SJS Enterprises: PAT growth of 54% & revenue growth of 36% for H1-25 at a PE of 37

Strong revenue visibility for FY25. 85% of FY25 revenue backed by order book. SJS guiding for growth 1.5 times the underlying industry, with inorganic growth. Strong cash flow generation in FY25

1. Why is SJS interesting?

sjsindia.com | NSE: SJS

SJS is a solid company that generates strong free cash flow and has no debt. It aims to grow 1.5 times faster than the underlying industry while keeping its EBITDA margins around 25%. For FY25, SJS's growth is backed by a strong order book, with 85% of its revenue expected from projects that enhance visibility.2. Premium aesthetics products manufacturer

Wide product range: Decals, appliques/dials, overlays, logos/3D lux, aluminium badges, in-mold decoratives (IMD), optical plastics and lens mask covers for diverse applications

3. FY20-24: PAT CAGR of 47% & Revenue CAGR of 14%

4. Strong FY23: PAT down 29% & Revenue up 18%

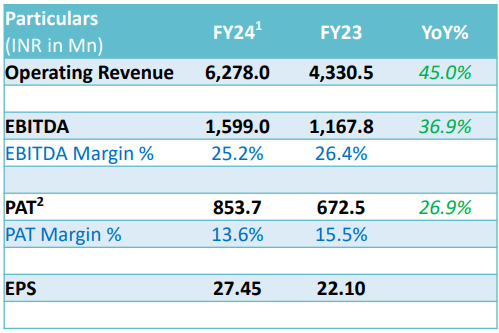

5. Strong FY24: PAT up 27% & Revenue up 45% YoY

6. Q2-25: PAT up 51% & Revenue up 18% YoY

PAT up 3% & Revenue up 2% QoQ

7. H1-25: PAT up 54% & Revenue up 36% YoY

8. Business metrics: Strong return ratios

9. Strong outlook: Revenue growth supported by order book

i. Strategy of organic & inorganic growth in place

Strategy for organic growth over FY24-26

Products: Focus on development of new technologies & advanced products

Key Customers: Growing mega accounts

Exports: Increasing global presence

Capacity Expansion

Inorganic Growth Expected to Boost Organic Growth Trajectory

ii. FY25: Strong top-line growth supported by a strong order book

SJS expects to outperform the underlying industry growth by over 1.5x

Current order book to be executed in FY25 is over 85% of FY25 forecasted revenue

iii. FY25: EBITDA Margin of 25% is sustainable

we continue to drive growth, outperforming the market and maintain an EBITDA margin of close to 25%

10. PAT growth of 54% & Revenue growth of 36% in H1-25 at a PE of 37

11. Hold?

If I hold the stock then one may continue holding on to SJS

SJS has delivered a strong Q2-25 and H1-25, indicating of strong underlying momentum in the business.

SJS continued its growth momentum and delivered the highest-ever quarterly revenue of INR 1,927.9 million in Q2 of FY 2025, again, surpassing industry benchmarks. This growth was primarily driven by the robust growth in the auto segment and the consumer segment and also a strong performance in our exports businesses as well.

SJS is indicating towards a strong outlook for FY25.

SJS to continue its strong financial performance trajectory

SJS expects to outperform the underlying industry growth by over 1.5x on account of :

Premiumisation + Building Mega OEM Accounts + Exports + WPI Acquisition = Higher than industry sales growth for SJS

Current order book to be executed in FY25 is over 85% of FY25 forecasted revenue

Maintain robust margin profile of business for FY25 as we balance higher growth with margin

SJS is pointing to a strong outlook for the next 4-5 years on account of support from exports

We are optimistic that exports is a good growth story for us, not just for H2, but also for the next 4, 5 years.

So when I said that 14.0% to 15.0% of my top line should come from exports, we see that margins are better.

We should be able to target more such large global businesses. While we continue to make good inroads in India, I think diversifying to the export markets because we had a very negligible presence so far.

So there's a huge TAM or untapped market opportunity available for us, and that is what drives our export focus.

12. Buy?

If I am looking to enter SJS then

SJS has delivered PAT growth of 54% and revenue growth of 36% in H1-25 at a PE of 37 which makes the valuations fairly priced in the short term.

SJS generated free cash flow of Rs 66.3 cr in FY24, resulting in a free cash flow yield of 1.8%(not annualized) based on its current market cap of Rs 3,764 crore.

Expectations of strong free cash flow generation implies in FY25 that valuation of SJS are reasonable.

Debt-free status would improve margin and cash-flow generation on account of reduction in interest cost.

I mean we are already generating a large amount of free cash, so we will shore up revenue and by the end of this financial year, we should again have corpus available with strong cash generation abilities.

SJS has successfully repaid a term loan of INR300.0 million, achieving a debt-free status.

We have a vacant plant in SJS Bangalore. And the Board has decided to monetize this asset. Maybe within, let's say, a period of 12 months, we expect the cash inflow

While SJS is open ended and guiding to outperform the underlying industry growth by over 1.5x, a PE 37 looks fully valued from a FY25 perspective

The opportunity in SJS exists over the longer term as new acquisition and entry into exports and non automotive segments via appliance manufacturers and consumer electricals will play out.

On the other hand, the ability to SJS to handle a relatively weak quarter is limited given its PE of 37.

Previous coverage of SJS

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer