Shilchar Technologies: PAT up 46% & Revenue up 59% in Q1-25 at a PE of 47

40-50% revenue CAGR guidance for FY24-26. Strong industry tailwinds to support growth. Order book in place to support FY25 revenue. Undergoing capacity expansion to support growth till FY26.

1. Power & Distribution Transformer Manufacturer

shilchar.com | BOM: 531201

Specializes in custom made transformers for Renewables & Industrial applications

Transformers up to 50 MVA & 132 KV class

2. FY20-24: PAT CAGR of 180% and Revenue CAGR of 54%

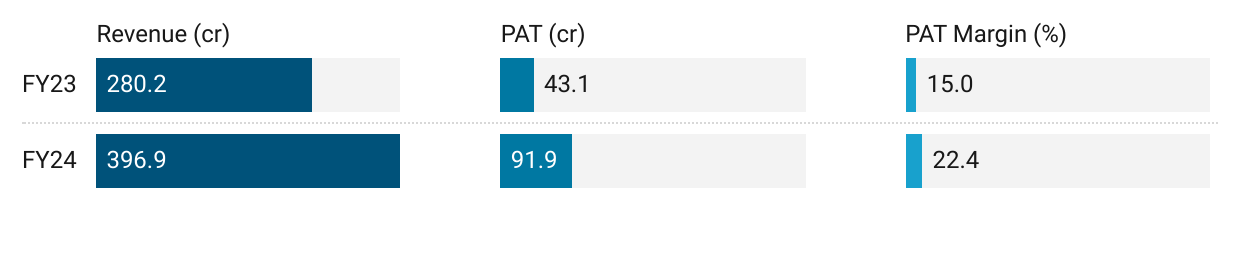

3. Strong FY23: PAT up 207% and Revenue up 56% YoY

4. Strong FY24: PAT up 113% & Revenue up 42% YoY

5. Strong Q1-25: PAT up 46% & Revenue up 59% YoY

6. Business metrics: Strong & improving return ratios

7. Outlook: FY25 to be muted on account of capacity constraints while demand is strong

New capacity coming on-stream in Q2FY25

New capacity utilization to begin from H2FY25, subject to initial teething issues

Geared for further CAPEX if industry scenario remains buoyant

Robust order inquiries from domestic & export clients

i. FY24-FY26: Revenue CAGR of 40-50%

FY24 revenue doubling to Rs 800-900 cr implies a revenue CAGR of 40-50%

We expect the turnover of around Rs. 800 to Rs. 900 crores in two years.

ii. Strong revenue visibility: Order book FY-25

Given the capacity constraints and ramp up of capacity during H2-25, the order pipeline of Rs 550 cr looks sufficient to support FY25 revenue

Order pipeline for FY25 – ₹550 Cr

iii. FY25: Capacity expansion by 88%

8. PAT growth of 46% & Revenue growth of 59% in Q1-25 at a PE of 47

9. So Wait and Watch

If I hold the stock then one can definitely hold on to Shilchar

Coverage of Shilchar was initiated after Q1-24 results. The investment thesis has not changed after a strong FY24 and equally strong Q1-25.

FY25 would be muted as FY24 operations were constrained by capacity. New capacity will come online in H2-25. full impact of the capex will be seen in FY26.

One can stay the course with Shilchar as it has roadmap to double revenue by FY26.

Strong industry tailwinds with renewables driving demand for the next 5 years

We are anticipating demand in renewable energy sector. This is mainly because of the government push government is targeting almost like you know 35 to 40 Gigawatt of the renewable you know projects to be installed each year so this will generate a huge demand of Transformers and I think for next 5 years at this demand should continue

10. Or, join the ride

If I am looking to enter Shilchar then

Shilchar has delivered PAT growth of 59% & Revenue growth of 46% in Q1-25 at a PE of 47 which makes the valuations fully priced at a PE of 47.

Shilchar has a track record of growth, delivering PAT CAGR of 180% and Revenue CAGR of 54% for FY20-24 at a PE of 47 which makes the valuations acceptable from a historic perspective.

The outlook for FY24-26 revenue CAGR of 40-45% at a PE of 47 which makes the valuations acceptable.

The capacity expansion provides support to the growth outlook.

If the momentum continues as delivered in the past, there is significant opportunity in Shilchar. However, the margin of safety is reducing at a PE of 47. The stock would not be able to sustain even a single weak quarter at a PE of 47

Previous coverage of Shilchar

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

I am saying FY 26 revenge at 700 cr

What will be the terminal valuation. With increased capacity, I don’t think they can do more than 700 Cr. Even if we do FY26 700 cr, and 30% margins, that’s 210 ebitda. What multiple will you give at exit. Even in DCF, what will be valuation