Talbros Automotive Components: PAT growth of 50% & Revenue growth of 21% in H1-24 at a PE of 27

TALBROAUTO on a roadmap to deliver Rs 2,200 cr of top-line as group by FY27. TALBROS 2.0 to deliver EBITDA margin of 15-16%, 35% exports & ROCE of 20%+ by FY27 while carrying reasonable debt

1. Auto Component manufacturer

talbros.com | NSE : TALBROAUTO

2. FY17-23: Strong track record of growth

3. Strong FY23: PAT up 24% and Revenue up 12% YoY

Expansion of PAT margin to 8.5% in FY23 from 7.7% in FY22

4. Strong Q1-24: PAT up 46% and Revenue up 20% YoY with expansion of PAT margin

5. Strong Q2-24: PAT up 53% & Revenue up 21% with expansion of PAT margin

PAT up 15% & Revenue up 6% QoQ with expansion of PAT margin

6. Strong H1-24: PAT up 50% & Revenue up 21% YoY with expansion of PAT margin

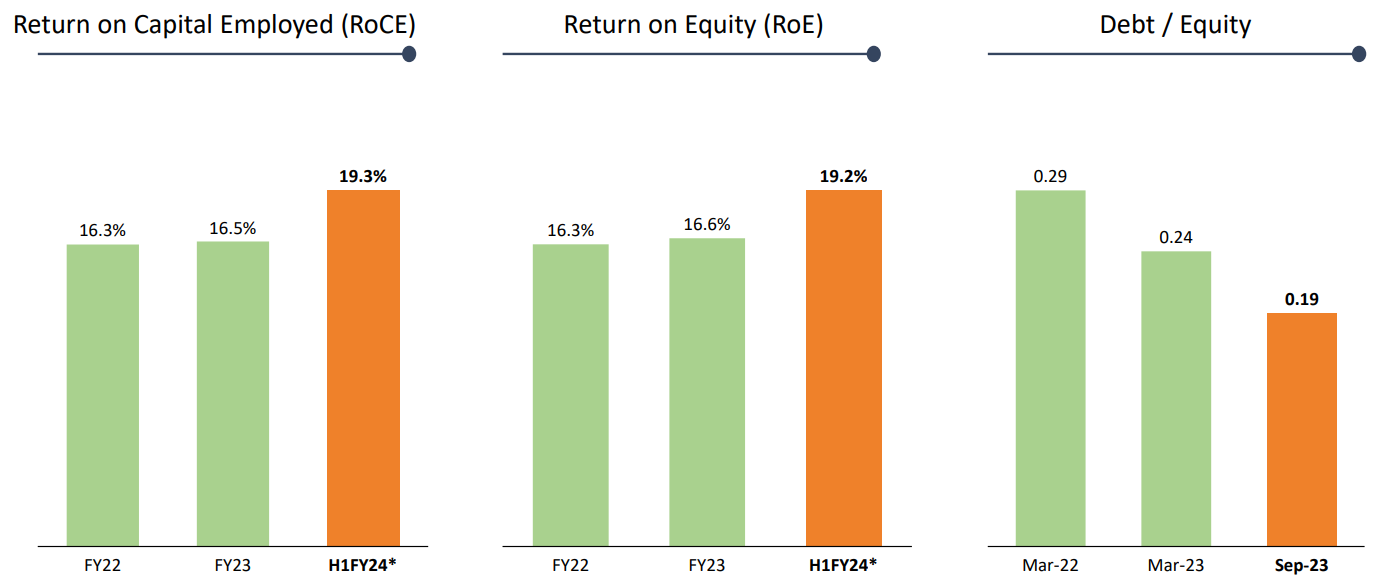

7. Business metrics: Strong return ratios

8. Outlook: Strong PAT growth in FY24

i. Revenue CAGR of 16% for FY23-27 excluding JV

TALBROAUTO expected to grow from Rs 653 cr in FY23 to Rs 1,200 cr (excluding Rs 1,000 from JV’s) by FY27 i.e. deliver a revenue CAGR of 16%. JV’s will add directly to the bottom-line. TALBROAUTO share of PAT from JAV added to TALBROAUTO standalone should lead to a PAT growth higher than 16%

iii. EBITDA margin 15-15.5% for FY24

Going forward, my margin EBITDA should above 15%. We are quite vocal about it. Yes, we should sustain it. Not 15.6% is a little higher in this quarter. But going forward between 15% to 15.5%, it should be there.

iii. Talbros 2.0: Margin expansion, improved ROCE & reasonable debt

9. PAT growth of 50% & Revenue growth of 21% in H1-24 at a PE of 27

10. So Wait and Watch

If I hold the stock then one may continue holding on to TALBROAUTO

Coverage of TALBROAUTO was initiated after Q1-24 results. The investment thesis has not changed after a strong H1-24. The only changes are the delivery of a strong H1-24 and the increased confidence in the management to deliver a stronger FY24

The roadmap to Rs 2,200 cr by FY27 is giving a roadmap worth holding on to the stock from a longer term perspective.

We are assure of achieving our group sales target of INR2,200 crores by FY '27, of which 35% export -- will be from export. This will come from the U.S., the U.K., Europe as well as Japan.

Revenue visibility is strong given the order book.

TACL has received new multi years orders over Rs. 1,000 crores from both, domestic and overseas customers across its business divisions, product segments and JVs. These orders are to be executed over a period of next 5 years covering the company's product lines – gaskets, heat shields, forgings and chassis. These orders will help us increase our share with existing customers and new customers across geographies thereby gaining market share in coming years.

11. Or, join the ride

If I am looking to enter TALBROAUTO then

TALBROAUTO has delivered a PAT growth of 50% and Revenue growth of 21% in H1-24. TALBROAUTO at a PE of 27 makes valuations quite fair in the short term.

In the medium term opportunity in TALBROAUTO may be limited given that top-line growth of 18% is being talked for FY24 which is slower than H1-24

The long term target of Rs 2,200 cr group revenue by FY27 implies TALBROAUTO consolidated revenue growing to Rs 1200 cr (excluding JV revenue) i.e. 16% revenue CAGR for FY23-27. Considering the EBIDTA margin expansion and the share of the PAT from the JV coming to TALBROAUTO will make the bottom-line grow faster than the top-line and hence make the PE of 27 reasonable from a FY27 perspective

Since the story will play out over the long term, positions in TALBROAUTO can be built over a period of time on bad days.

Previous coverage of TALBROAUTO

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades