Ugro Capital: PAT up 200% & Net Total Income up 64% in FY24 at a PE of 21

FY24 PAT to potentially grow 4X by FY26. PAT growth to be significantly higher than 30% AUM growth. Strong longer term guidance of ROE of 18% and ROA of 4%.

1. NBFC & India’s largest Co-lender in the MSME segment,

ugrocapital.com | NSE: UGRO

Heading Towards Serving 1% of MSME Lending Market

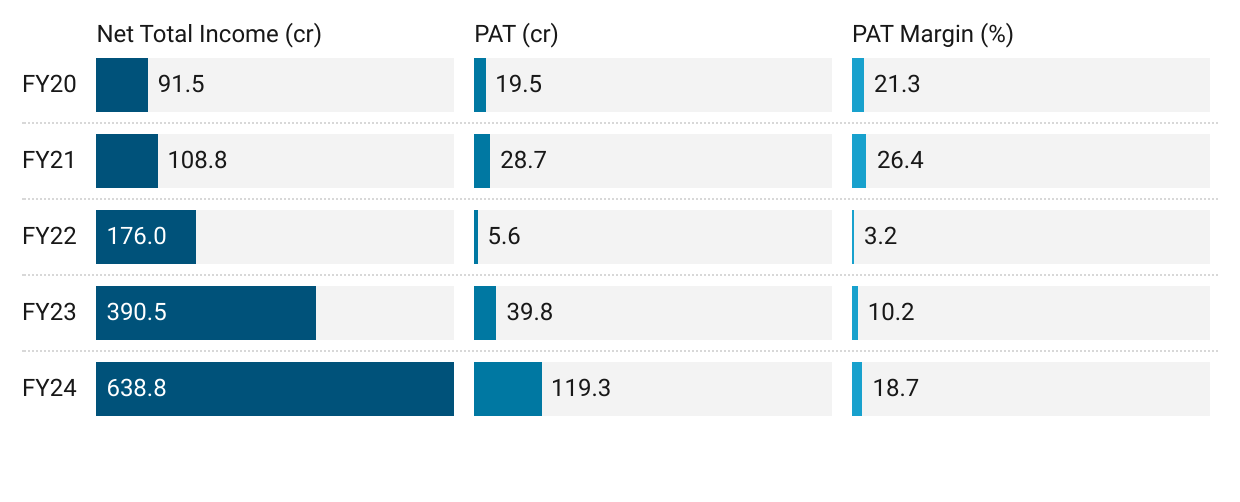

2. FY20-24: PAT CAGR of 57% & Net Total Income CAGR of 63%

3. FY23: PAT up 173% & Net Total Income up 123% YoY

4. Strong 9M-24: PAT up 237% & Net Total Income up 66%

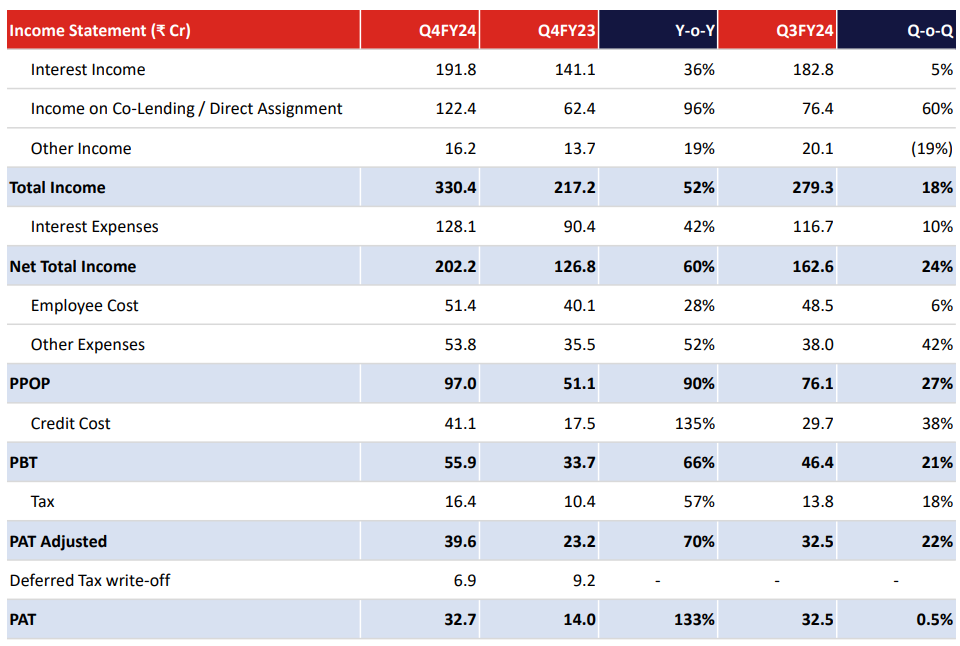

5. Q4-24: PAT up 133% & Net Total Income up 60% YoY

PAT up 0.5% & Net Total Income up 18% QoQ

6. Strong FY24: PAT up 200% & Net Total Income up 64%

7. Business metrics: Improving return ratios

8. Strong outlook: 30%+ PAT growth in FY25

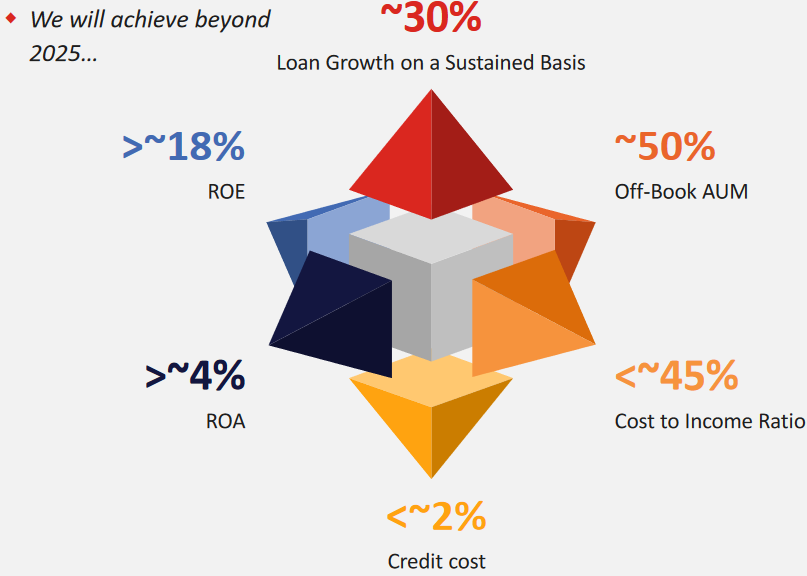

i. FY25: AUM Growth of 30%

We would be growing on a sustainable basis for about for about 30%.

For the next 2 years, whatever capital we would require, we have already locked in that capital.

Our aim is to reach 50% on-book and 50% off-book in the form of co-lending, co-origination and direct assignment.

Cost to income ratio, as of now is closer to 54%, we'd like to take it to 45% which may be over 6 to 8 quarters from now,

Ultimately we'll reach the desired ROA of 4%, which we believe may take around 8 quarters time.

ii. FY24-27: PAT growth significantly higher than AUM growth of 30%

PAT growth will be higher than the AUM growth. Otherwise, this target of reaching 4% ROA cannot happen.

our profit growth would be definitely, significantly higher compared to our AUM growth. And that would continue to be the trend for next 3 years, and it will be significantly superior.

9. PAT growth of 200% & Net Total Income growth of 64% in FY24 at a PE of 21

10. So Wait and Watch

If I hold the stock then one may continue holding on to UGRO

Coverage of UGRO was initiated after Q3-24 results. The investment thesis has not changed after a strong FY24 which keeps it on track to meet its longer term guidance. The delivery of a strong FY24 has increased confidence in the management to deliver a FY25 as per the guidance

The outlook for PAT growth significantly higher than AUM growth is a reason to continue with UGRO.

UGRO is in the middle of a strong run. It is consistently increasing PBT over past 8 quarters.

11. Join the ride

If I am looking to enter UGRO then

UGRO has delivered PAT growth of 200% & Net Total Income growth of 64% in FY24 at a PE of 21 which makes the valuations fairly priced in the short term.

Outlook for UGRO PAT growth higher than the AUM growth of 30% over the longer term at a PE of 21 makes the valuations quite reasonable over the mid to longer term.

With a stock price of Rs 276.25 against a book value of Rs 157 as of Q4-24 end implies that UGRO is available a price to book of 1.76 which makes the valuations reasonable from a longer term purpose.

Book Value per Share INR 157.0 as on Mar’24

The guidance for FY26 aims for a ROE of 18%. Net-worth of Rs 2770 cr as of in FY26 without adding the profitability in the next year delivering a ROE of 18% implies FY26 PAT of 18% X 2770 = Rs 486 cr which is 4X the FY24 PAT of Rs 119.3 cr. PAT becoming 4X by FY26 provides the longer term opportunity in UGRO.

Our capital raise of Rs 1,330 crore added to networth of 1,440 crore, and 2 years of profitability should be the networth. When we apply 18% RoE, our Eps would be far superior than what it is today.

Previous coverage of UGRO

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer