Sharda Motor: Growth at a good value

Legislation tailwinds driving increase in content per vehicle and top-line growth while valuations are quite attractive for Sharda Motor

Company Overview

Sharda Motor Industries Ltd is engaged in the manufacturing and assembly of Auto Components and White Goods Components. The company's product portfolio includes exhaust systems, catalytic convertors, suspension systems, sheet metal components and plastic parts for the automotive and white goods industries.

India market share

Exhaust Systems: ~30%

Suspension Systems: ~10%

Share Details

NSE:SHARDAMOTR( shardamotor.com)

Quality: Returns on capital employed

Return ratios indicate an efficient running company generating cash. The adjusted ROCE shows the clear picture of cash and the value in the company.

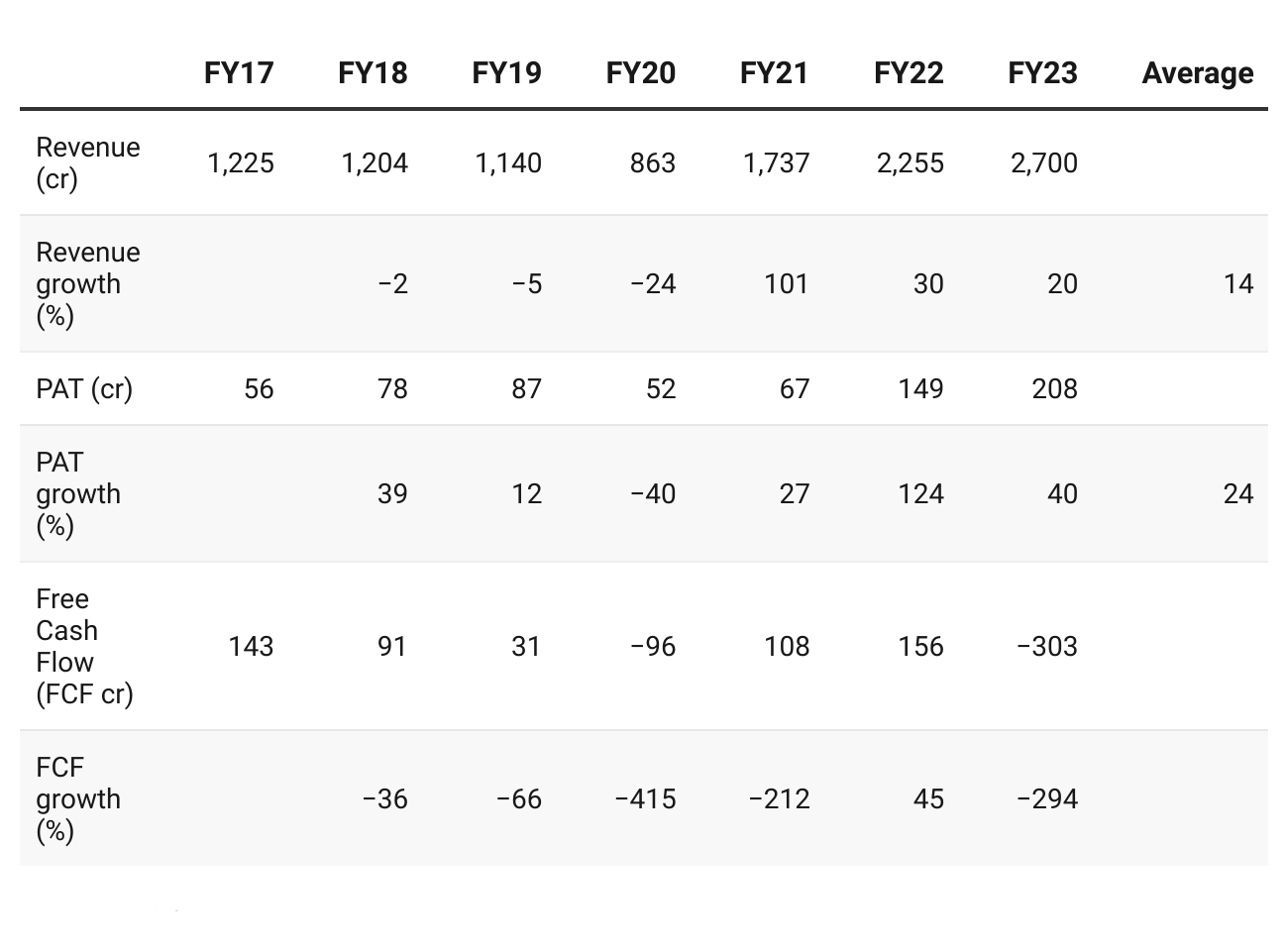

Growth

FY21 to FY23 show the real growth as the numbers are proforma financials after excluding a legacy seating business which was de-merged in FY20 and revenues from the seating operations have been excluded.

Growth Momentum

The growth momentum in the top-line and bottom line is strong from FY20 onward after the de-merger of the seating business.

Outlook

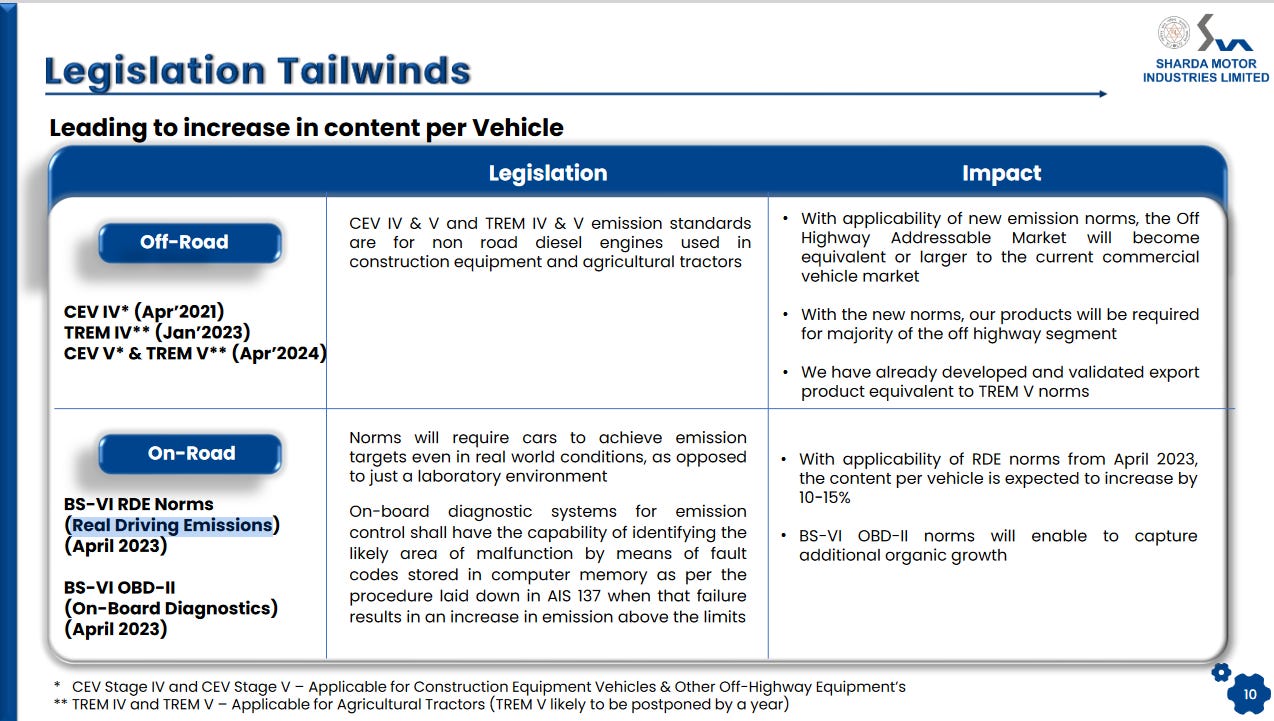

Legislation tailwinds leading to increase in content per vehicle along with Real Driving Emissions (RDE)

We are definitely going to be maintaining our market share maybe even slightly increasing in our products which in general will increase our content per car, LCV, etc., so that is going to be growth driver number one

With applicability of RDE norms from April 2023, the content per vehicle is expected to increase by 10-15%

Revenue Expansion & Visibility

Capitalizing on Eberspaecher JV and implementation of BS VI emission norms

Foray into Electric Vehicle lithium battery manufacturing segment

High margin export markets for sub-components

Margins will be stable around 7-8%

Margins we expect similar margins going forward as well, but no specific numbers that we will give out as guidance.

Surplus cash to be utilized to drive inorganic growth. End of FY23, Sharda Motor had Rs 567 cr of surplus cash on market cap of around Rs 2500 cr i.e. 23% of the market cap is in cash.

Our full focus is and our preference is to utilize this for M&A opportunities for powertrain agnostics products, but there is no fixed timeline as you want to be extremely careful with the cash surplus.

Rs 567 crores including cash, cash equivalence and bank balances.

Red flag

Bharat Seat is related to the de-merged business of Sharda Motor and the issue of bogus billing may raise questions on the quality of the financials reported by Sharda Motor

I-T raids Sharda Motor, Bharat Seat: The Income Tax (I-T) department conducted searches at Relan Group companies — Sharda Motor Industries, and Bharat Seat Ltd. The search has been on since morning in companies' select officials' homes and factories in Chennai, Delhi and Gurugram on bogus billing, the sources added.

So What????

If I currently hold the stock, I may continue holding it based on my past returns, expectations for future returns, and the availability of alternative stock ideas. Sharda Motor is on a growth trajectory based on legislation tailwinds and one needs to keep riding it and ignore the temporary ups and downs. One should be agile in exiting the stock if there is any further development around the red flag.

If I don't currently own the stock, I may want to enter it at the current level.

Efficiently run lender with good return ratios

Legislation tailwinds leading to increase in content per vehicle

Available at a PE of around 12, the company is quite cheap given the top line and bottom line growth rates.

Possibility of inorganic growth indicated by the management

The company is available at market cap less than FY23 revenue

Around 23% of the market cap is cash

The issue is if the red flag can be ignored or not?

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades