Ugro Capital: PAT up 62% & Revenue up 37% in 9M-24 at a PE of 22

Strong roadmap for growth in place based on guidance for FY25. Based on 9M-24 performance, UGRO is on track to deliver as per FY24 & FY25 guidance.

1. NBFC & India’s largest Co-lender in the MSME segment,

ugrocapital.com | NSE: UGRO

Heading Towards Serving 1% of MSME Lending Market

2. FY20-23: PAT CAGR of 27% & Net Total Income CAGR of 62%

3. FY23: PAT up 173% & Net Total Income up 123% YoY

4. H1-24: PAT up 329% & Net Total Income up 76% YoY

5. Q3-24: PAT up 148% & Net Total Income up 51% YoY

PAT up 13% & Revenue up 10% QoQ

6. Strong 9M-24: PAT up 237% & Net Total Income up 66%

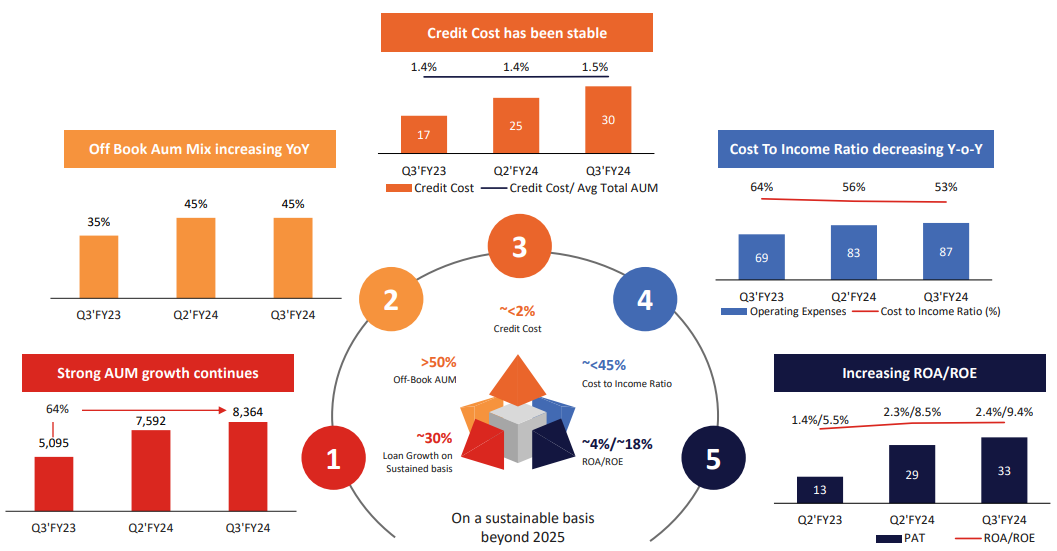

7. Business metrics: Strong return ratios & cash generation

8. Strong outlook: Road map in place till FY25

i. FY24: On track to deliver as per guidance

AUM INR10,000 cr

RoA of 3.1%

RoE of 10%

ii. On track to deliver on FY25 guidance

9. PAT growth of 237% & Net Total Income growth of 66% in 9M-24 at a PE of 22

10. So Wait and Watch

If I hold the stock then one may continue holding on to UGRO

Based on 9M-24 performance, UGRO looks on track to deliver the strongest PAT in FY24

UGRO is in the middle of a strong run. It has delivered sequential QoQ growth of PAT for four quarters in a row.

UGRO is on track to deliver as per the FY24 & FY25 guidance

11. Join the ride

If I am looking to enter UGRO then

UGRO has delivered PAT growth of 237% & Net Total Income growth of 66% in 9M-24 at a PE of 22 which makes the valuations quite reasonable.

With a stock price of Rs 261.5 against a book value of Rs 153.8 as of Q3-24 end implies that UGRO is available a price to book of 1.7 which makes the valuations reasonable

The guidance for FY25 aims for a ROE of 18%. The net-worth of Rs 1405 cr as of Q3-24 end implies a FY25 PAT of Rs 250+ cr (18%X1405) which could be a 100%+ growth over the FY24 PAT. Even if PAT grows by 50% in FY25, there is opportunity in UGRO.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer