Som Distilleries & Breweries: 50% PAT growth & 62% revenue growth in 9M-24 at a PE of 28

SDBL guiding 36-49% revenue growth & EBIDTA growth of 27-45% for FY24. The capacity expansion in FY25 will deliver 20%+ revenue growth. Promoters are increasing stake for the last 8 quarters.

1. One of the fastest growing beer companies in India

somindia.com | NSE: SDBL

Product portfolio consists of beer, rum, brandy, vodka and whisky

Three key millionaire brands (sales more than 1 mn cases per annum) – Hunter, Black Fort and Power Cool

New products introduced with seasonal themes to increase consumer traction and engagement –flavors of RTD drinks

Beer accounted for 94% of total volumes and 91% of the revenue during 9M FY2024

2. FY19-FY23: PAT CAGR = 32% & Revenue CAGR=20%

FY23 turned profitable after two years of losses

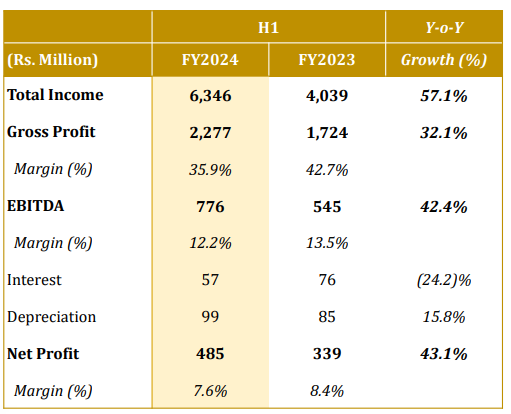

3. Strong H1-24 : PAT up 43% & Revenue up 57% YoY

4. Strong Q3-24 : PAT up 71% & Revenue up 77% YoY

5. Strong 9M-24 : PAT up 50% & Revenue up 62% YoY

6. Strong return ratios in FY23

7. Outlook: 36-49% top-line growth in FY24

i. FY24: Revenue growth of 36-49%

I’ll be more comfortable between the range of about Rs. 1,100 crores to Rs. 1,200 crores for the current year.

ii. FY24: EBIDTA growth of 27-45%

EBITDA Margin to contract to 12-12.5% in FY24 from 12.8% in FY23. EBIDTA Margin of 12-12.5% on a revenue of Rs 1,100-1,200 cr implies expected EBIDTA of Rs 132-150 cr in FY24 vs Rs 104 cr of EBITDA in FY23. This implies EBITDA growth of 27-45% in FY24

I think we should aim at about 12% to 12.5%.

iii. FY25: Capacity expansion to deliver 20%+ revenue growth

We aim to finalize the expansion of Hassan plant in Karnataka by Q1 FY2025

If you consider a 90% capacity utilization, so it can easily give us about Rs. 270 crores of net revenue.

8. 50% PAT growth & 62% revenue growth in 9M-24 at a PE of 28

9. So Wait and Watch

If one holds the stock then one may continue holding on to SDBL

Coverage of SDBL was initiated after Q2-24 results. The investment thesis has not changed after a strong 9M-24. There is confidence that SDBL is on track to deliver Rs 1100-1200 cr of revenue in FY24.

Strong results have been delivered by SDBL in all the 3 quarters of FY24

The underlying business of SDBL is strong and delivering growth across all brands & categories

Capacity expansion in Karnataka plant is providing visibility into 20%+ growth in FY25

Margin contraction needs to be watched out for, but the margin contraction can be absorbed given the growth being delivered by SDBL

SDBL promoters are increasing their holdings for the last 8 quarters, indicating their bullishness on the business.

11. Or, join the ride

If one is looking to enter SDBL then

SDBL has delivered a strong 9M-24 with PAT growth of 50% & revenue growth of 62% at a PE of 28 which makes the valuations reasonable.

SDBL is guiding for 27-45% & EBITDA growth & 36-49% revenue growth in FY24 at a PE of 28 makes the valuations look reasonable.

With 20%+ revenue growth coming in only from the expansion of Karnataka plant, a PE of 28 from a FY25 perspective looks reasonable.

Previous coverage on SDBL

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

Perspectives may change based on evolving understanding of the company.

Focus is on identifying potential stock ideas for long-term market-beating returns.

Content does not constitute explicit stock recommendations.

Investors should conduct thorough stock research and seek professional advice.

Information is for educational purposes and not financial advice or a call to action