Sharda Motor Industries: PAT up 35% & Revenue up 7% in H1-24 at a PE of 16

As a key player in exhaust Systems SHARDAMOTR is benefiting from legislative tailwinds on emissions while preparing for the threat to exhaust systems by EV systems.

1. Auto-ancillary Company

shardamotor.com | NSE: SHARDAMOTR

Exhaust Systems - Indian Market Share of ~30%

Suspension Systems - Indian Market Share of ~10%

Strategic Partnerships

Purem (Formally known as Eberspaecher), Germany (CV exhaust systems)

Kinetic Green, India (EV Battery)

Bestop Inc. USA (Roof Systems)

2. FY19-23: PAT CAGR of 157% & Revenue CAGR of 188%

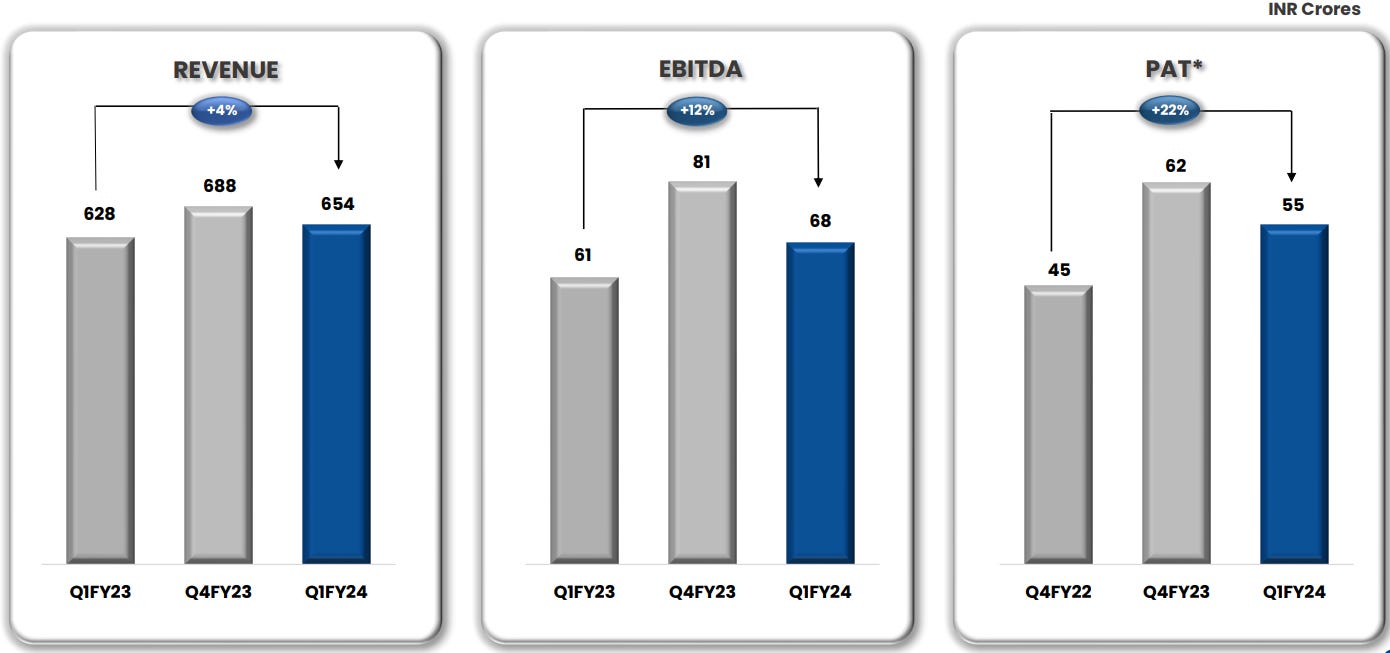

3. Strong Q1-24: PAT up 22% & Revenue up 4% YoY

4. Q2-24: PAT up 47% & Revenue up 9% YoY

PAT up 45% & Revenue up 17% QoQ

5. Strong H1-24: PAT up 35% & Revenue up 7%

Catalyst used in exhaust systems is no longer procured by SHARDAMOTR and explains the impact on top-line

But on the other hand, if a customer really insists that due to business model reasons that they want us to procure the catalyst, then we would, but it would be a strong exception. We are trying our best that for all the new business that we are developing, it would be without the catalyst.

6. Business Metrics: Strong return ratios

Debt free with surplus cash above INR 658 crores as on 30th September 2023

Rs 658 cr cash & end equivalents on a market cap of Rs 3,929 cr implies 17% of market cap is in cash

6. FY24: Strong outlook

i. Strong Tailwinds - Leading to increase in content per vehicle

ii. Optimistic for FY24 & FY25 with positive surprises from suspension business

Without giving any specific numbers, we are very optimistic in terms of the business development in 2024 and '25.

And there have been some surprise, good news business developments type business of suspension, which was not our core focus at that time, will be nominated for a few programs now and actually, all of them are EV programs as well as our international business development cycle is going good.

iii. Potential for inorganic growth in power train agnostic products

For our cash surplus the preference is always utilizing it for M&A opportunities in power train agnostic products but we do not keep any fixed timeline as we want to be very careful with the deal and the valuation specifically because we are on the conservative side and we want to ensure that it would create long term wealth and value for the company as well as shareholders.

7. PAT up 35% & Revenue up 7% in H1-24 at a PE of 16

8. So Wait and Watch

If I hold the stock then one may continue holding on to SHARDAMOTR

Coverage of SHARDAMOTR was initiated after Q4-23 results. The investment thesis has not changed after a strong H1-24. The only changes are the delivery of a strong H1-24 and the increased confidence in the management to deliver a stronger FY24

Top-line growth in H1-24 at 7% looks very weak however, SHARDAMOTR is using gross profit growth as the proxy of volume growth. Gross profit as an indicator needs to be watched

So if you look at gross profit as an indicator growth in gross profit, it generally correlates with volumes. But of course, with various caveats attached to it, I would say, for the time being, it's better to monitor gross profit. We are also monitoring the movement vis-a-vis gross profit and industry volume growth.

Q2-24 was a mixed quarter, weak in terms of top-line but strong in terms of bottom line. We need to keep a watch on Q3 results given that we have a mixed quarter in Q2 and don’t want a trend of weakening top-line. Beyond a point a weakening top-line cannot sustain a strong bottom-line.

Keep a watch for the implementation timelines for TREM5 which is the legislation tailwind forming the core of the investment thesis for SHARDAMOTR

Yes. So there is a likely delay, which I mentioned last time also post-election, but there's no notification of it. The way the OEM planning is going that business nomination has been concluded. Half the customer is already concluded, and the balance half we're expecting to conclude by February. And I think the finite date will come from a government notification, which likely will be post-election only, the way it is looking.

9. Join the ride

If I am looking to enter SHARDAMOTR then

SHARDAMOTR has delivered PAT growth of 35% and revenue growth of 7% in H1-24 at a PE of 16 which makes the valuations reasonable.

SHARDAMOTR generated Rs 155 cr of free cash flow in H1-24 on a market cap of Rs 3,929 cr which translates into a free cash flow yield of 3.9% (not annualized) which makes valuations quite reasonable. The outlook for future free cash flow generation is strong given low CAPEX requirements

Projects in pipeline requiring only incremental CAPEX with high cash generation ability

Rs 658 cr cash & end equivalents as of Q2-24 end on a market cap of Rs 3,929 cr implies 17% of market cap is in cash which makes valuations reasonable

There was an IT raid on SHARDAMOTR in May-23 and we have not heard about it from the management. It is a risk to be kept in mind. There was no earning call in Q4-23. Is it a coincidence that there was no earning call after the raids in May-23.

It is as per what was disclosed it was a search and survey. Our business operations are continuing as per normal and there is no update beyond that and it is just these kind of matters are routine and they take time so there is no litigation per se.

Previous coverage of SHARDAMOTR

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades