Senores Pharmaceuticals Q2 FY26 Results: PAT up 130%, On-track FY26 Guidance

Doubling FY26 PAT with 50% growth in revenue. Guidance of 25-30% revenue CAGR & 20-30% PAT CAGR for next 3-5 years. Available at reasonable forward valuations

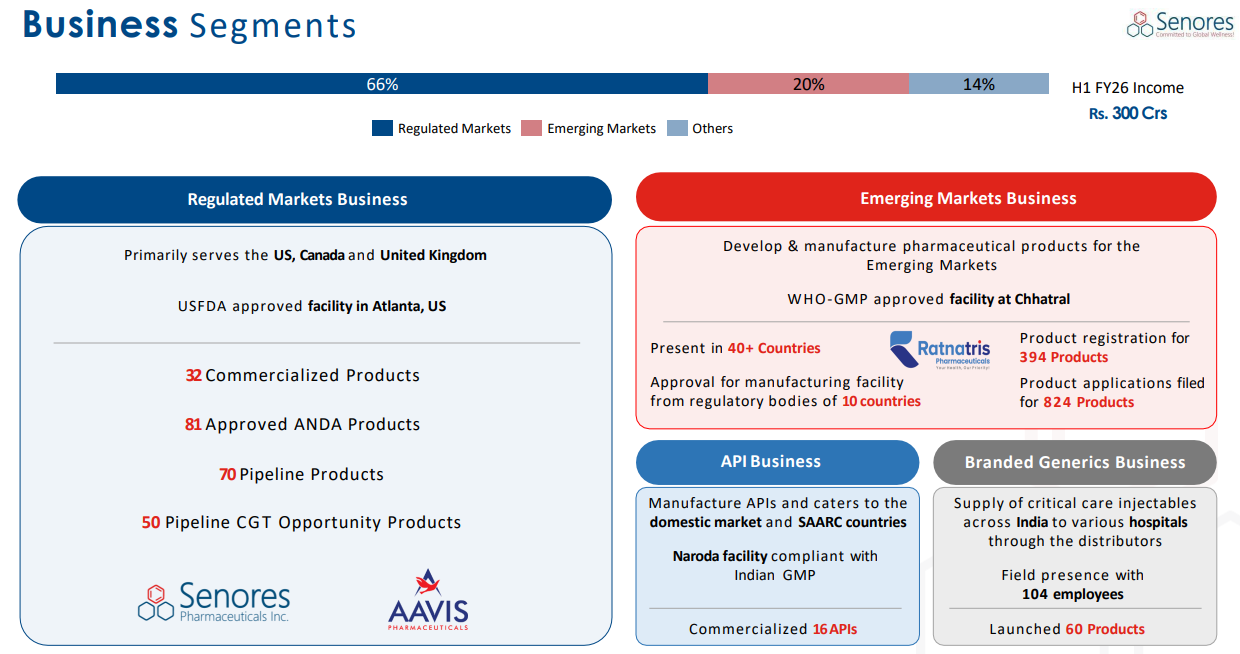

1. Pharmaceutical Company

senorespharma.com | NSE: SENORES

US Manufacturing:

US FDA and DEA-approved facility in Atlanta, US

Insulating them from tariff-related risks

Enabling them to cater to controlled substances and government contracts (BAA compliant)

2. FY25: PAT up 78% & Revenue up 91% YoY

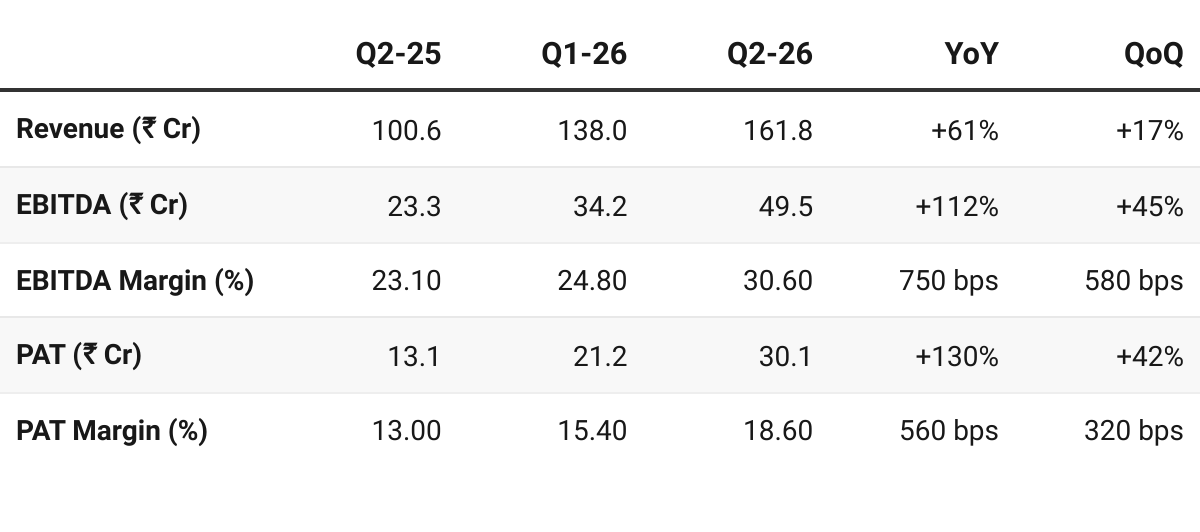

3. Q1 FY26: PAT up 130% & Revenue up 61% YoY

PAT up 42% & Revenue up 17% QoQ

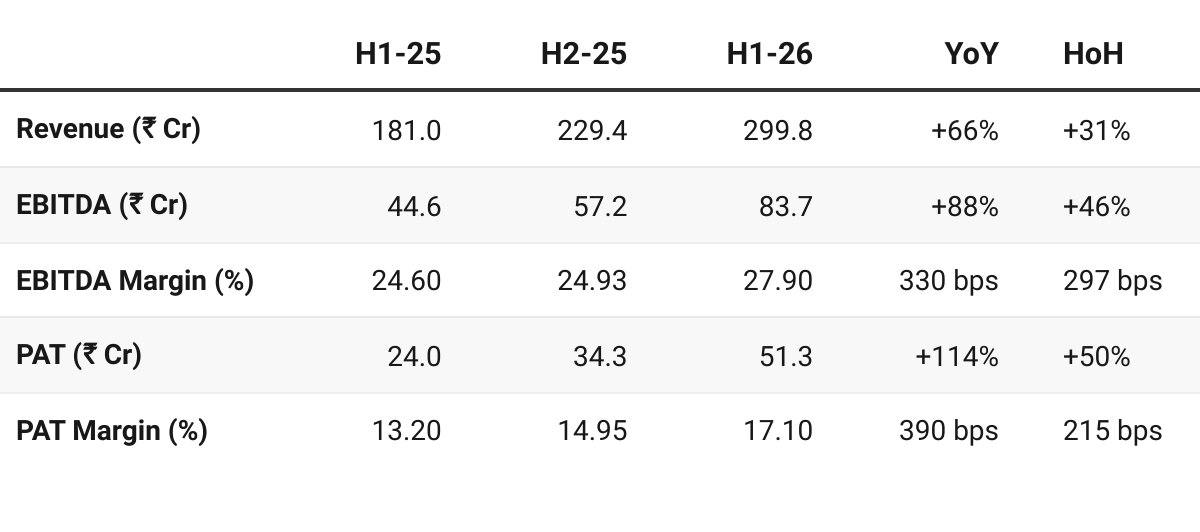

4. H1 FY26: PAT up 114% & Revenue up 66% YoY

PAT up 50% & Revenue up 31% HoH

5. Business Metrics: Reasonable Return Ratios

Funds from IPO in muted FY24 return ratios

6. Outlook: Doubling PAT in FY26

6.1 FY26 Guidance

FY26

Our revenue and profits for the first half of the year are in line with our annual guidance and we remain on track and confident of delivering at least 50% growth in top line and 100% growth in PAT for FY26 over FY25.

Margin — in the similar range what we have achieved in H1

FY27 Onwards

Revenue Growth: So post this year FY 27 I think sustainable growth on a CAGR basis should be between 25 and 30%. That is what we’ve targeted. I mean with a positive launches it this could well exceed but from our internal target perspective — at least 30% CAGR sustainable growth over over next 3 to 5 years is very much visible for us and which will continue to deliver. So that’s that’s what our internal targets have been

PAT Growth: 20 to 30% is what we are looking at from next year onwards

PAT as a percentage will improve by couple of hundred bips that’s what we are looking at

Strategic Investments and Integration

US Capacity Expansion:

Third manufacturing line at the US facility expected to be operational in Q3 FY26

Fourth line is anticipated towards the end of FY26

API Backward Integration:

Projected to get US FDA approval in Q2 FY27

Primary role is backward integration for supply chain protection.

Sterile Manufacturing Facility:

Plans to put up a sterile manufacturing facility in the US — Q2 or Q3 of FY27.

Will handle general injectables and be part of the biologic CDMO/CMO business.

The growth guidance (25-30%) does not include the contribution from this future sterile facility.

Zora Pharmaceuticals (US):

Acquired a 51% interest in Zoraya Pharmaceuticals, a US-based entity.

For vertical integration and expediting market presence for strategic key products by leveraging the remaining partner’s decades of marketing experience and infrastructure.

6.2 H1 FY26 Performance vs FY26 Guidance

On-track FY26 guidance

Usually for us the second half has always been better over last 3 years is trajectory that we’ve seen. So we expect it to be better. I feel we are pretty much on target to achieve those numbers.

Revenue Run-Rate: H1 revenue of ~₹300 Cr and ~₹50 Cr PAT — guidance on-track

Profitability: Strong — as per guidance

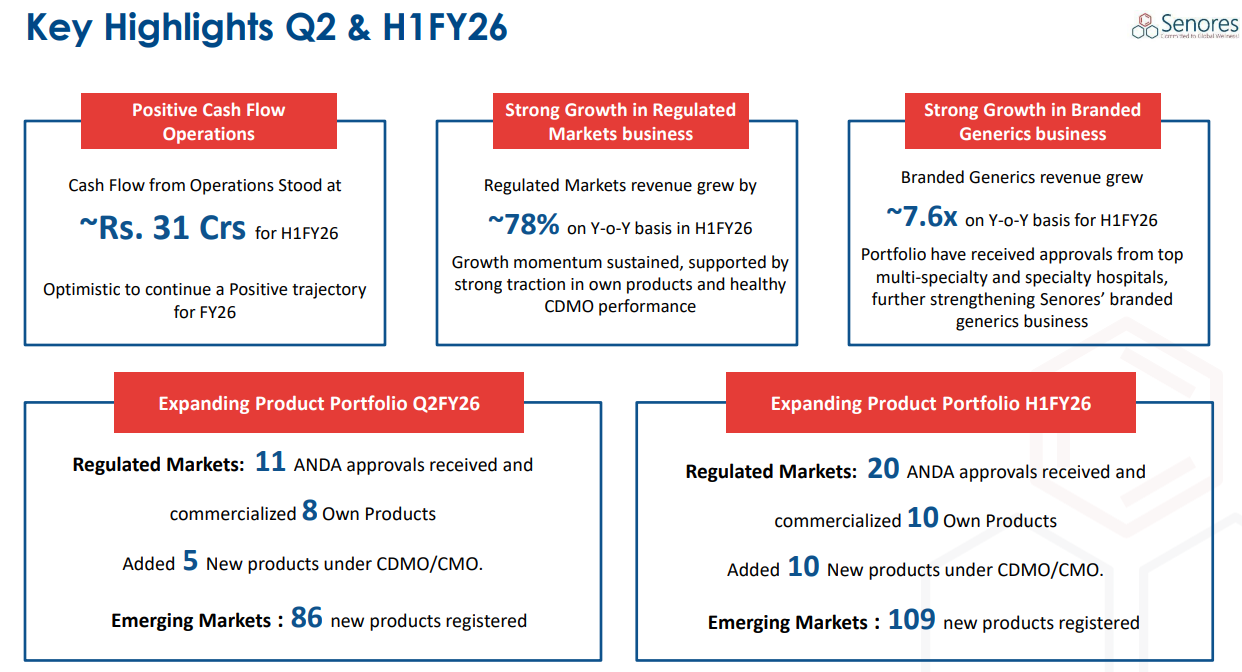

Positive Cash Flow: Turning operating cash flow positive in Q1 and sustaining it in H1-26 strengthens confidence in quality of guidance delivery.

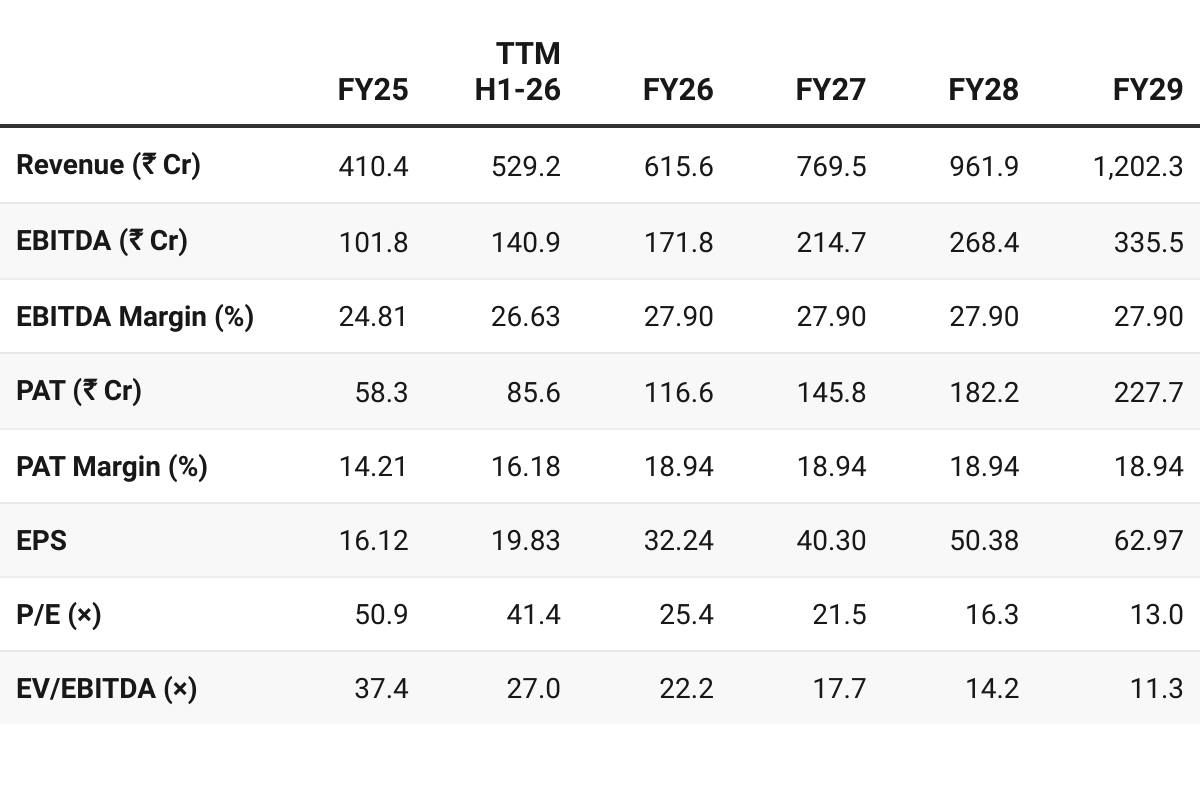

7. Valuation Analysis — Senores Pharmaceuticals

7.1 Valuation Snapshot

CMP ₹820; Mcap ₹3,776.39 Cr

Assumptions:

Revenue growth at 25% beyond FY26 — lower end of guidance

PAT growth in-line with revenue growth

Stable margins

Attractive Forward Valuations

FY27 valuations are undemanding — provide flexibility to sustain a quarter or two where performance is not as per guidance

Fully valued on FY26E and but attractive on FY27E, provided execution sustains with 20-30% CAGR and stable margins. Multiples leave room for re-rating if FY27 is delivered.

7.2 Opportunities at Current Valuation

Strong Growth Outlook:

The opportunity lies in the guidance of 20-30% revenue CAGR from FY27 onwards for the next 3-5 years.

Forward projections are conservative — Growth assumed at the lower end of the guidance

Impact of sterile manufacturing facility not considered in the growth projections

Growth assumptions are strong but not extraordinary

SENORES targets 25-30% growth for the next 3-5 years for the opportunity to play out.

It is not a continuation of the exceptional 50% growth targeted in FY26

FY27 Valuation — P/E of 21× & EV/EBITDA of ~18×

Implies that growth beyond FY26 has not been fully discounted.

8.3 Risks at Current Valuation

Execution Risk:

While FY26 looks on track, delivering 25-30% for the next 3-5 years will require exceptionally consistent performance

All strategic initiatives need to fall in place

However at

Regulatory Dependence: Heavy reliance on USFDA/DEA compliance for Atlanta facility; any adverse inspection outcome is a material risk.

Concentration: ~65% of revenues from Regulated markets; while a strength, it also exposes SENORES to US generics pricing pressures and competitive intensity.

Previous Coverage of SENORES

Help your group stay ahead. Share now!

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer