Venus Pipes & Tubes: PAT growth of 93% & Revenue up 55% in FY24 with Revenue CAGR of 35% till FY23-25 at a PE of 42

With improving demand environment & order visibility, VENUSPIPES is optimistic of growth momentum sustaining. Increased capacities & increasing utilization will drive the revenues & margins

1. Manufacturer of stainless-steel pipes and tubes

venuspipes.com | NSE: VENUSPIPES

Revenue Split

2. PAT CAGR= 86%, Revenue CAGR= 47%, for FY19-23

YoY sequential growth over five years from FY19-23

3. Strong Q1-24: PAT up 91% and Revenue up 58% YoY

PAT up 29% and Revenue up 2% QoQ

4. Strong Q2-24: PAT up 97% and Revenue up 51% YoY

PAT up 17% and Revenue up 7% QoQ

5. Strong H1-24: PAT up 93% and Revenue up 55% YoY

6. Solid return ratios , dip in FY23 needs to be watched

7. Strong outlook: Revenue CAGR of 35% till FY25

i. Revenue CAGR of 35% till FY25 followed by revenue CAGR of 15-20% till FY28

Regarding the growth type, for FY2024 and FY2025, we are seeing CAGR of 35% for FY2024 and FY2025 and further for FY2026 and FY2027 and FY2028 we are foreseeing growth of almost 15 to 20% every year, so we have right now plan for five years. We have further plans after that also but right now we can say for five years this is our plan.

ii. Strong revenue visibility

our current order book stands at Rs. 210 Crores

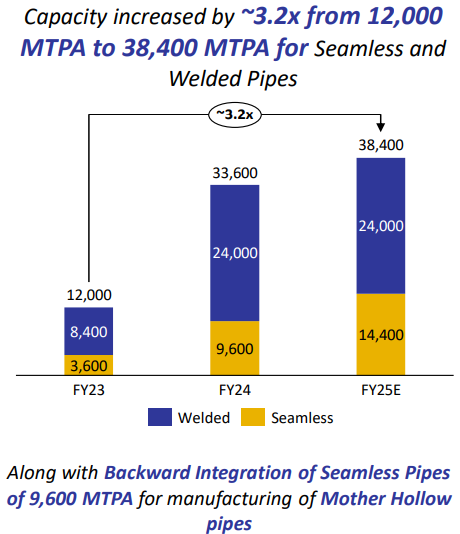

iii. Planned capacity expansion in place to support demand growth

the additional 400 MTM installation of the capacity for seamless pipe is on track and expected to be completed by Q4 of the FY2024.

iii. Cash flow improvement from H2-24

Definitely a second-half will also see a much better operating cash flow as compared to what we have achieved in the first year but I think FY2025 would be a very good year, cash flow from operation should be there in good quantum.

8. PAT growth of 93% and Revenue up 55% in FY24 with Revenue CAGR of 35% till FY23-25 at a PE of 42

9. So Wait and Watch

If I hold the stock then one may continue holding on to VENUSPIPES

Coverage of VENUSPIPES was initiated after Q1-24 results. The investment thesis has not changed after a strong H1-24. The only changes are the delivery of a strong H1-24 and the increased confidence in the management to deliver a stronger FY24

Order book of Rs 2010 cr and the outlook of 35% CAGR from FY23-25 and 15-20% CAGR going forwards provides visibility for the medium to long term

Historically, H2 has always been a stronger half as compared to H1.

Capacity expansion is in place to support the demand

10. Join the ride

If I am looking to enter VENUSPIPES then

VENUSPIPES has delivered PAT growth of 93% and revenue growth of 55% in H1-24 at a PE of 42 which makes the valuations reasonable.

Valuations are priced to perfection. PE of 42 for 35% CAGR top-line growth guidance for FY23-25 with bottom-line growing faster than the top-line

The performance for FY24 looks well discounted in the price. The opportunity in stock is from the performance and growth outlook from FY25 onwards.

A PE of 41 looks rich in the short term hence positions need to be built over time over bad days when the stock is not doing well.

Previous coverage of VENUSPIPES

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades