Rategain Travel Technologies: PAT up 176% & revenue up 84% in 9M-24 at a PE of 73

RATEGAIN expected to double in the next 3 years. FY24 guidance of 69% revenue growth. Management is conservative with an intention to over-delivered on what is promised.

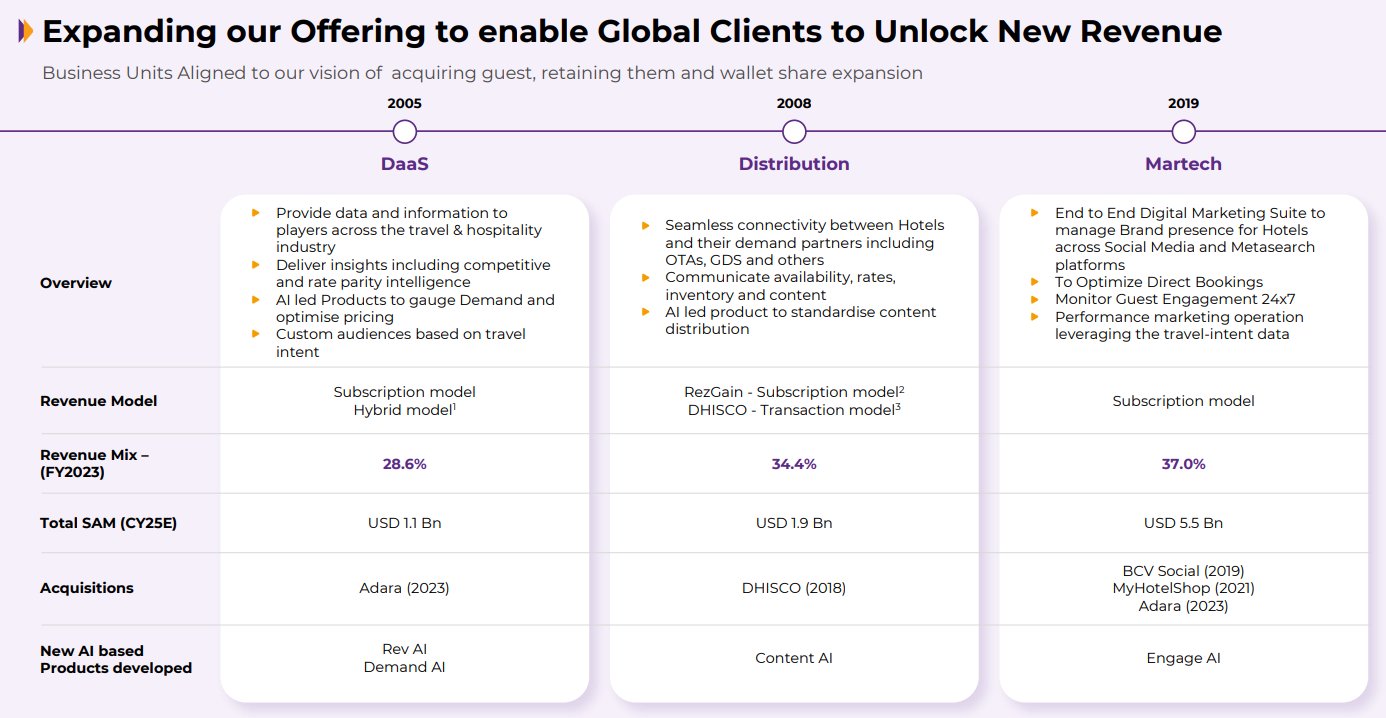

1. India’s Largest SaaS company in hospitality & travel

rategain.com | NSE : RATEGAIN

RateGain Travel Technologies Limited is a provider of SaaS solutions for travel and hospitality, and one of the world’s largest processors of electronic transactions, price points, and travel intent data.

Business Units

MarTech: Helping hotels drive more ROI through digital

Distribution: Reaching the Right Guest

Data-as-a-Service: Enabling hotels, car rentals, and ferries plan their demand and pricing strategy using the automated AI powered pricing recommendation platform as well as a demand forecasting solution

2. Growing at a 50% CAGR FY21-23

Strong profitability metrics supported by improved positive cash flow generated from Operating Activities

3. FY23: PAT up 8X+ on revenue growth of 54%

Revenue for FY23 stood at INR565 crores with a growth of 54%. Margin improvement has been strong as we reported a 17.6% EBITDA margin in our Q4 and 15% for the full year, well ahead of the guidance given at the time of the IPO of 200 to 300 basis points expansion from the 8.3% margin we reported last year.

PAT grew significantly last year to 68.6 crores from INR8.4 crores almost eight times

4. H1-24: PAT up 157% & revenue growth of 84% YoY

5. Q3-24: PAT up 206% & revenue growth of 82% YoY

PAT up 35% on revenue growth of 7% QoQ

6. 9M-24: PAT up 176% & revenue growth of 84% YoY

7. Business Metrics: Strong cash flow generation

As you can see from our numbers, the company is extremely cash-generative. We are doing now north of INR200 crores EBITDA. So – and then the cash on the balance sheet is over, between INR1000 to INR1050. So, we intend to use that pool of capital for any good acquisition that might come about. Our typical size so far has been around INR150 to INR200 crores.

8. Outlook: 69% revenue growth for FY24

i. FY24: 69% revenue growth

given the YTD performance, we are increasing the revenue guidance to close to 69% year-over-year growth, up from 65% growth guidance given on the last earnings call, and up from 55% given at the beginning of the year.

As of Q3-24

In terms of guidance for financial year 2024, we expect to grow around 55% to 58% and end up around INR875 crores to INR890 crores revenue in FY ‘24. On the margin front, we expect to see a 200 basis point expansion year-over-year to 17%. Our Q1 is a soft quarter, both in terms of revenue and EBITDA due to seasonality of the business and also the annual pay review impact starts kicking in in Q1. Our EBITDA margin in Q1 will be around 13.5% and gradually increase to 20% in Q4, delivering an average 17% EBITDA for the year. We expect to deliver a PAT of around 12% and EPS around INR10 per share next year.

As of Q4-23

ii. FY24 guidance on growth and margins to be beaten

Concurrently, given the improved margin performance so far, we estimate EBITDA margin for the year will be close to 19.5%.

As of Q3-24

In terms of guidance for FY’24 for the full year, we're confident of beating the growth guidance given last time. And similarly, we would be looking to exceed the 17% margin guidance given for the full year.

As of Q1-24

iii. 2X revenue in next 3 years i.e. organic revenue CAGR of 26%

Our goal is to double the revenue in the next three years, which implies a CAGR of 26%. So, some of it will be organic, some of it will be inorganic, but organically, you know, we should land between, you know, 20% to 25% for the next three years.

9. PAT growth of 176% and revenue growth of 84% in 9M-24 at a PE of 73

10. So Wait and Watch

If I hold the stock then one can definitely hold on to RATEGAIN

Coverage of RATEGAIN was initiated after Q1-24 results. The investment thesis has not changed after a strong Q3-24. The delivery of a strong 9M-24 and the increased confidence in the management to deliver a stronger FY24

After delivering 84% revenue growth in 9M-24, the FY24 guidance of 69% revenue growth is very conservative.

So, we're not seeing any scaling down in literally any of the business. We just want to be prudent in how we guide the market. As I said that we want to be very, very prudent and diligent in what we are guiding the market so that we over deliver on whatever promises we make.

Q4-24 should be strong

I think Q4 is a strong quarter for us for organic business, but we do have some seasonality for Adara in Q4, where Q3 is much better than Q4. So, again, we are again learning for Adara. So that's why we are being cautious. Nothing else.

11. Or, join the ride

If I am looking to enter RATEGAIN then

RATEGAIN has delivered PAT growth of 176% and revenue growth of 84% in 9M-24 at a PE of 73 which makes the valuations acceptable.

RATEGAIN is guiding for a revenue growth of 69% for FY24 which makes the PE of 73 look fairly valued in the short term.

RATEGAIN is guiding to double in the next 3 years a CAGR of 26% which looks very conservative given the past growth momentum and the possibility of inorganic growth. Out-performance against the conservative guidance would create the upside over the medium to long term in RATEGAIN

we just want to be diligent in what we commit and what we promise and what we deliver. If you see our track record over the last two years on revenue, on margin expansion, we have over-delivered than what we promised. So, we want to be conservative in our commentary and be prudent in delivering on what we promise and that's sort of the narrative we want to maintain.

If the momentum continues as delivered in the past, there is significant opportunity in RATEGAIN however the margin of safety is low. The stock would not be able to sustain even a single weak quarter at a PE of 73

In the short term opportunities in RATEGAIN would be limited. FY25 guidance would create the next short term opportunity.

Previous coverage of RATEGAIN

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

Perspectives may change based on evolving understanding of the company.

Focus is on identifying potential stock ideas for long-term market-beating returns.

Content does not constitute explicit stock recommendations.

Investors should conduct thorough stock research and seek professional advice.

Information is for educational purposes and not financial advice or a call to action.