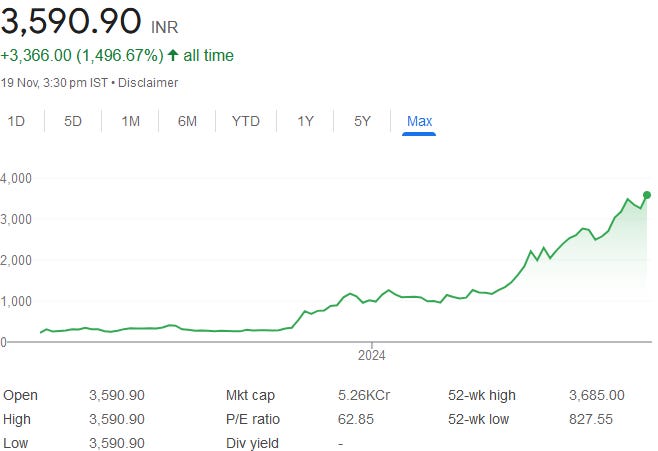

Sky Gold: PAT up 99% & Revenue up 92% in H1-25 at a PE of 49

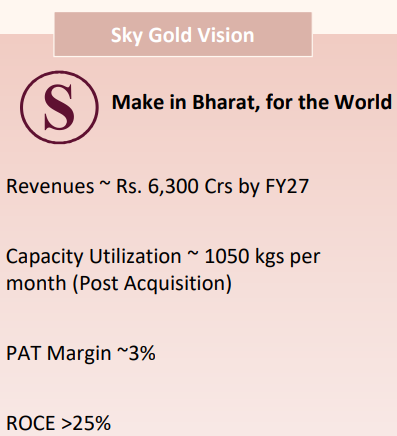

FY25 guidance of 185% growth in PAT & Revenue growth of 89%. Guidance of PAT CAGR of 67% and Revenue CAGR of 53% for FY24-27.

1. Manufacturing of casting Gold Jewelry

skygold.co.in | NSE: SKYGOLD

The Company works on B 2 B model with leading Jewellery Retailers like Malabar Gold & Diamonds, Joyalukkas , Kalyan Jewellers, GRT Jewellers and Samco Gold . The Company also works with large wholesalers . With this Sky Gold products are available at more than 2 ,000 showrooms across India .

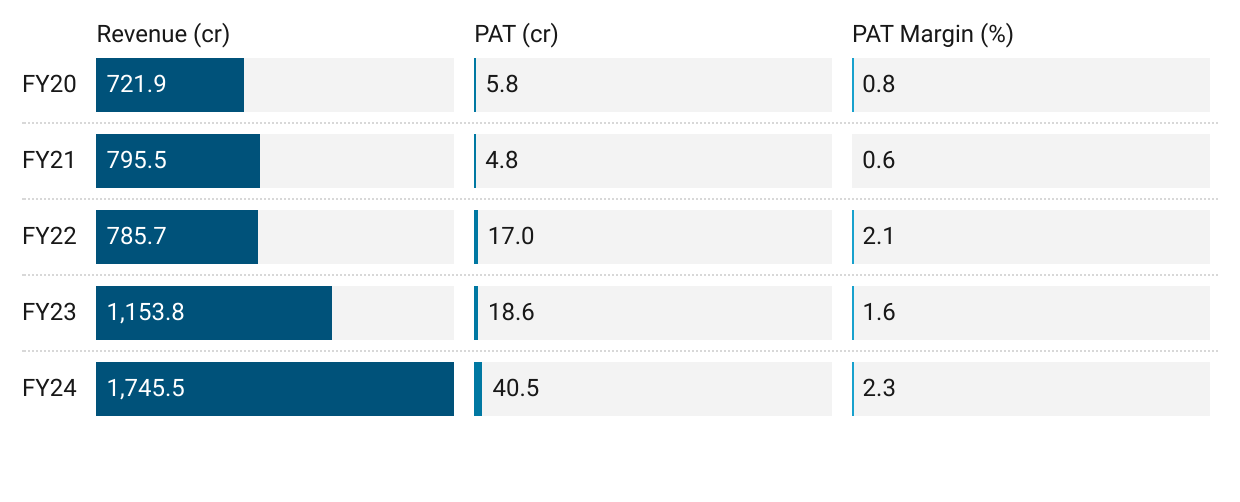

2. FY20-24: PAT CAGR of 62% & Revenue CAGR of 25%

3. Strong FY24: PAT up 118% & Revenue up 51%

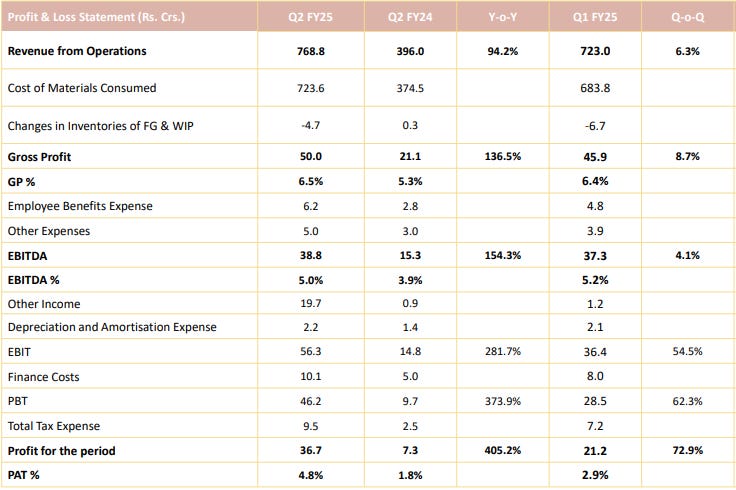

4. Strong Q2-25: PAT up 405% & Revenue up 94% YoY

PAT up 73% & Revenue up 6% QoQ

5. Strong H1-25: PAT up 223% & Revenue up 93% YoY

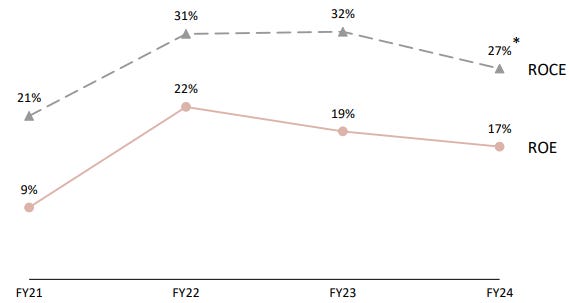

6. Business metrics: Strong return ratios

7. Outlook: PAT growth of 185% & Revenue growth of 89% in FY25

Revenue of ₹3,300 crore for FY25, which includes ₹2,700 crore from core operations and ₹600 crore from recently acquired subsidiaries.

The contribution from subsidiaries was limited in Q2, but is expected to be on a full quarter basis from Q3 onwards.

Gross Margin: Sky Gold aims to achieve a gross margin of 8% through an optimised product mix and exports.

EBITDA Margin: The company plans to maintain a long-term EBITDA margin of 5-5.5%.

PAT Margin: Sky Gold expects to improve its PAT margin to 3.5% by reducing interest costs through increased utilization of gold metal loans (GML).

The company expects to reach monthly production volumes of 375-400 kg by the end of FY25.

Sky Gold also projects reaching 550-600 kg per month by FY26.

i. FY24-27: PAT CAGR of 67% & Revenue CAGR of 53%

Revenue growing from Rs 1,745.5 cr in FY24 to Rs 6,300 by FY27 implies a revenue CAGR of 53%

A 3% PAT margin on revenue of Rs 6,300 cr implies a FY27 PAT of Rs 189 cr up from Rs 40.5 cr in FY24, growing at a CAGR of 67%

ii. FY25: PAT growth of 185% & Revenue growth of 93%

FY25 revenue of Rs 3,330 cr from Rs 1745.5 cr in FY24 implies a 89% growth. PAT increasing from Rs 40.5 cr in FY24 to Rs 115.5 cr (3.5%*3,330) implies a 185% growth in PAT.

8. PAT growth of 223% & Revenue growth of 93% in H1-25 at a PE of 49

9. Hold?

If I hold the stock then one may continue holding on to SKYGOLD

SKYGOLD has delivered a strong FY24 and is following it up with an equally strong guidance for FY25. Based on H1-25 performance, SKYGOLDlooks on track to deliver on the guidance for FY25.

The guidance for execution upto FY27 is equally strong. One can stay in for the long term guidance.

The business momentum continues to be strong as seen from the gold volumes.

The challenge for SKYGOLD is the ability to deliver strong year on year performances. One can stay on as long as we can see SKYGOLD is broadly on track to deliver as per FY27 guidance.

10. Buy?

If I am looking to enter SKYGOLD then

SKYGOLD has delivered PAT growth of 223% & Revenue growth of 93% in H1-25 at a PE of 49 which makes the valuations attractive in the short term.

FY25 guidance of PAT growth of 185% & Revenue growth of 89% at PE of 49 makes the valuations attractive from a medium term perspective.

Outlook for FY24-27 with a PAT CAGR of 67% & Revenue CAGR of 53% at a PE of 49 which makes the SKYGOLD valuations quite attractive over the longer term .

FY24 was the first year of strong performance in the last 5 years. The track record of growth of SKYGOLD has been limited. The FY24-27 guidance would require a long period of strong year on year performances which have not been delivered in the past. Hence entry in to SKYGOLD needs to be done cautiously.

Previous coverage of SKYGOLD

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer