Shakti Pumps: PAT growth of 9199% & revenue growth of 402% in Q1-25 at a PE of 33

Guidance of 25-30% revenue growth in FY25 with 15% EBITDA margin, supported by a strong order book. Capex plans in place to support doubling of revenue in 3 years

Shakti Pumps is one of the few Indian manufacturers with the competency to manufacture solar and submersible pumps and motors in-house.

The company is the biggest beneficiary under the PM KUSUM scheme and holds ~25% market share in the scheme.

Corporate Structure

Business Segments

2. FY20-24: EBITDA CAGR of 111% & Revenue CAGR of 38%

3. Strong FY24: PAT up 487% & Revenue up 42% YoY

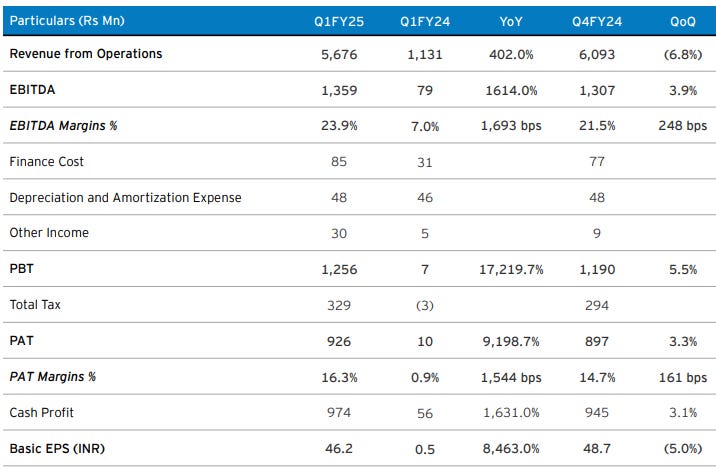

4. Q1-25: PAT up 9199% & Revenue up 402% YoY

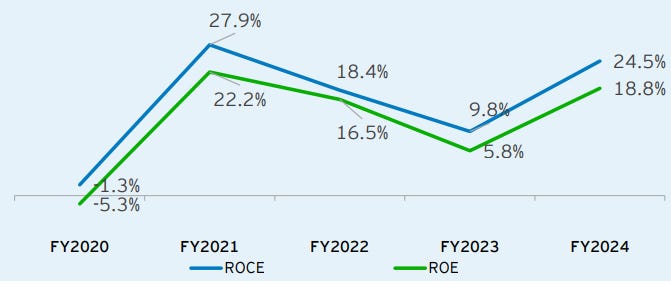

5. Business metrics: Strong & improving return ratios

6. Outlook: Revenue growth of 25-30%

i. FY25: Revenue growth of 25-30%

25% to 30% is our commitment.

This is minimum quote and can be more than this.

ii. EBITDA margins to sustain

EBITDA margin guidance of 15% for FY25 vs achievement of 16.4% in FY24

Our minimum commitment is that we want to work on 15% margin, so the guideline which was 12% is being revised to 3% and made it 15%.

iii. Strong order book providing revenue visibility

We continue to maintain a healthy order book of approximately Rs. 2,000 Crores as on 30th June 2024, which is expected to be implemented in the next 15 months. We are also optimistic about the prospective order inflow from various states in the upcoming quarters

iv. Capex to double revenue potential in 2 years

Q4-24 revenue was Rs 609 cr which is close to the Rs 2,500 cr revenue run-rate which would trigger the capex to double the capacity in 2 years. Doubling of capacity with 25-30% growth could mean revenue doubling in 3 years

The total capacity will be 2x. In our previous calls, we have been telling that as soon as sale of Rs. 2,500 crores come then after that we will do further planning for production capacity, and we see more orders ahead. In 2 years, we will complete our investment and then our capacity will become Rs. 5,000 crores

7. PAT growth of 9199% & revenue growth of 402% in Q1-24 at a PE of 33

8. So Wait and Watch

If I hold the stock then one may continue holding on to SHAKTIPUMP

SHAKTIPUMP has delivered the strongest revenue & PAT in FY24 and followed it by a strong Q1-24 delivering top-line growth with a PAT margin expansion on QoQ

Guidance of 25-30% revenue growth with 15% EBIDTA margin supported by a strong order book is creating a positive outlook for SHAKTIPUMP in FY25

We are expecting H1-25 to be strong as Rs 900 cr of revenues need be executed by SHAKTIPUMP in the first 90-120 days of FY25. The Q1-24 revenue is pointing to the fact that the Rs 900 cr target will be met.

The order book of Rs 2400 cr as of Mar-24 has reduced to Rs 2,000 cr as of Jun-24 end. SHAKTIPUMP management is optimistic about the prospective order inflow from various states in the upcoming quarters. However, we need to keep a watch on the order book.

9. Or, join the ride

If I am looking to enter SHAKTIPUMP then

SHAKTIPUMP has delivered PAT growth of 9199% & Revenue growth of 402% in Q1-25 at a PE of 33 which makes valuations acceptable in the short term.

The FY25 outlook for guiding for 25-30% revenue growth with 15% EBITDA and the support of strong order book providing visibility into H1-25 at a PE of 33 makes the valuation reasonable from the medium term. Q1-25 is in-line with FY25 guidance.

The capex to support doubling of revenue in 3 years at a PE 33 makes the valuations reasonable from the longer term provided the order book is in place to support the growth.

Like our coverage on Shakti Pumps (India) Ltd? Please share it.