Time Technoplast: PAT growth of 40% & Revenue growth of 16% in 9M-24 at a PE of 19

Value unlocking 18% of market cap in FY25. Reduction in interest cost & higher contribution of value added products to drive PAT growth much higher than 15% revenue growth guided for FY25

1. Industrial Packaging Company

timetechnoplast.com | NSE : TIMETECHNO

Products

Business Segments

Business growth to be driven by Composite Cylinders

FY24: we are achieving this year in the range of around Rs.500 crores

FY25: But definitely next year it's around 800 crores

FY27: We are targeting in the next three years’ time which will reach to 1,500 crores.

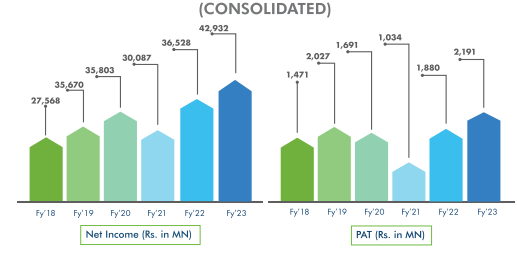

2. FY18-23: Top-line growth not converted into bottom-line growth

3. FY23: PAT up 17% & Revenue up 18% YoY

4. Strong H1-24: PAT up 34% & Revenue up 16% YoY

5. Strong Q3-24: PAT up 50% & Revenue up 17% YoY

PAT up 30% and Revenue up 11% QoQ

6. Strong 9M-24: PAT up 40% & Revenue up 16% YoY

7. Business metrics: Targeting ROCE improvement

Against last year ROCE, which was 13.5%, in nine months 15.6% there's a 2% increase in the ROCE.

Full year ROCE at the end of the year, we are targeting 15.5%

next 3 years overall objective in the company to reach the ROCE around 20%.

8. Outlook: 15% top-line growth in FY23-25

i. 15% top-line growth in FY23-25

FY24: we are growing around 15%, so our target is 5,000 crores

FY25: next year also, we achieve more than that. 15% growth is there.

ii. Value unlocking of Rs 951 cr, 18%+ of market cap of Rs 5247 cr

Divestment of overseas JV with a valuation of around Rs 1000 cr. planned in FY25. 80% of stake will be divested, bringing in Rs 800 cr which is 18% of current market cap of Rs 5,247 cr. Additional assets worth Rs 151 cr to be sold.

Roughly, I can say we were estimating for 100% addition is around INR1,000 crores. But as we have mentioned that we are diluting around 80%.

The Board has approved sale of Non-Core Assets (land, building & plant, equipment etc.) for total value of ₹ 1.25 billion

The Board has also authorised completion of formalities for recently concluded transaction of sale of land and building in the Southern Region for value of ₹ 265 million and expect to complete this transaction in 90 days’ time subject to compliance with local authorities.

9. PAT growth of 40% & Revenue of 16% in 9M-24 at a PE of 19

10. So Wait and Watch

If I hold the stock then one may continue holding on to TIMETECHNO

Coverage of TIMETECHNO was initiated after Q1-24 results. The investment thesis has not changed after a strong 9M-24. The only changes are the delivery of a strong Q3-24 and the increased confidence in the management to deliver a stronger FY24

TIMETECHNO is in them middle of a strong run. It has delivered sequential QoQ growth in its top-line and bottom-line in all the three quarters of FY24.

Management is confident of a strong FY24

With the strong growth in sales of value-added products, composite cylinder LPG and CNG along with the stable core industrial packaging business, we are highly optimistic of a strong performance for the full year.

Margin profile of TIMETECHNO expected to improve and drive PAT growth with increasing contribution of value added products

And given our value-added product has much higher margins as compared to your established product, so it’s share which is currently at 27%, so ideally it per year based on what you are saying per year it should increase by 3%-4% per year for next 2-3 years. Like it can go from 27% right now to 35%-36%.

Substantial EBITDA margin increase which is currently 14% to 16%

The proposed value unlocking will create opportunity in TIMETECHNO. It is expected to be higher than the previously expected value of Rs 800 cr.

We have already closed calendar year '23. We will again talk on the new chapter. Old chapter is closed. We will take the new chapter based on our earning estimation of 2024 because when we are going 10% to 12% and we do not sell for the '21 or '22 EBITDA basis.

11. Or, join the ride

If I am looking to enter TIMETECHNO then

For a PAT growth of 40% and revenue growth of 16% in 9M-24, the PE of 19 looks acceptable.

TIMETECHNO is guiding for 15% revenue growth in FY25 with PAT expected to grow faster than the revenue at a PE of 19 which makes the valuations reasonable.

TIMETECHNO generated Rs 109 cr free cash flow in 9M-24. It is quoting a market cap of Rs 5247 cr. It is available at free cash flow yield of 2% (not annualized) which makes the valuations reasonable.

TIMETECHNO had a net worth of Rs 2,366 cr as of H1-24 against a market cap Rs 5247 cr. It is quoting a price to H1-24 book of 2.1 which makes valuations quite reasonable.

Potential of value unlocking of Rs 951 cr or around 18% of market cap of Rs 5247+ cr. Expecting the value unlocking to take place within FY25.

Proceeds from the value unlocking will be used for debt reduction. and will reduce interest cost by Rs 40 crore. Reduction in interest cost will drive 14% (Rs 40 cr ) PAT growth in FY25 coming over the FY24 expected PAT of about Rs 280 cr.

That will give the benefit of the interest cost which is in the range of Rs. 100 crores will go down to around Rs. 50 crores - Rs. 60 crores.

TIMETECHNO is quoting at 1.05 market cap to FY24 sales. TIMETECHNO is at a market cap Rs 5247 cr against the expected FY24 revenue of Rs 5000 cr

Previous coverage of TIMETECHNO

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer