Sky Gold FY26 Result: Profit Up 102%, Strong Guidance for FY27

Guidance of 35% PAT CAGR for FY26-30. SKYGOLD at attractive forward valuation with potential for re-rating of multiples. Opportunity to ~3x based on FY30 guidance

1. Manufacturing of Casting Gold Jewelry

skygold.co.in | NSE: SKYGOLD

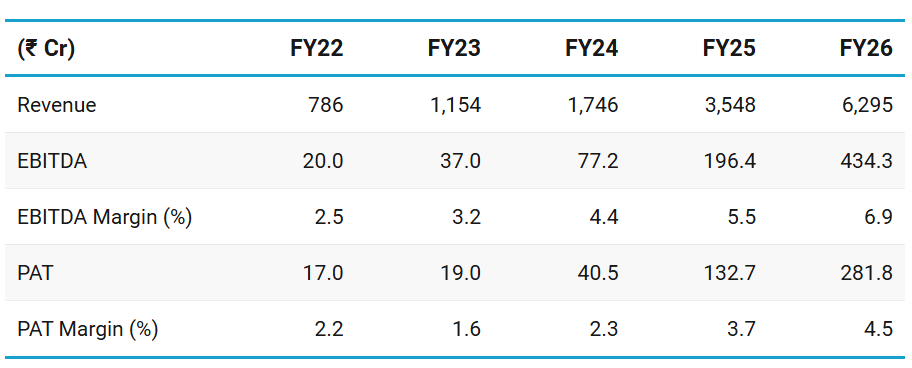

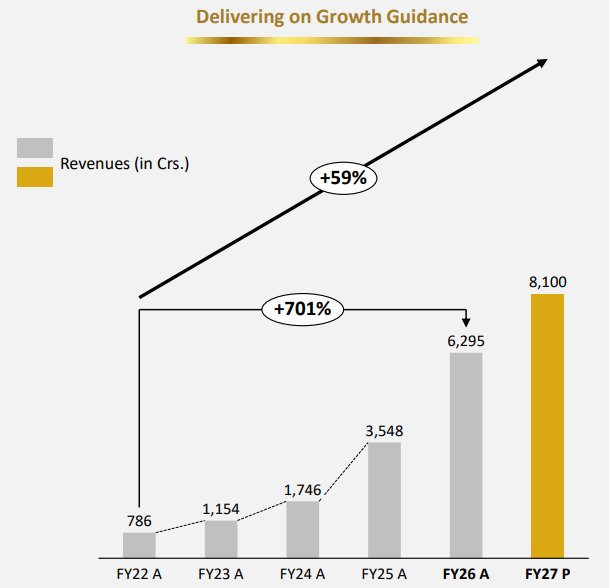

2. FY22–25: PAT CAGR of 102% & Revenue CAGR of 68%

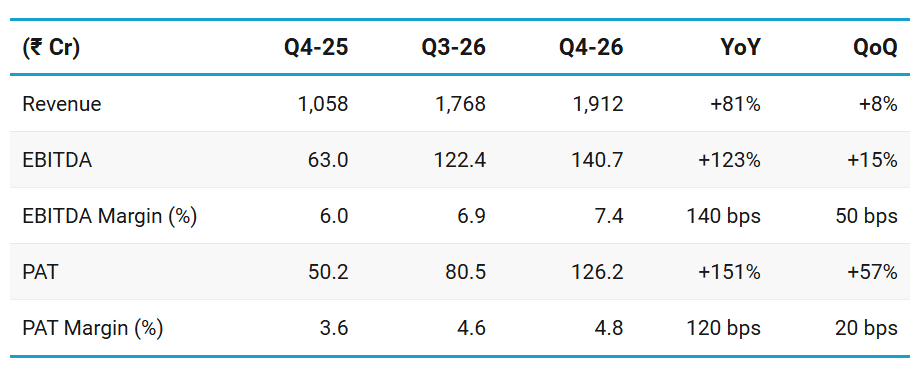

3. Q4-26: PAT up 151% & Revenue up 81% YoY

PAT up 57% & Revenue up 8% QoQ

Key drivers for PAT margin expansion are advanced gold, gold metal loans, and our high margin diamond business, along with operating leverages from scale

4. FY26: PAT up 228% & Revenue up 103% YoY

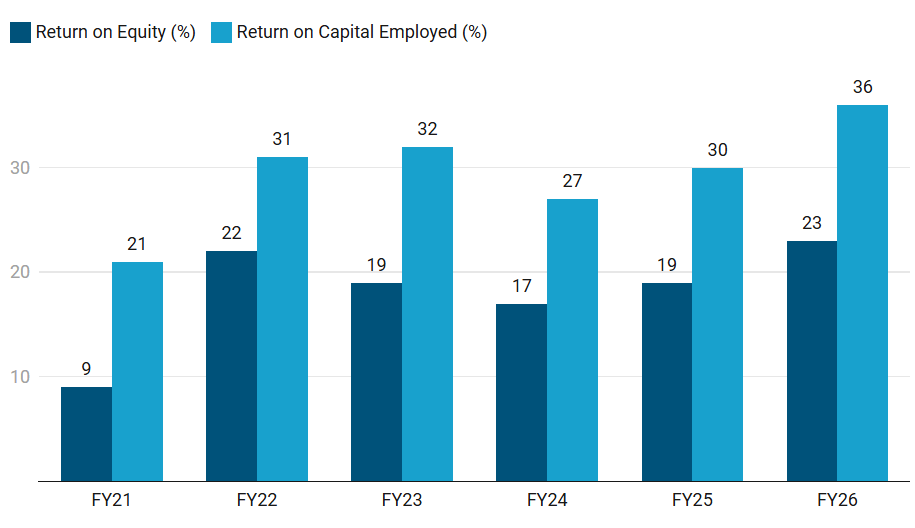

5. Business Metrics: Strong Return Ratios

ROCE guidance of 27%+ by FY30

6. Outlook: PAT CAGR of 35% for FY26-30

6.1 Guidance — Sky Gold & Diamonds

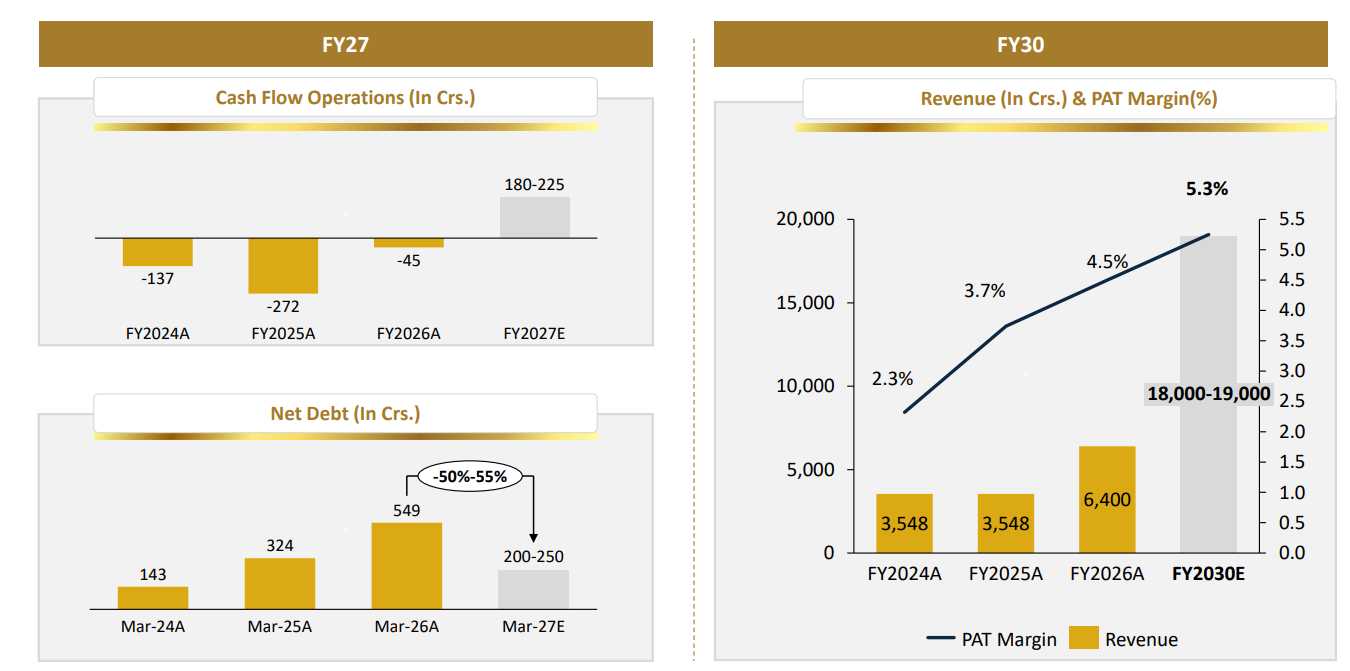

FY27 Guidance:

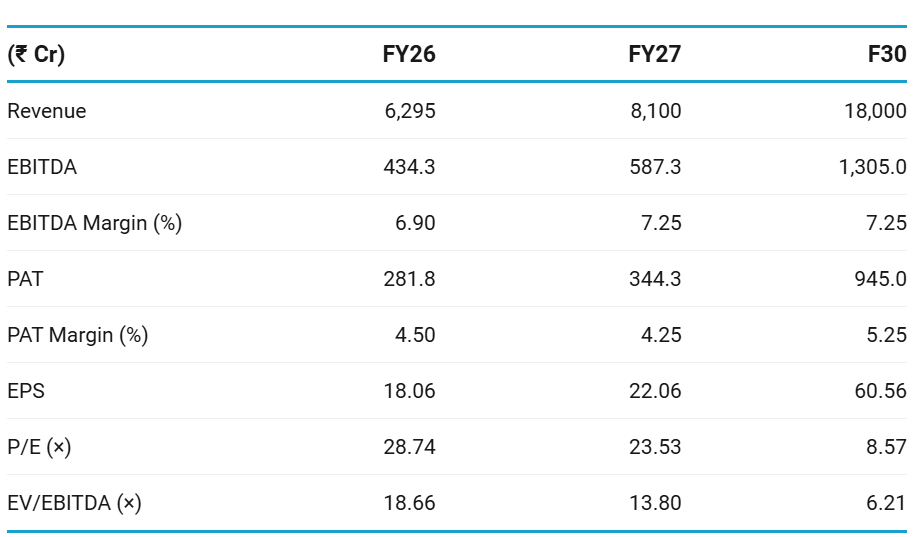

FY27 Revenue projected at ~8,100 crore

EBITDA margin expected in the range of ~7.0-7.5%

PAT margin guided at 4.5% - 4.75%

Focus on capital efficiency, advance gold and margin expansion

Key Growth Levers

Portfolio strengthened through strategic acquisitions, expanding TAM and product depth

Manufacturing footprint expanded to 1,35,000 sq. ft.

Opening of Dubai Office

FY30 Guidance

Revenue expected to be ~₹18,000 -19,000 crore

PAT margin projected to be ~5.25%+, aggregating to ₹ 945 crores

ROCE of 27% +

CFO/PAT of ~20% +

Net debt positive, driven by improvements in the working capital cycle

Advance gold expected to contribute ~30% of volumes by FY30, is 11.5% in FY26

Key Growth Levers

Exports mix to improve

Product mix upgraded with higher design complexity and value-added jewellery, supporting differentiation and margin expansion

Expansion into emerging categories such as 18kt, 9kt, and diamond-studded jewellery

Business Quality by FY30

Balanced domestic and export revenue mix

Improving ROCE, supported by margin expansion and stronger asset turns

Strong corporate governance, consistent positive operating cash flows, and a resilient balance sheet

Revenue Guidance

Targeting a sustainable annual revenue growth of 30% to 35%.

A Shift in Focus: Management explicitly stated they wish to avoid specific long-term revenue guidance going forward because gold price volatility, which is beyond their control, can make top-line figures a “misnomer”. They prioritize “cash in the bank” over “vanity” top-line numbers.

Volume Guidance

Moving away from specific volume targets for the same volatility reasons as revenue

Of the projected 30-35% revenue growth, management expects 27% to 28% to come directly from volume increases.

Aggressively scaling its “advanced gold” business (where they only record job fees as revenue).

Segment grew from 5.7% in FY25 to 11–12% in FY26,

Target of reaching 30% by FY30.

Margin Guidance

PAT Margin Targets:

Conservative 5.25% PAT margin by FY30 — , a 75 bps expansion

Gross Margin Drivers:

Expect expansion of 60 to 90 basis points driven by a better mix of advanced gold and studded jewelry.

Margin Levers:

Advanced Gold: As the share of advanced gold increases, absolute profit and margins improve even if the top-line revenue appears lower.

Interest Cost Reduction: Current interest expenses account for 1.25% of sales. By transitioning to a net debt-free balance sheet by FY30, they see a combined 200-basis-point margin expansion opportunity as interest costs drop to zero.

Value-Added Products: Growth in high-margin 18K, 9K, and diamond-studded jewelry (currently 1.5% of sales) will further bolster margins.

6.2 FY26 Performance vs FY26 Guidance

Delivered Ahead of FY26 Revenue Guidance

Revenue: Ahead of FY26 guidance (₹6,295 Cr vs ₹6,100 Cr guidance)

Margins: FY26 = 4.5% ahead of PAT margin guided at 4.25%+

Volume Targets: (kg per month)

Back on track after lagging in Q2

Q2 FY26: 580 target vs 554 achieved

Q3 FY26: 630 vs 631 achieved

Q4 FY26: 650 ACHIEVED

7. Valuation Analysis

7.1 Valuation Snapshot — Sky Gold

Current Market Price= ₹519.05; Market Cap = ₹8,065.5 Cr

Reasonably priced on a FY27 basis with 24x P/E and 14x EV/EBIDTA for a stock promising 35% CAGR for FY26-30

Opportunity to re-rate to to a 25x+ PE based on FY30 EPS.

Opportunity to ~3×

Sky Gold & Diamonds appears undervalued on FY30 metrics — with re-rating potential as it delivers on FY30 guidance

8.2 Opportunity at Current Valuation

Guidance for FY30

Multi-year visibility: Guidance for FY30 (though far away) provides a longer term view on the stock

Attractive Forward Valuations: The valuations don’t seem to be discounting FY30 guidance

Potential for re-rating of multiples based on execution

Cash-flow turnaround

Management on the Q4 call that Q4 exit revenue run-rate of around ₹7,650 Cr is already close to FY27 revenue guidance of ₹8,100 Cr, so incremental working capital required for FY27 growth should be low.

If CFO turns meaningfully positive in FY27, the market may stop looking at Sky Gold as a “working-capital-heavy business” and start valuing it as a high-growth, cash-generating business.

Debt reduction can create re-rating

50%+ net debt reduction in FY27, driven by land monetization and operational improvement.

This matters because current valuation concern is not just P/E; it is cash conversion and leverage.

If debt falls sharply, the equity story improves.

Advance gold model — can improve ROCE and cash conversion

This reduces inventory funding, lowers receivable intensity, and improves capital efficiency.

Was 11.5% of FY26 volumes, and management targets ~30% by FY30.

Advance gold exit run-rate is already close to 20%, versus annual FY26 mix of around 11–12%.

Even if reported revenue gets deflated because only making charges are booked, PAT, CFO and ROCE can improve. This can make the business higher quality than the historical financials suggest.

Margin expansion opportunity

Management said gross margin improved due to lower gold loss, advance gold, and value-added products such as 18K, 9K, diamond-studded jewellery and co-creation designs. It expects further gross-margin expansion from advance gold and studded jewellery.

Even a 50–100 bps PAT margin improvement on a ₹8,000–10,000 Cr revenue base can materially increase PAT.

Export opportunity

Exports were around 11–12% of FY26 revenue, versus around 6% in FY25

Wants to move toward 20% export share.

Focus markets are UAE/Middle East, Malaysia, Singapore and potentially the UK.

Exports matter because management says export receivable days and ROCE are better than domestic business.

If exports scale to 20%, Sky Gold gets a larger addressable market, better customer diversification and potentially better working-capital quality.

Capacity runway without major immediate capex

Q4 FY26 monthly volume was around 650 kg, while existing capacity is around 1.2 tonnes per month, implying roughly 55% utilization.

Capacity should not be a problem until around March 2028. — supports operating leverage and reduces near-term capex pressure.

A 30–35% PAT compounder with improving ROCE, falling debt, positive CFO and a more asset-light / advance-gold-led model.

8.3 Risk at Current Valuation

Valuation has limited margin of safety in the short-term

Sky Gold is not cheap on FY27 guidance — ff FY27 PAT comes below guidance, valuation quickly becomes expensive.

Margin of safety will start emerging from FY28 as FY27 guidance is delivered

Profit is not converting into cash

Even if FY27 PAT is ₹340 Cr, CFO guidance of ₹180–225 Cr means CFO/PAT may still be only around 52–65%.

That is a big improvement from negative CFO, but still not excellent cash conversion.

FY30 target is ambitious

Strong upside case, but it depends on multiple things going right at once: exports, advance gold, value-added mix, diamond/studded jewellery, unorganized-market expansion, working-capital discipline, and no major gold-price or credit-cycle shock.

Net CFO turns positive.

Inventory and receivables grow slower than revenue.

Debt does not rise materially again despite high growth.

Until then, the P&L deserves credit, but the cash-flow quality deserves caution.

Last coverage of SKYGOLD

Previous coverage of SKYGOLD

https://www.moneymuscle.in/t/skygold

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer