NCC: Order book 3.6X FY23 revenue, 20% revenue growth guided for FY24 at a PE of 15

Big order book providing visibility for the next 2-3 years. In middle of a strong growth cycle since FY21. Revenue = 40%, PAT = 51%, EPS = 49% CAGR growth for FY21-23

1.NCC Ltd, a leading construction company

ncclimited.com |NSE: NCC

NCC is one of the leading construction companies in India with presence across varied verticals of infrastructure space.

2. Strong growth delivered in the last two years

CAGR growth for FY21-23

Revenue = 40%

PAT = 51%

EPS = 49%

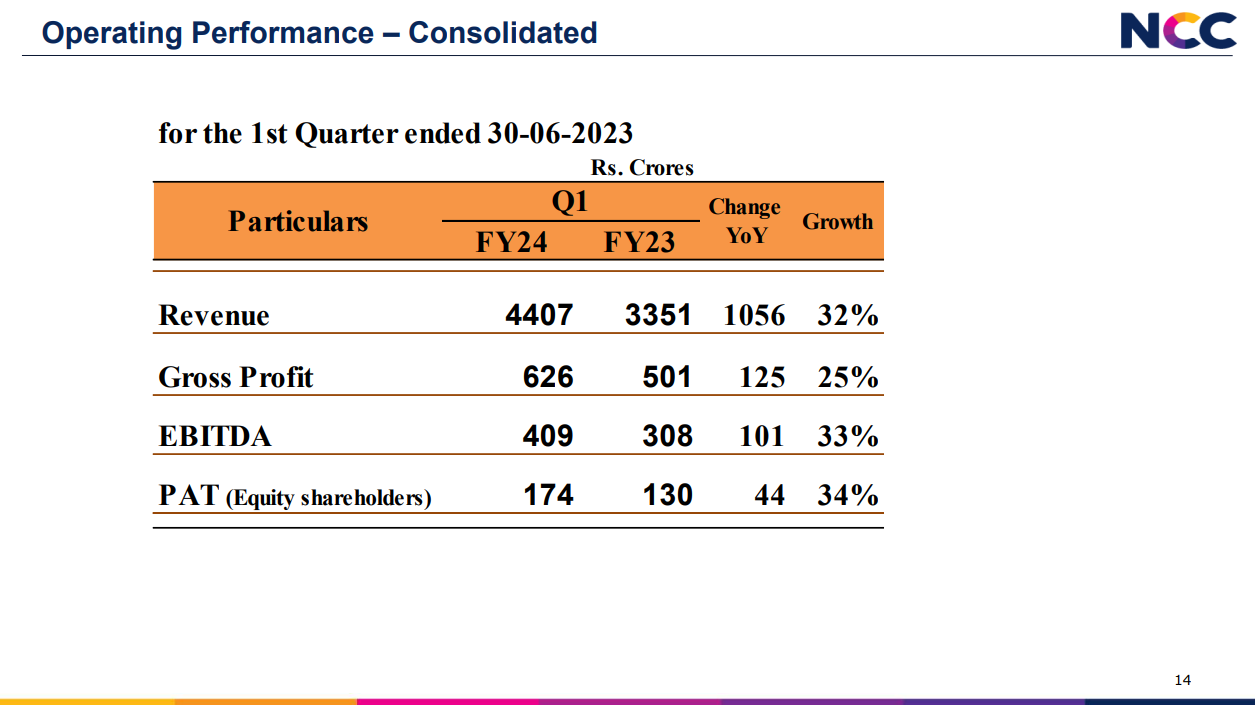

3. Q1-24: Momentum going strong, 30%+ YoY growth

4. High quality of growth and earnings delivered

Return ratios have improved on the back of margin expansion

Strong track record of cash conversion

5. Revenue visibility on the back of a strong order book

Order book = Rs 56K cr as of Jul-23 = 3.6X FY23 revenue .

So, there is a good amount of orders in the pipeline, and the company also secured about 1,919 crore since July month,

6. Outlook for 20% revenue growth in FY24

i. 20% revenue growth in FY24:

32% revenue growth YoY in Q1-24 implies scope for beating the management guidance or else the next 3 quarters are going to be weak.

The UP Jal Jeevan Mission project, 16,500 crores now picked up the progress and report a substantial turnover, nearly 30% in 1st Quarter of financial year '24. We believe that this project reports substantial turnover going forward which ultimately helps the company to reach its guidance of 20% growth given for the year '23-'24.

ii. 15% revenue growth in FY25

15% revenue growth when order book is 3.6X of FY23 revenue is not exciting

Yes, the company plans to maintain that 15% plus the growth in the turnover, and since we have the strong order book at this moment, it is possible to achieve that kind of growth.

iii. Order inflow of Rs 20K cr in FY24

So, based on the momentum what we have, definitely the 20,000 crores plus orders we expect to receive in this year '23-'24.

7. 20% revenue growth in FY24 at a PE of 15

7. So Wait and Watch

If I currently hold NCC, I may continue holding it based on my its performance from FY21 onwards.

One needs to keep a a close watch on the quarterly performance because the management guidance can either be viewed as very conservative or else the management is expecting a weak performance in the next three quarters.

How else can one explain a 20% revenue growth guidance in FY24 after delivering a 31% YoY growth in Q1-24. Additionally the revenue growth slowing from 20% in FY23 to 15% in FY25 could be the management being conservative or being aware of a weak FY25 based on slow order execution.

8. Look before you get in

If I am looking to enter the stock then

For the growth it has delivered in FY21-23 and Q1-24, the PE of 15 looks fair.

Quality of growth is good in term of return ratios and free cash generation.

The management guidance looks a bit confusing on the back of an order book 3.6X of FY23 revenue.

If one is looking in the construction space then one can look at HG Infra Engineering Ltd HGINFRA is smaller than NCC but promising more growth for the next years with better margins and cheaper valuations

Don’t like what you are reading?

Let us know at hi@moneymuscle.in

Will make it better.

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades