Shanti Gold Q3 FY26 Results: PAT Up 128%, On-track FY26 Guidance

Guidance of 60% growth till FY27. Market has not discounted current performance and future capacity expansion of 3x. Trading at very attractive valuations

1. Manufacturing of Gold Jewelry

shantigold.in | NSE: SHANTIGOLD

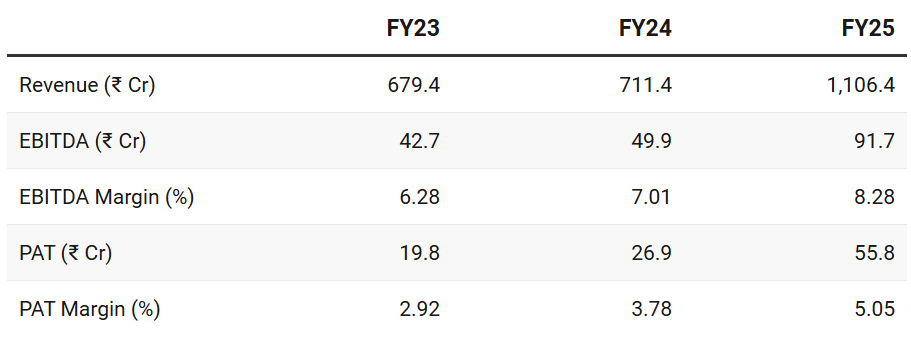

2. FY23-25: PAT CAGR 68% & Revenue CAGR 28%

3. FY-25: PAT up 108% and Revenue up 56% YoY

4. Q3-26: PAT up 128% and Revenue up 110% YoY

PAT down 9% and Revenue up 48% QoQ

Volume Growth: Sold 535 kg of gold, a 31% Y-o-Y increase.

Fueled by the peak wedding and festive season (October–December)

Shift in consumer behavior toward large organized retailers (like Kalyan and Joyalukkas), who are outsourcing more manufacturing to Shanti Gold.

Margin “Normalization”

Q3 results saw sequential dip in margins compared to Q2 FY26.

Lower Inventory Gains: In Q2, SHANTIGOLD benefited from a massive rally in gold prices on stock they bought at low pre-IPO prices.

In Q3, gold prices stabilized, so the “speculative gain” was much smaller.

Product Mix Shift: SHANTIGOLD introduced machine-made plain gold jewellery. It sells faster but carries lower margins than their specialized bridal/CZ-studded collections.

Active Hedging: SHANTIGOLD began hedging its gold positions. While this protects them from price drops, it also limits the “windfall profits” seen in Q2.

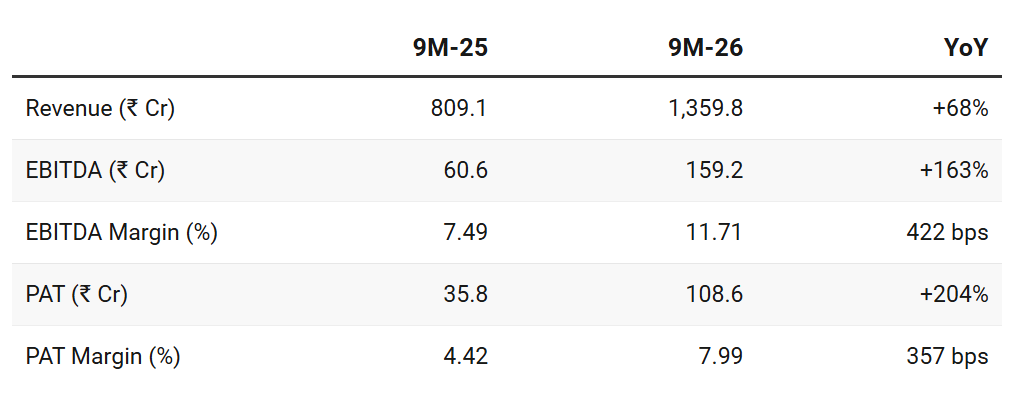

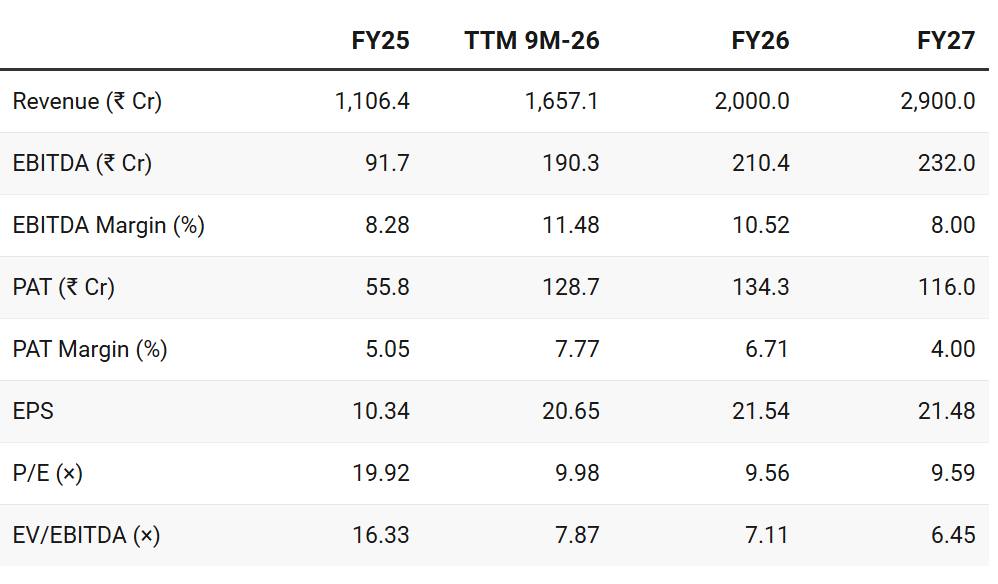

5. 9M-26: PAT up 204% and Revenue up 68% YoY

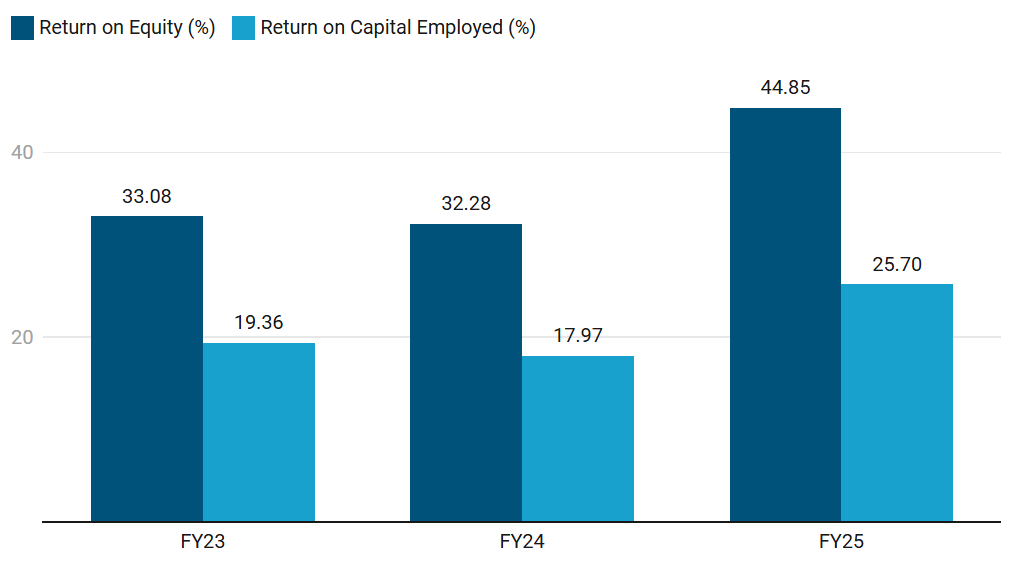

6. Business Metrics: Strong Return Ratios

Very attractive for a manufacturing business that has a demonstrated ROCE of 25.7% (from FY25).

7. Outlook: Solid Growth Guidance till FY27

7.1 FY26 Guidance — Shanti Gold

FY26: I am going to close at 2,000 this year,

FY27: Next year, maybe around INR2,800 crores to INR3000 crores, we will achieve. INR3,000 crores looks more likely.

Financial Guidance and Growth Targets

FY26: Revenue of ~₹2,000 Cr — total gold sales volume ~1,900-2,000 kgs.

FY27: Revenue of ~₹2,800-3,000 Cr — volume growth of 60% to 70%.

Long-term Growth: Historically grown at a CAGR of 40% to 50%, — confident in maintaining this growth trajectory in the coming years.

Margin Outlook:

EBITDA margin 7-8%

Gross margins of 8-10%.

PAT margin of 4% going forward.

Capacity Expansion

Move from 2,700 kg to 7,900 kg total capacity by May 2026:

Jaipur Facility: New facility — will add 1,200 kg pa capacity.

Expected to be operational by May–July 2026.

New Mumbai Facility: New unit is — to add 4,000 kg pa capacity.

Utilization: 75-80% utilization for the existing factory in FY27.

For Jaipur unit — process 800-1,000 kg in the first year of operation

Product Diversification Diversifying its portfolio beyond its core 22-carat CZ-studded bridal jewelry:

Machine-Made Plain Gold: Jaipur facility will introduce machine-made plain gold jewelry aimed at the mass market and affordability-led demand.

Mangalsutra Category: Planning entry into the Mangalsutra jewelry category to participate in this culturally significant and luxury segment.

Geographical and Export Expansion

Domestic Expansion: Have a stronghold in South India,

Targeting expansion in Western and Northern India, specifically in states like Maharashtra, Haryana, and Chandigarh.

International Reach:

Opening a subsidiary office in Dubai to strengthen its global footprint in markets such as the UAE, Qatar, Singapore, and Malaysia.

Export revenue to jump from current 2-4% to 10% by FY27.

Strategic Hedging Policy

Benefited from inventory appreciation by holding gold on its own risk

Strategy to shift towards a Gold Metal Loan (GML) hedging mechanism.

Eliminate the risk exposure to gold price volatility and allow to operate with simple, predictable business margins.

7.2 9M FY26 Performance vs FY26 Guidance

Revenue — On-track ₹2,000 Cr guidance for FY26.

Asking rate looks reasonable

Asking rate of ₹640 Cr in Q4-26 vs ₹637 Cr delivered in Q3-26

EBITDA Margins: 11.71% over-performing against guidance of 7-8%.

However, management has been transparent that the 9M margins were artificially boosted by inventory gains (buying gold low before a price rally).

On-track to deliver FY26 guidance

8. Valuation Analysis

8.1 Valuation Snapshot

Current Market Price ₹206; Market cap ₹1,485.2 Cr

P/E (10×): Attractive — given the growth projected till FY27.

PE is not demanding a high growth rates beyond FY28 to sustain valuations

EV/EBITDA (6.5×): Attractive.

PEG: <0.5→ very attractive

If SHANTIGOLD transitions to its 7,900 kg capacity and stabilizes its PAT at the guided 4% margin, the current valuation provides a significant “Margin of Safety.”

Rerating possible based on FY26 earnings. Re-rating to P/E (15×) easily possible.

Near-term valuation comfort is strong.

8.2 Opportunity at Current Valuation

In a “Value-Growth” sweet spot.

Extreme Valuation Undershoot (Relative to Growth)

Shanti Gold has a PEG ratio of roughly 0.12 to 0.20, which is statistically considered “deep value” or significantly undervalued for a high-growth company.

Future Potential not yet discounted

For a company expanding its capacity by 3x (from 2,700 kg to 7,900 kg), these multiples suggest the market has not yet priced in the successful execution of the new facilities.

Structural Catalysts for Re-Rating: “Re-rating” possible if the following occur:

Capacity Execution: Once the Jaipur and Mumbai facilities go live in May 2026 and show high utilization.

Shift to Hedging: Moving to Gold Metal Loans (GML) will make earnings more predictable and less dependent on “luck” with gold prices. Markets award higher multiples to predictable earnings.

Organized Retail Tailwind: As a B2B supplier to giants like Kalyan, Joyalukkas, and Malabar, Shanti Gold is a “proxy play” on the formalization of the Indian jewellery market.

8.3 Risk at Current Valuation

Corporate Governance & Business Overlap

The promoters (Pankajkumar Jagawat and Manojkumar Jain) also run and own Utssav CZ Gold, another listed entity in a similar line of business.

The Risk: Conflict of interest. Investors worry about:

Order Diversion: Which company gets the most profitable orders?

Resource Allocation: Where is management spending most of their time?

Related Party Transactions: Are funds or resources being moved between the two companies?

Note: Management addressed this in the Q3 earnings call, stating Shanti is for “mass production” and Utssav is “design-focused,” but the overlap remains a psychological barrier for investors.

Execution Risk of “Hyper-Scaling”

SHANTIGOLD is attempting to triple its capacity from 2,700 kg to 7,900 kg in a very short timeframe

Scaling a handmade or even semi-automated jewellery business by ~290% is operationally complex.

Karigar (Artisan) Management: Finding and managing hundreds of skilled artisans.

Quality Control: At these volumes, maintaining the “design leadership” they claim becomes much harder.

Utilization: If they build the 7,900 kg capacity but can only fill 50% of it, the fixed costs (depreciation, salaries, rent) will eat into their already thin 4% margins.

Working Capital & Interest Rate Sensitivity

To generate ₹2,900 Cr in revenue, the company needs to hold massive amounts of gold inventory.

Even though the company’s Debt-to-Equity is low (0.3x), the absolute amount of debt required to fund a 7.9-ton capacity is huge.

If interest rates rise, their Finance Costs (which were ₹19.22 Cr in FY25) could balloon, further squeezing the 4% PAT margin.

Any tightening of credit by banks toward the jewellery sector (a common occurrence in India) could stall their growth completely.

Client Concentration Risk

45% of their sales go to top retail chains like Kalyan, Joyalukkas, and Lalithaa.

B2B manufacturing for large retailers is a “low-moat” business.

If a retailer like Kalyan Jewelers decides to squeeze Shanti Gold on “making charges” or moves its orders to a competitor (like Sky Gold), Shanti’s margins and volumes would take an immediate and severe hit. They are currently “price takers,” not “price makers.”

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer