Venus Pipes & Tubes: 2-2.5X revenue by FY25, a track record of 86% PAT CAGR for FY19-23

Shift towards organized players, the implementation of Anti-Dumping Duty (ADD) and Indian capex cycle driving demand for Venus Pipes

1. Manufacturer of stainless-steel pipes and tubes

venuspipes.com | NSE: VENUSPIPES

Venus Pipes & Tubes Limited is a manufacturer and exporter of stainless steel pipes and tubes. The company is manufacturing stainless steel tube products in two broad categories - seamless tubes/pipes and welded tubes/pipes.

Venus a manufacturing plant located in Kutch, Gujarat with an installed capacity of 33,600 MT per annum.

2. PAT CAGR= 86%, Revenue CAGR= 47%, for FY19-23

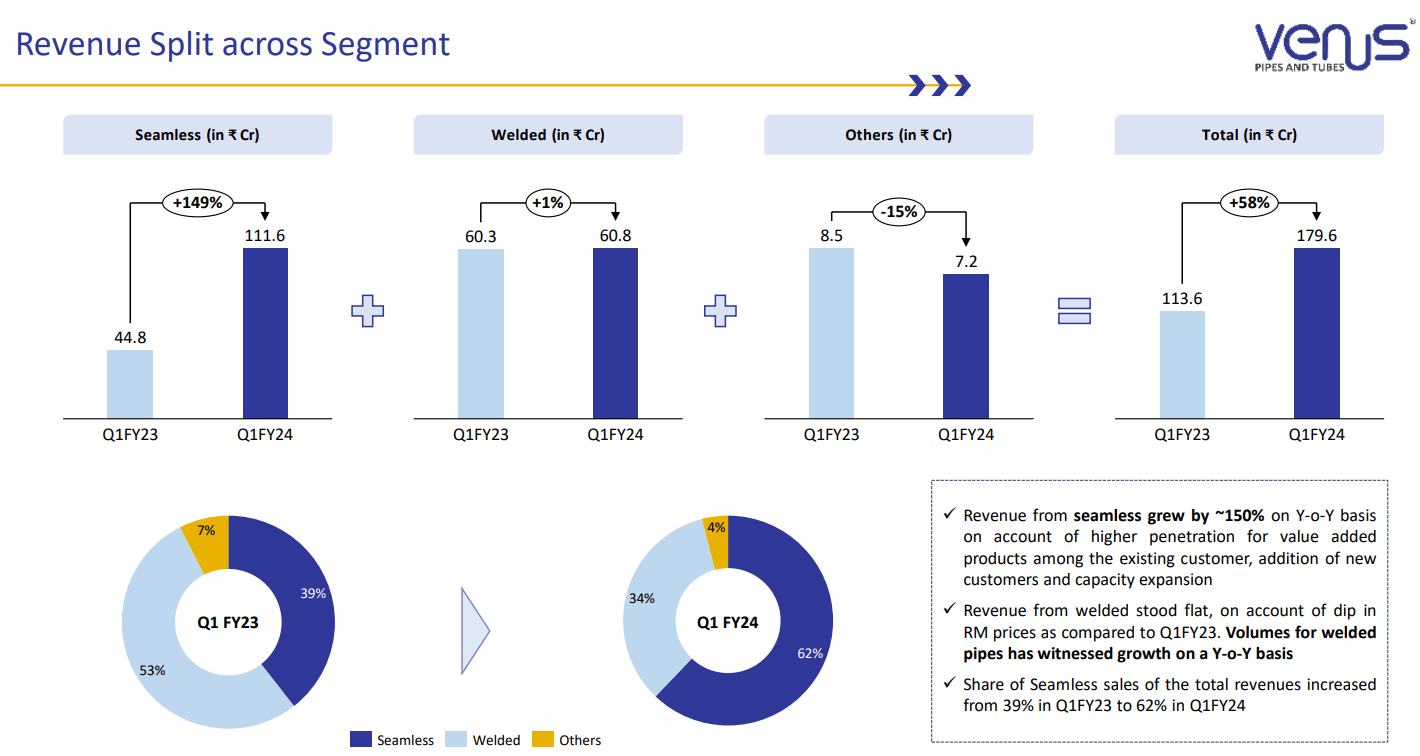

YoY sequential growth over five years from FY19-23

3. Momentum of FY19-FY23 carried in to Q1-24

Growth delivered on both YoY & QoQ basis

We are happy to report robust financial performance with Revenues growing at 58% Y-o-Y and EBITDA growing at 92% Y-o-Y, whilst EBIDTA margins increasing by ~269 bps Y-o-Y

4. Solid return ratios , dip in FY23 needs to be watched

5. Growth from 2.75X capacity expansion in FY24

2.75X capacity expansion in FY24 vs 1.7X in 5 years (FY19-23)

Capacity expansion is the basis for the growth

We started FY24 by commencing operations at our new facilities and now have tripled our capacity along with backward integration of manufacturing of mother hollow pipes. This has not only enhanced our competitiveness but also enabled us to enter new markets and customer segments.

6. Strong outlook for 2-2.5X revenue by FY25

i. Revenue 2-2.5X by FY25. 40-55% revenue CAGR

See the endeavor will always be there to achieve it by FY25.

ii. Volume growth of 79% in FY24

70% capacity utilization indicated for FY24

FY23 Volume = 13,127 MTS

Volume growth for FY24 = 79% (70%X33600/13127)

70% yes. 70% on the total 33600.

iii. FY24 revenue visibility = 0.7X FY23 revenue as of Q1-24 end

FY24 Revenue visibility = Q1-24 revenue + order book (Q1-24 end) = 179.2+ 200 = Rs 379.2 cr

FY24 Revenue visibility = 379.2/ 552 = 0.7X

The order book is around 200 odd crore as on date

iv. 30% growth in the bottom-line in FY24

Take the guidance 30% on a blended basis increase in EBITDA for FY24.

v. Industry tailwinds : Favorable government policy and macro environment in the country

Sustaining the momentum going forward

The industry is witnessing a notable shift towards organized players due to the compulsory BIS certification and the implementation of Anti-Dumping Duty (ADD). This provides us a great opportunity to seize the industry's structural changes. Moreover, the Indian capex cycle is underway, driven by government support and favorable policies, resulting in substantial investments across industries and an increased demand for our products.

7. Revenue CAGR of 40-55% for FY23-25 at a PE of 52

8. So Wait and Watch

If I hold the stock then one must wait and watch for quarterly results to see if the company is on track to deliver 2-2.5X revenues by FY25. Its not a long wait as FY25 is only seven quarters away.

9. Join the ride

If I am looking to enter the stock then

Valuations are priced to perfection. PE of 52 for 40-55% growth guidance

This is story which plays out by FY25 i.e. 7 quarters away. So the upside should come quickly.

On the flip side the margin for error is small. One bad quarter in the seven remaining quarters to reach the FY25 target and the asking rate will become quite high.

Positions need to be built over time over bad days when the stock is not doing well.

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will send you better stuff.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades