SG Finserve FY26 Results: PAT up 58%, Solid FY27 Guidance

PAT CAGR of 30-35%. AUM CAGR of 30-35%. Trading at attractive forward valuations. Opportunity of re-rating of multiples if the guidance is delivered.

Confused about AUM, ROA and ROE in NBFC’s? Gain clarity now.

1. NBFC — Supply Chain Financing

sgfinserve.com | NSE: SGFIN

Business Mix & Portfolio

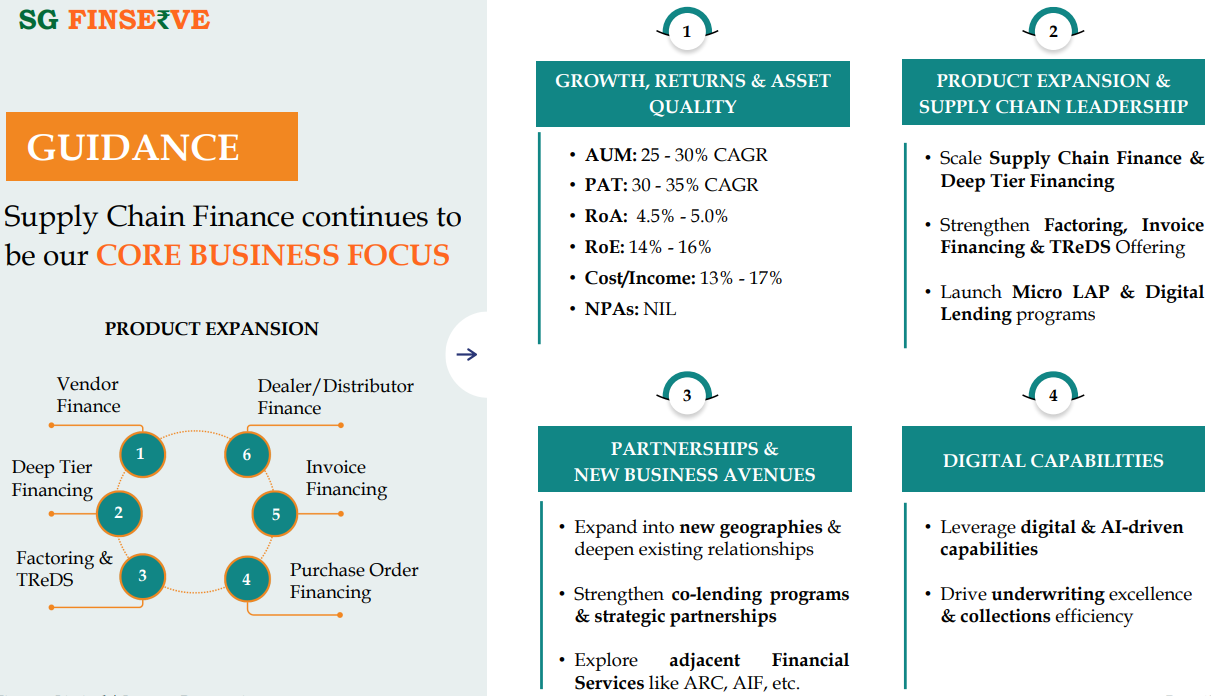

Our core business is supply chain finance and the inherent strength of supply chain finance is that, it has a tripartite relationship between the anchor, borrower, and the financer. Across all the NBFCs and banks who are operating in the supply chain space, the matrix of credit cost remains the similar. For us, the advantage is this: our core business is supply chain, which is more than three-fourths of our business.

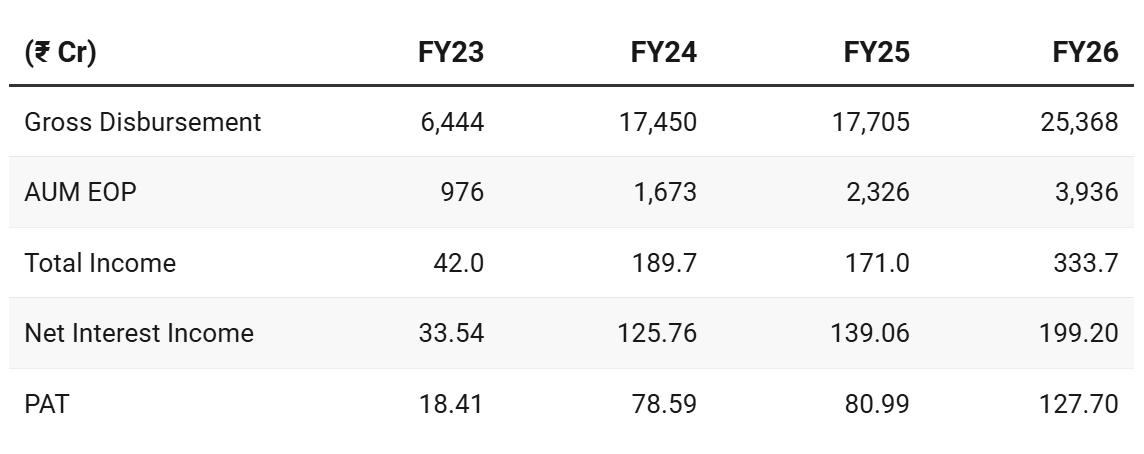

2. FY23-26: PAT CAGR 91% & Net Inerest Income CAGR 81%

FY25: A regulatory pause lending in H1 to comply with Type II NBFC licensing norms muted growth

FY26: Leadership transition (H2) + downward revision in guidance (after Q2 results)

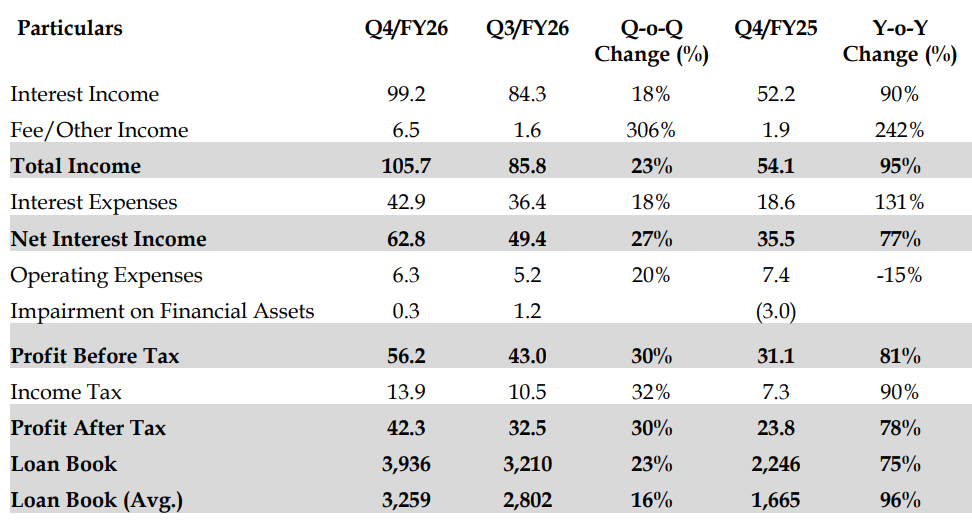

3. Q4 FY25: PAT up 78% & Net Interest Income up 77%

PAT up 30% & Net Interest Income up 27% QoQ

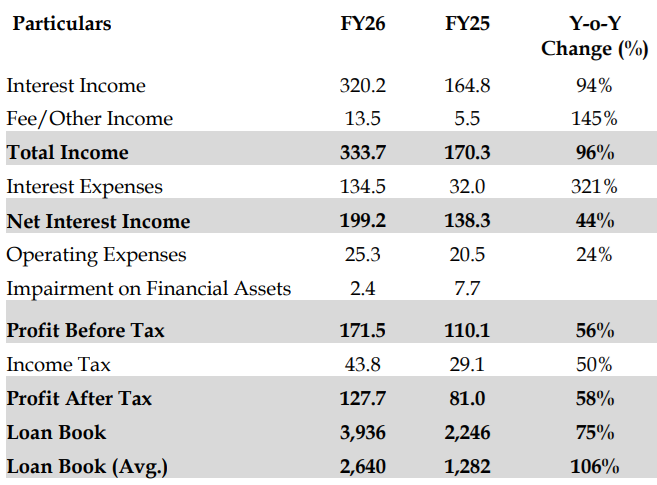

4. FY26: PAT up 58% & Net Interest Income up 44% YoY

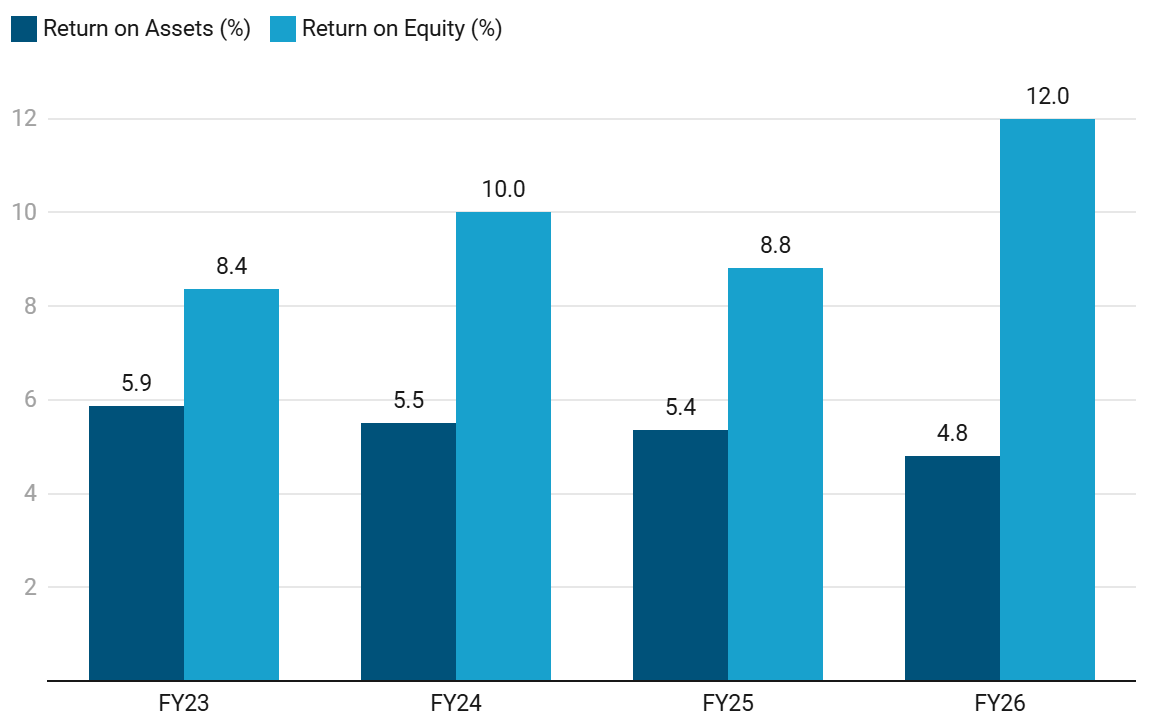

5. Business Metrics: Strong Return Ratios

Management guidance:

ROA: 4.5–5% (sustainable)

ROE: 14–16% target

On the ROA, I think 4.8% is a very healthy ROA. Anything more than this is not desirable, it can go up to 5%. But, ROA will range between 4.5% to 5% depending the leverage levels because if our leverage goes up, the ROA tends to go down, and the ROE tends to go up.

6. Outlook: 30-35% PAT CAGR

6.1 Management Guidance and Future Outlook

FY27 Guidance

For FY '27, our AUM growth may be not 25% to 30%, it will be more. But in a medium to long term, this will be the average of 25% to 30%. Our aspiration on the AUM for FY '27 is around 35%-40% growth.

INR 10,000 crores of AUM we can easily reach in three to four years without being dependent on any fresh equity, because we will accumulate profits also and there is a enough bank lines available and more bank lines will get added. So for INR 10,000 crores AUM with 3x leverage, we are not dependent on any fresh equity.

Q4 FY26 momentum to carry forward into Q1 FY27

On the business momentum, we will continue to grow. The incremental equity we raised in Q4, going to benefit us to maintain this momentum in Q1 and in subsequent quarters.

6.2 FY26 Performance vs FY26 Guidance – SG Finserve

Guidance as of Q3 FY26

FY26 Performance Ahead of a Lowered Guidance

PBT = ₹171.5 Cr in FY26 — ahead of ₹160 Cr target

Leverage = 1.9x in FY26 — in-line with <=2x target

RoA = 4.8% in FY26 — ahead of 4.4% target.

RoE = 12% in FY26 — ahead of 10% target.

One needs to keep in mind that FY26 was revised downwards after H1 FY26 on account of a leadership transition.

The silver lining is that the leadership transition has been smooth based on Q4 FY26 results and the long-term guidance.

Guidance pre-revision

PAT Revision: The full-year FY26 Profit After Tax (PAT) guidance was revised down to approximately ₹120-125 Cr. This is lower than the initial guidance of ₹150-160 Cr (which corresponded to 200 cr PBT)

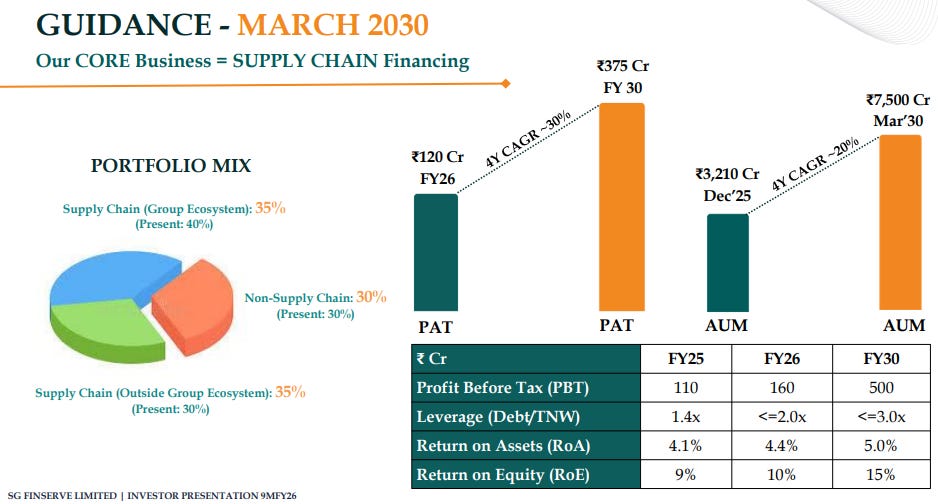

The exit loan book for FY26 is confidently projected to be around ₹3,500 Cr, with a possible positive surprise up to ₹4,000 Cr depending on economic performance in the final three month — toning down of AUM guidance

The company aims for an AUM (loan book) of 6,000 crores by FY27, targeting a PBT of 250 cr (approximately 190 cr PAT)

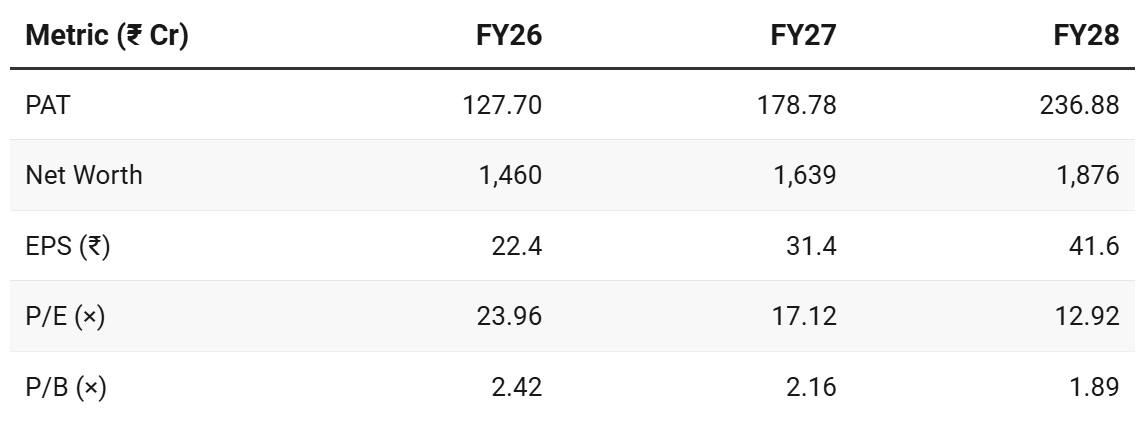

7. Valuation Analysis — SG Finserve

7.1 Valuation Snapshot

Current Price — ₹537

Market cap — ₹3,538.56 Cr

For a stock promising 25-30% long-term AUM CAGR and 30-35% PAT CAGR over the long-term with nil NPA the forward valuations of ~1.9x P/B (FY28) provide an opportunity for re-rating of multiples closer to 3x P/B

7.2 Opportunity at Current Valuation

Strong head-room to grow

Next 3-4 years of growth towards an AUM of ₹10,000 Cr from the Mar’26 AUM of ₹3,900 Cr+ is covered. 2.5x growth in AUM will not require any equity dilution.

The scalability in this space is huge.

Out of top 500 corporates, if we talk about, not even 100 are active in a supply chain space. So there is a huge space for the new anchors to follow the trend of the successful anchors to come and start doing supply chain.

Number two, the anchors who are already doing supply chain, their entire sales is not yet covered. In my understanding, basis back of the hand calculation, only 25% to 30% of their sales is covered under organised supply chain programs. Still there is a lot of room left for those anchors to also deep dive and get their dealers onboarded under the organized supply chain programs.

So the space is humongous. There is no saturation I see in my sight, at least for next 10-15 years.

Valuations are not demanding

The forward valuations are not demanding — have been able to sustain the downward revision in guidance in FY26

7.3 Risk at Current Valuation

Repeated “one-off disruptions”

FY25 disruption

Lending/license issue → business slowdown/reset

AUM temporarily reduced

External + internal shock

FY26 disruption

Leadership change

Guidance cut (conservative stance)

Yet FY 26 execution was strong — Internal transition, not business weakness

FY27 = Make-or-break year

If FY27 has another “one-off excuse” → red flag

One would like to see a a arrowing gap between original guidance and execution.

More predictable execution is required

The impact of this is seen in the stock performance which has gone nowhere and not delivered in-line with the business momentum

Previous Coverage of SGFIN

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer