Welspun Corp: 90% EBITDA growth & 50% revenue growth in FY24 at a PE of 17

The industry is seeing tailwinds and WELCORP is trying to capitalize upon that and its pipe business is doing phenomenally well. H1FY24 performance is in line with its guidance for FY24.

1. One of the largest manufacturers of large diameter pipes globally

welspuncorp.com | NSE : WELCORP

Top 3 global Line Pipe manufacturer

The company also manufactures BIS-certified Steel Billets, TMT (Thermo Mechanically Treated) Rebars, Ductile Iron (DI) Pipes, Stainless Steel Pipes, and Tubes & Bars.

The company recently acquired Sintex-BAPL, a market leader in water tanks and other plastic products, to expand its building materials portfolio.

It has also acquired specified assets of ABG Shipyard with a potential to enter Defence and commercial shipbuilding, green steel, ship breaking, and ship repair.

2. FY13-23: An Average business

Nothing bad, nothing spectacular to talk about

Went nowhere in the last decade

Consistent Performance over the last 10 years: EBITDA in the range of INR 800 – 1200 crores per annum from Line Pipes Business

3. Weak FY23: PAT down 53% & Revenue up 50% YoY

4. Strong Q1-24: PAT up 3924% and Revenue up 208% YoY

Q1-24 Results are strong on a QoQ basis

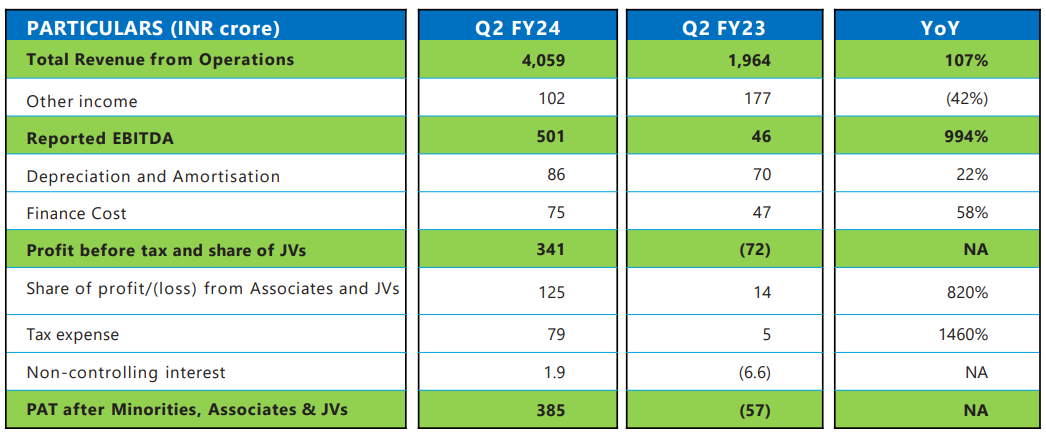

5. Strong Q2-24: Revenue up 107% YoY & back in profit

PAT up 41% and Revenue up 3% QoQ

6. Strong H1-24: Revenue up 147% YoY & back in profit

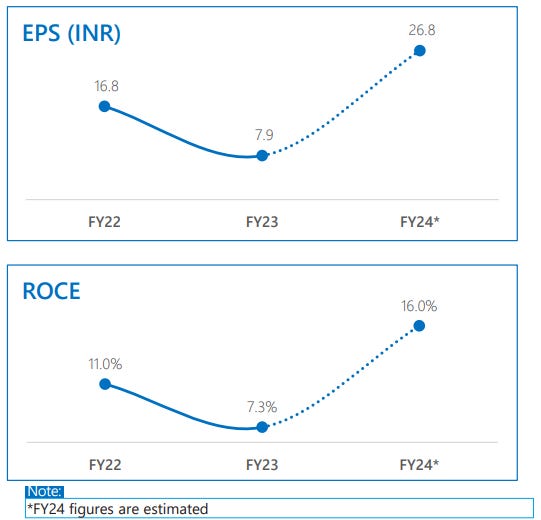

7. Business metrics: Return ratios improving in H1-24

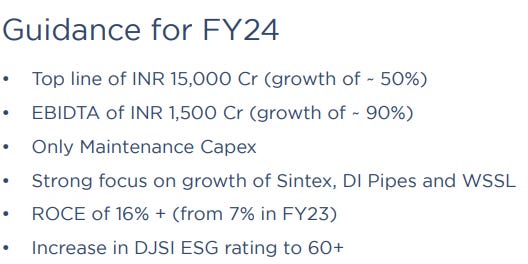

FY24 ROCE guidance of 16%, 2X+ over FY23 ROCE

8. Outlook: 50% revenue growth and 90% EBITDA growth in FY24

i. Progress till H1FY24 has been in line with our guidance

EPS Guidance for FY24 should be beaten as H1-24 EPS = 20.98

9. 90% EBITDA growth & 50% revenue growth in FY24 at a PE of 17

10. So Wait and Watch

If I hold the stock then one may continue holding on to WELCORP

Coverage of WELCORP was initiated after Q1-24 results. The investment thesis has not changed after a strong H1-24. The only changes are the delivery of a strong H1-24 and the increased confidence in the management to deliver a stronger FY24

There is a strong possibility of FY24 guidance to be beaten.

WELCORP does not have a consistent track record of delivering growth. One needs to monitor execution on its guidance quite closely and then look at the guidance for FY25.

11. Or, join the ride

If I am looking to enter WELCORP then

WELCORP is guiding for 90% EBITDA growth & 50% revenue growth in FY24 at a PE of 17 which makes the valuations reasonable.

WELCORP generated Rs 950 cr in H1-24. It is available at free cash flow yield of 6.95% (not annualized) which makes the valuations quite attractive.

WELCORP is at a market cap to FY24 sales of less than 1

Previous coverage of Kilburn

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades