Talbros Automotive Components: PAT growth of 56% & Revenue growth of 22% in 9M-24 at a PE of 23

TALBROAUTO to deliver 20%+ revenue CAGR for FY23-27. Slowdown in FY25 with 15%+ revenue growth. Roadmap to deliver EBITDA margin of 15-16% & ROCE of 20%+ by FY27 with reasonable debt

1. Auto Component manufacturer

talbros.com | NSE : TALBROAUTO

2. FY17-23: Strong track record of growth

3. Strong FY23: PAT up 24% and Revenue up 12% YoY

Expansion of PAT margin to 8.5% in FY23 from 7.7% in FY22

4. Strong H1-24: PAT up 50% & Revenue up 21% YoY with expansion of PAT margin

5. Strong Q3-24: PAT up 66% & Revenue up 26% with expansion of PAT margin

6. Strong 9M-24: PAT up 56% & Revenue up 22% YoY with expansion of PAT margin

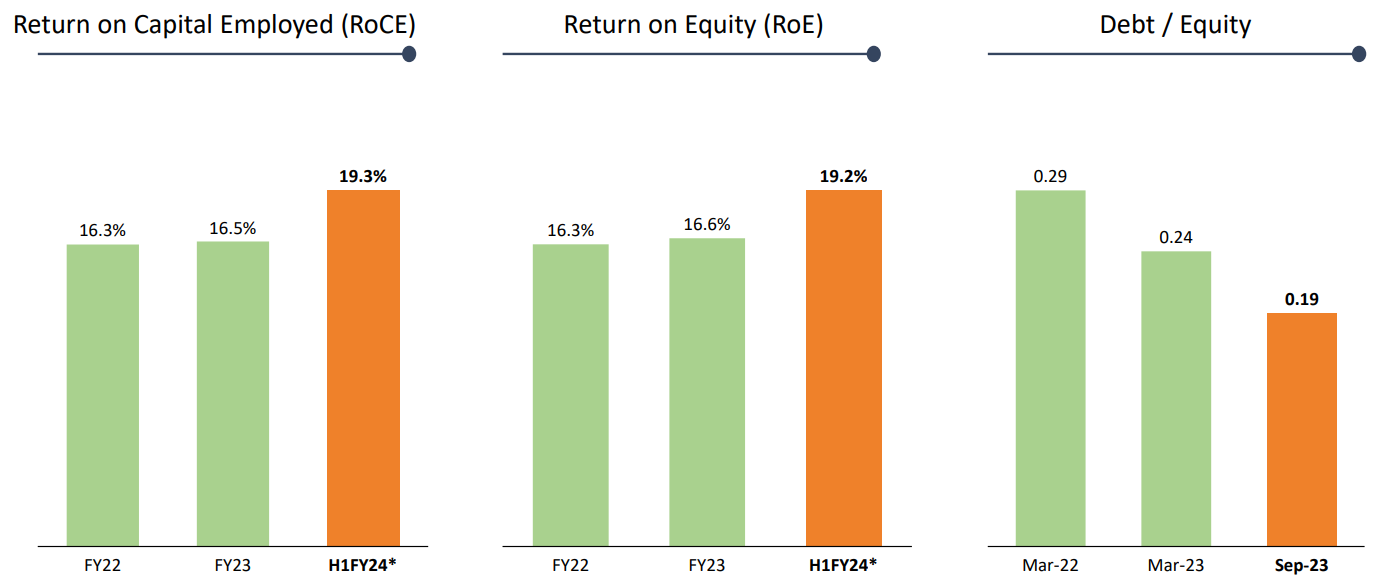

7. Business metrics: Strong return ratios

8. Outlook: Revenue CAGR of 20%+

i. FY23-27: Revenue CAGR of 20%+

Talbros group including JV expected to grow to Rs 2200 cr of which TALBROAUTO would be Rs 1400-1500 cr. This implies a growth of TALBROAUTO from Rs 653 cr in FY23 at CAGR of 21-23%

So Talbros will be around INR1400 crores - INR1500 crores out of that.

ii. FY25: 15%+ revenue growth

Yes, plus we are hopeful that next year also at present we can see a growth of minimum 15% plus. And I will be able to give you in our next earning call which will happen sometime in May.

iii. EBITDA margin 15.6-16% for FY24

it should be in the range of 15.6%, 16% minimum.

iv. Talbros 2.0: Margin expansion, improved ROCE & reasonable debt

9. PAT growth of 56% & Revenue growth of 22% in 9M-24 at a PE of 23

10. So Wait and Watch

If I hold the stock then one may continue holding on to TALBROAUTO

Coverage of TALBROAUTO was initiated after Q1-24 results. The investment thesis has not changed after a strong 9M-24. The delivery of a strong 9M-24 has increased confidence in the management to deliver a stronger FY24

TALBROAUTO is expecting a good Q4-24

We again see a good quarter coming up as well.

Management is on track to deliver as per the roadmap to Rs 2,200 cr by FY27

We are assure of achieving our group sales target of INR2,200 crores by FY '27, of which 35% export -- will be from export. This will come from the U.S., the U.K., Europe as well as Japan.

Revenue visibility is strong given the order book.

This order will be executed over the next 4-5 years, but we are happy to announce that of this INR980 crores order book, INR415 crores of orders came from exports and INR475 crores of orders are directly for passenger vehicles in the EV space, both for the domestic and the export market. So almost 45% of the order book is for EV.

New orders are to be announced by end of Q4-24

We have received some orders. We are waiting for some order more to come. When a sizable amount will be there, then we will announce. You need to wait for a couple of months for that, please.

11. Or, join the ride

If I am looking to enter TALBROAUTO then

TALBROAUTO has delivered a PAT growth of 56% and Revenue growth of 22% in 9M-24. TALBROAUTO at a PE of 23 makes valuations quite fair in the short term.

In the medium term, 15% growth for FY25 is a slow down compared to FY24

The long term outlook for 20%+ revenue CAGR for FY23-27 creates opportunity in the stock.

Since the story will play out over the long term, positions in TALBROAUTO can be built over a period of time on bad days.

Previous coverage of TALBROAUTO

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer