Supriya Lifescience: PAT growth of 27% & Revenue growth of 24% in H1-24 at PE of 24

SUPRIYA is guiding for delivering a revenue of Rs 1,000 cr by FY27. The revenue CAGR of 20%+ for FY23-27 could provide opportunity for the stock.

1. API Manufacturer

supriyalifescience.com | NSE : SUPRIYA

2. FY19-23: PAT CAGR =23% & Revenue CAGR = 13%

3. Weak FY23: PAT down 41% and Revenue down 13% YoY

4. Q1-24: PAT up 13% and Revenue up 30% YoY

5. Strong Q2-24: PAT up 42% & Revenue up 25% YoY

6. Strong H1-24: PAT up 27% & Revenue up 24% YoY

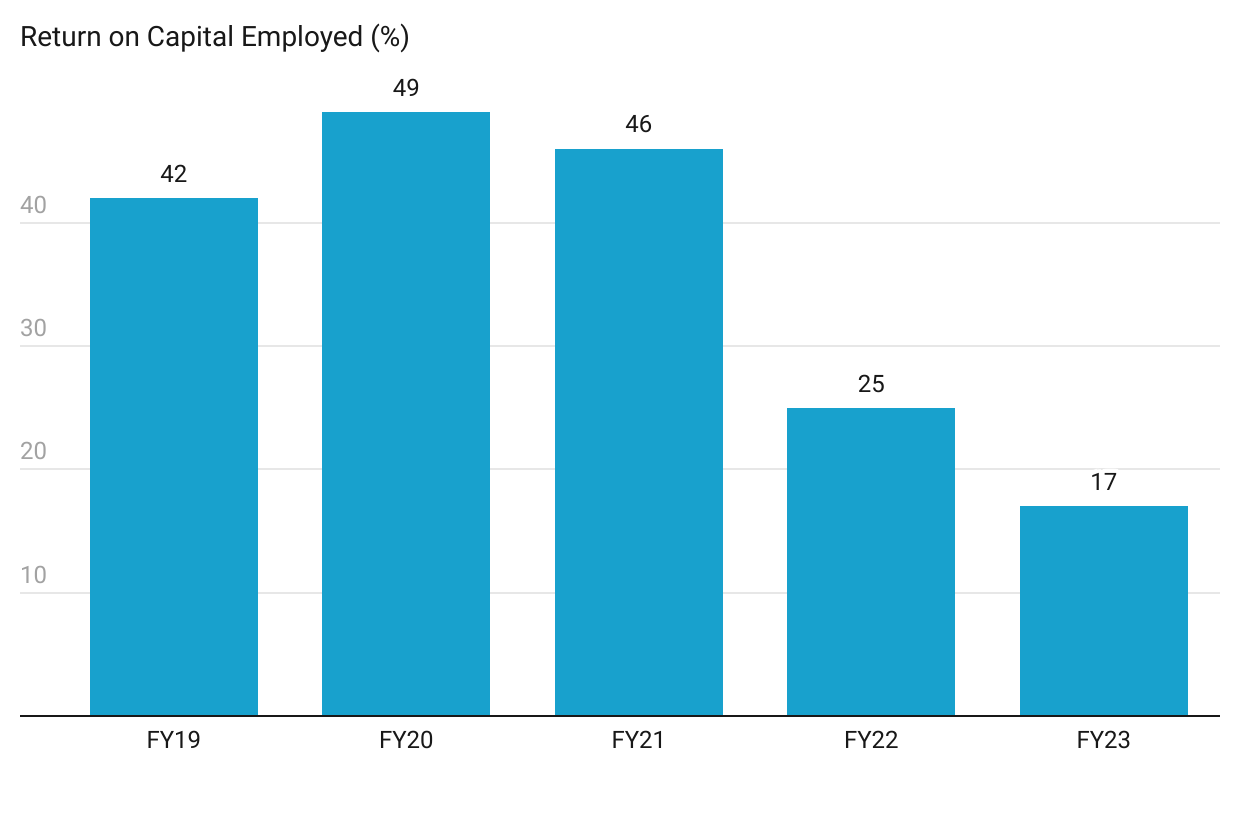

7. Business metrics: Return ratios declining, still good

One needs to keep a watch on the falling ROCE in FY24

8. Outlook: Revenue growth of 20-25% in FY24

i. FY24: Revenue growth of 20-25%

we will maintain an overall around 20% to 25% overall growth on the revenues over the last year number

ii. FY24: 28-30% EBITDA margin

H1 FY23 and EBITDA margins stood at 28% in both the quarters and in both the half year, respectively.

we will maintain our 28% to 30% margin

iii. FY23-27: 20-24% revenue CAGR

Growing to Rs 1,000 cr by FY27 from Rs 461 cr in FY23, implies a revenue CAGR of 21% which is in the range of 20-24% guided by management an looks reasonable.

So, we have always maintained our guidance that year-on-year we will grow anywhere between 20% to 24%. So, that is the same kind of guidance we would like to give. The revenue growth would be anywhere between 20% to 24%.

Doubling revenue to Rs 1,000 cr by FY27: So, yes, we are still maintaining that for the financial year FY '26-'27. We are still confident that we would be able to achieve the guidance what we have given in terms of revenue.

9. PAT growth of 27% & Revenue growth of 24% in H1-24 at a PE of 24

10. So Wait and Watch

If I hold the stock then one may continue holding on to SUPRIYA

Coverage of SUPRIYA was initiated after Q1-24 results. The investment thesis has not changed after a strong H1-24. After a solid H1-24 confidence in the management is in place to deliver a strong FY24 where revenue and PAT could be expected to beat the all time high of FY22.

In the short-term, H2-24 is expected to better than H1-24

Yes, usually second half is slightly better than the first half

The out look for FY25 also looks positive given the management guidance around top-line growth and the increase in capacities by 50% from Q3-24

11. Or, join the ride

If I am looking to enter SUPRIYA then

SUPRIYA has delivered PAT growth of 27% & Revenue growth of 24% in H1-24 at a PE of 24 which makes valuations acceptable without a significant margin of safety.

Outlook for revenue growth of 20-25% till FY25 also makes the valuations acceptable without any margin of safety.

From a longer term perspective, the growth guidance of the management to deliver a top-line of Rs 1,000 cr by FY27 and grow at CAGR of 20%+ for FY23-27 creates opportunity in the stock. Doubling of the company at a CAGR of 20%+ could create an opportunity for the stock to also deliver 20%+ CAGR returns over the long term.

Previous coverage on SUPRIYA

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

Perspectives may change based on evolving understanding of the company.

Focus is on identifying potential stock ideas for long-term market-beating returns.

Content does not constitute explicit stock recommendations.

Investors should conduct thorough stock research and seek professional advice.

Information is for educational purposes and not financial advice or a call to action.