greenfield/brownfield expansion

New hospital ramp-up

New Delhi / Model Town — 300 beds

Current occupancy: ~32% on 100 census beds

Monthly revenue: ~₹6 Cr

ARPOB: ~₹40k

Expected EBITDA break-even: 14–15 months, likely FY27 H2

Faridabad Sector-20 — 400 beds

Current occupancy: ~52% on 100 census beds

Monthly revenue: ~₹8–9 Cr

ARPOB: ~₹38k

Expected EBITDA break-even: month 10–11, likely FY27 H2

These two hospitals are the main FY27 operating leverage trigger. If they break even in H2 FY27, reported EBITDA margin can improve.

Agra — integrated from February 2026.

Capacity: 250 beds

Monthly revenue: ~₹7 Cr

ARPOB: ~₹26–27k

EBITDA margin: management said around 18%

Role: feeder hub for oncology and high-value specialties into NCR hospitals

Gurugram — next major growth asset.

250-bed under-construction super-speciality hospital

Sector 40, Central Gurugram

Acquisition cost: ~₹100 Cr

Additional outlay: ~₹100 Cr

Total proposed outlay: ~₹200 Cr

Expected operationalisation: April 2027

ARPOB potential: ₹50k+

Expected EBITDA break-even: around 15 months after operationalisation

Gurugram is more FY28 than FY27 — It improves long-term ARPOB potential but will require capital and may create initial ramp-up losses.

ARPOB — ARPOB growth should be close to 10% driven by

new premium hospitals

higher private insurance/cash mix

international patients

better speciality mix.

Occupancy outlook

FY26 occupancy was 68%, and Q4 FY26 occupancy was 71%.

Yatharth can grow revenue without adding too many new beds immediately, simply by increasing census beds and occupancy in the recently added hospitals.

Payer mix — Government business ~35% of revenue.

Management wants to reduce this to ~25% over the next two financial years.

6.2 FY26 Performance vs FY26 Guidance

Revenue, margins In-line, capacity expansion on schedule

I think we are being actually a bit conservative when we’re seeing 30% revenue growth. We feel that this number should be easily overachieved

Revenue Growth: Over-achieved 30% growth as per guidance

EBITDA Margin: Guidance just met at the lower end of the 24-25% guidance range

FY26 added 950 beds operationally: New Delhi, Faridabad Sector-20 and Agra.

This is a very large expansion — around 59% increase over FY25 operational capacity of ~1,605 beds.

7. Valuation Analysis

7.1 Valuation Snapshot — Yatharth Hospital

Current Market Price= ₹790; Market Cap = ₹7,912 Cr

Fully-priced from an FY26 perspective — Yatharth’s valuation is ahead of current return ratios.

The stock is not expensive because growth is weak — growth is strong.

It is expensive because ROE is only ~10.4% and ROCE is only ~12–16%, while the stock trades at ~4.3x book and ~44x earnings.

For valuation comfort, the company must show that expansion converts into higher returns.

The key trigger is not just revenue growth. The real trigger is: ROE moving toward 15%+ and ROCE moving toward 18–20% while maintaining 24–25% reported EBITDA margin.

Until then, the stock deserves a growth premium, but not a large margin of safety.

Reasonably priced from an FY27 perspective as full year impact of profitable Agra hospital is felt. – possibility of re-rating of multiples

Opportunity emerges beyond FY28 as addition of beds is completed and operations start stabilizing with integration of New Delhi (Model Town)/ Fairdabad hospital.

7.2 Opportunity at Current Valuation

The opportunity is in FY28/FY29 earnings catch-up if the 5,000-bed plan is executed on-time with efficiency.

Limited opportunity in FY26 valuation.

Doubling of capacity to approximately 5,000 beds within 3 years is not yet discounted

Management is targeting ~5,000 beds over the next 3 years, compared with current operational capacity of around 2,555 beds and announced capacity of ~3,255 beds could create a 3x opportunity in YATHARTH

2x beds +

improving APROB

improving occupancy

improving margins — as hospitals mature

improving payor mix with reduction of government schemes.

7.3 Risk at Current Valuation

Risks in execution towards 5,000 bed is the biggest risk

Margin of safety is limited at current valuations is limited.

Delays in expansion could lead to a negative reaction in the stock price

The new hospitals are promising, but not fully mature. Delay in break-even can hurt reported margins and market confidence.

70% of future beds may come through acquisitions. This leads to

Integration risk — acquired hospitals may not ramp as planned.

Capital allocation risk — paying too much for assets can depress ROCE.

Goodwill risk — goodwill has already increased meaningfully after acquisitions.

At high valuation, the market is assuming acquisitions will be disciplined and profitable.

Recent Coverage of YATHARTH

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer