Tinna Rubber & Infrastructure: PAT growth of 85% & Revenue growth of 23% in FY24 at a PE of 53

Guiding for 37%+ revenue growth in FY25. Strong outlook till FY27 with revenue CAGR of 35%, profitability growth of 33% & EBITDA margin expansion from 12.4% to 18% with a target ROCE of 30%

1. Recycler of End of Life Tyres

tinna.in | BOM: 530475

on the micronized rubber powder, we have probably more than 80% market share in India.

2. FY20-24: EBITDA CAGR of 62% & Revenue CAGR of 31%

Profitability from FY22

3. Strong FY23: PAT up 29% & Revenue up 29% YoY

4. Strong 9M-24: PAT up 57% & Revenue up 14% YoY

5. Strong Q4-24: PAT up 132% & Revenue up 51% YoY

PAT up 57% and Revenue up 18% QoQ

6. Strong FY24: PAT up 85% & Revenue up 23% YoY

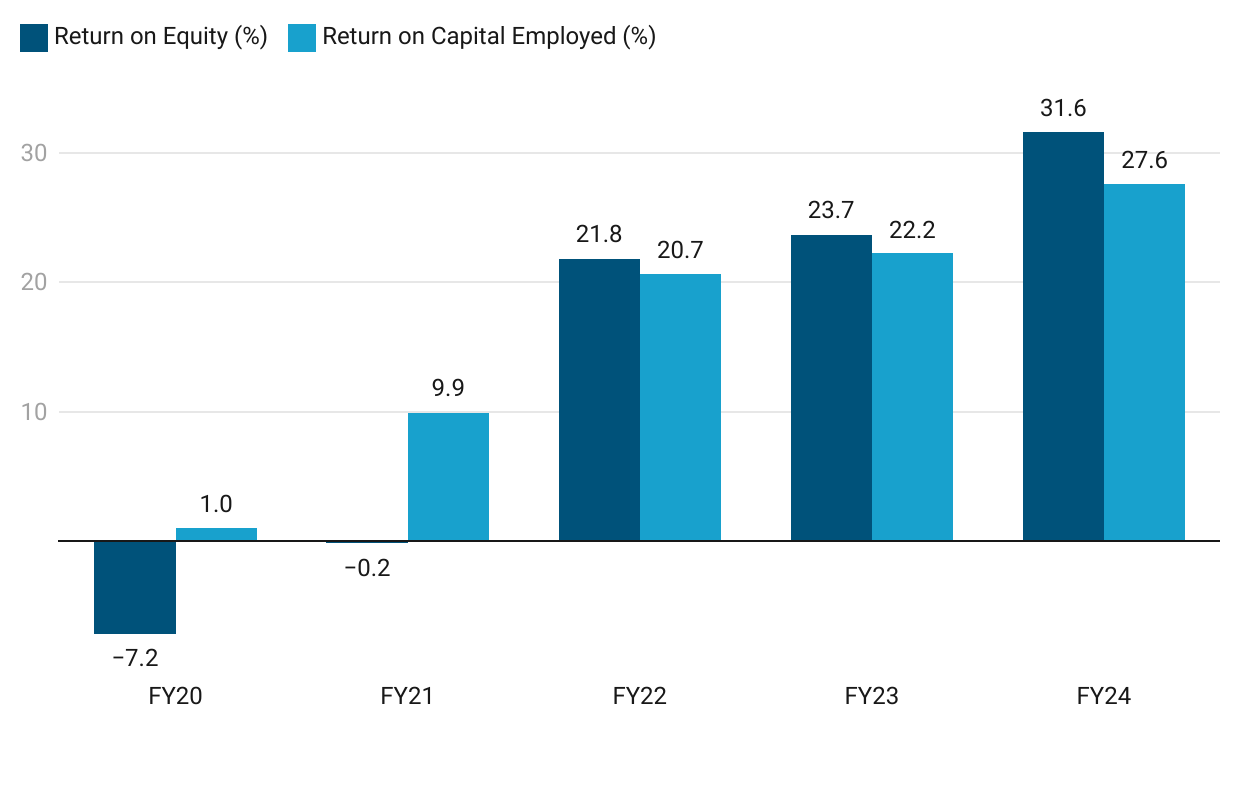

7. Business metrics: Strong & Improving return ratios

Target ROCE: 30%

8. Outlook: 37% Revenue growth in FY25

i. FY24: Revenue growth of 37%+

Growing from Rs 363 cr to Rs 500 cr in FY25 implies a growth of 37%+

we want to get to 500 in this year and INR 900 by FY '27.

ii. Vision 2027: Revenue CAGR of 35% for FY24-27

While management is guiding for 25%+ revenue growth, the growth of Rs 363 cr in FY24 to Rs 900 cr in FY27 implies an actual revenue CAGR or 35%

We remain completely committed and focused towards achieving it. To reiterate, it is our aim to reach revenues of INR 900 crores by FY27 and achieve EBITDA margins of 18% plus and return on capital employed of over 30%.

ii. Capacity expansion in place to support Vision 2027

9. PAT growth of 85% & Revenue growth of 23% in FY24 at a PE of 44

10. So Wait and Watch

If I hold the stock then one may continue holding on to Tinna

Tinna has delivered ahead of its guidance of Rs 340 cr of revenue in FY24 which gives confidence in its ability to deliver as per FY25 guidance

We expect our FY24 number to be at around 340 odd crores and we are very much progressing towards that and

FY25 number we are expecting roughly 500 crores of revenue

Tinna is in the middle of a strong run and has delivered sequential QoQ growth in PAT for 6 consecutive quarters starting Dec-22

The road map laid out till FY27 provides opportunity to stay in the stock.

11. Or, join the ride

If I am looking to enter Tinna then

Tinna has delivered PAT growth of 85% & Revenue growth of 23% in FY24 at a PE of 53 which makes valuations fairly priced in the short term.

Tinna is guiding for revenue growth of 37%+ in FY25 at a PE of 53 which makes valuations quite reasonable in the medium term.

Tinna has a strong outlook till FY27 with revenue growing to Rs 900 cr at CAGR of 35% at a PE of 53 which makes valuations quite reasonable from the long term

In the short-term there may not be margin of safety in Tinna at a PE of 53. Even a single weak quarter could trigger a strong reaction on the price.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer