Supriya Lifescience: PAT growth of 59% & Revenue growth of 29% in 9M-24 at PE of 24

SUPRIYA is on track to delivering revenue of Rs 1,000 cr by FY27 while maintaining EBITDA margin of 28-30%. The revenue CAGR of 20%+ for FY23-27 could provide opportunity for the stock.

1. API Manufacturer

supriyalifescience.com | NSE : SUPRIYA

2. FY19-23: PAT CAGR =23% & Revenue CAGR = 13%

3. Weak FY23: PAT down 41% and Revenue down 13% YoY

4. Strong H1-24: PAT up 27% & Revenue up 24% YoY

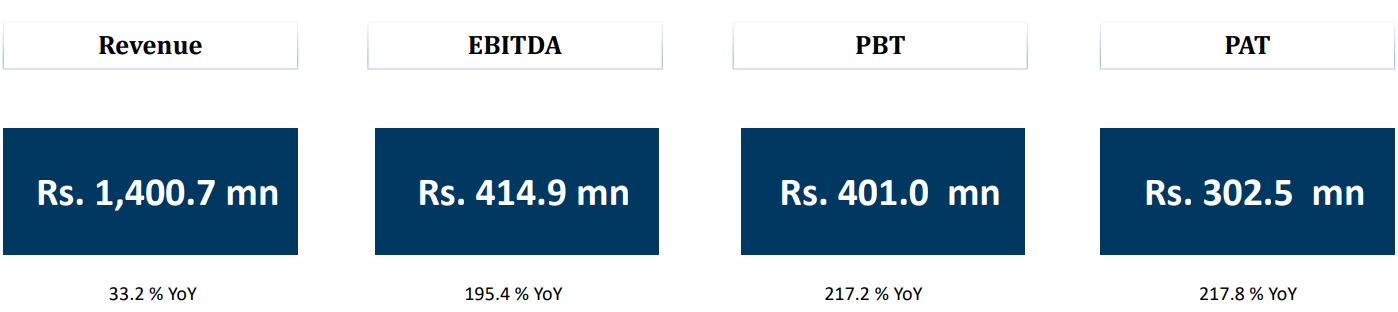

5. Strong Q3-24: PAT up 218% & Revenue up 33% YoY

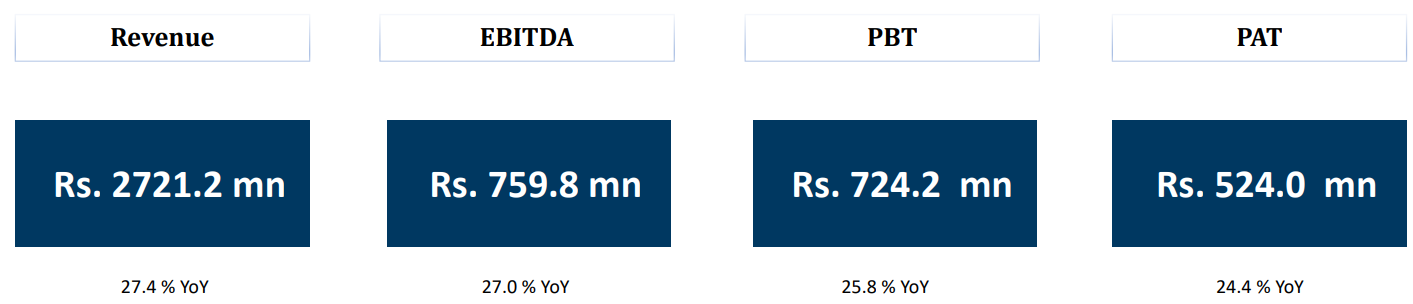

6. Strong 9M-24: PAT up 59% & Revenue up 29% YoY

7. Business metrics: Return ratios declining, still good

One needs to keep a watch on the falling ROCE in FY24

8. Outlook: Revenue growth of 20-25% in FY24

i. FY24-27: Revenue CAGR of 20%+

In terms of revenue growth, we have always maintained that year on year, you can expect upwards of 20% growth from our side. And that is still the number that we would like to maintain for the next three years.

ii. FY24-25: 28-30% EBITDA margin

a sustainable EBITDA margin for us is between 28% to 30%. And that is what we would also like to guide for the future quarters.

iii. FY23-27: 20-24% revenue CAGR

Growing to Rs 1,000 cr by FY27 from Rs 461 cr in FY23, implies a revenue CAGR of 21% which is in the range of 20%+ guided by management and looks reasonable.

So, we have always maintained our guidance that year-on-year we will grow anywhere between 20% to 24%. So, that is the same kind of guidance we would like to give. The revenue growth would be anywhere between 20% to 24%.

Doubling revenue to Rs 1,000 cr by FY27: So, yes, we are still maintaining that for the financial year FY '26-'27. We are still confident that we would be able to achieve the guidance what we have given in terms of revenue.

9. PAT growth of 59% & Revenue growth of 29% in 9M-24 at a PE of 24

10. So Wait and Watch

If I hold the stock then one may continue holding on to SUPRIYA

Coverage of SUPRIYA was initiated after Q1-24 results. The investment thesis has not changed after a strong 9M-24. After a solid Q3-24 confidence in the management is in place to deliver a strong FY24 where revenue and PAT could be expected to beat the all time high of FY22.

The out look for FY25 also looks positive given the management guidance around top-line growth and the increase in capacities by 50% from Q1-25

total capacity will increase from 597 KL to 900 KL by early Q1 FY25

SUPRIYA is working on a clear roadmap for growth

the guidance what we have given in the past, that INR1,000 crores in the next three years still stands. Growth for us will come in three buckets.

The first one is, you know, of course, the top three products which the company sells.

Then there is a basket of about 8-12 molecules which we have said in the past that we are trying to scale up in the regulated market space for which we have now started getting the approval.

Other than this, we have large CMO, CDMO opportunities in our hand. Those will also scale up in the next three years.

11. Or, join the ride

If I am looking to enter SUPRIYA then

SUPRIYA has delivered PAT growth of 59% & Revenue growth of 29% in 9M-24 at a PE of 24 which makes valuations acceptable.

Outlook for revenue growth of 20%+ till FY27 also makes the valuations reasonable.

From a longer term perspective, the growth guidance of the management to deliver a top-line of Rs 1,000 cr by FY27 and grow at CAGR of 20%+ for FY23-27 creates opportunity in the stock. Doubling of the company at a CAGR of 20%+ could create an opportunity for the stock to also deliver 20%+ CAGR returns over the long term.

Previous coverage on SUPRIYA

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer