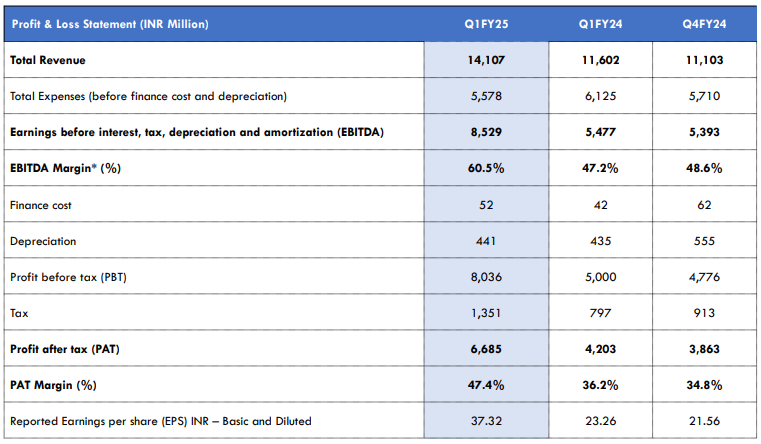

Natco Pharma: PAT growth of 59% & Revenue growth of 22% in Q1-25 at a PE of 16

FY25 PAT growth of 20%. Guiding for 15-20% revenue growth in FY25. Possibility of inorganic growth coming in FY26. Reasonable valuations based on free cash flow yield.

1. Pharmaceutical company

natcopharma.co.in | NSE : NATCOPHARM

Well established player in oncology with brands catering to diseases including breast, bone, lung and ovarian cancer

Focused on complex generics for the US Markets with niche Para IV and Para III filings

Targeting growth in Crop Health Sciences business with state-of-the-art manufacturing facilities for both technical and formulation

2. FY20-24: PAT CAGR of 32% & Revenue CAGR of 20%

3. Strong FY23: PAT up 321% and Revenue up 38% YoY

4. Strong FY24: PAT 94% & Revenue up 47% YoY

5. Strong Q1-25: PAT up 59% & Revenue up 22% YoY

PAT up 73% and Revenue up 27% QoQ

6. Business metrics: Improving return ratios

7. Outlook: PAT growth of 20% & Revenue growth of 15-20%

The management is guiding for a strong FY25 with 15-20% growth in revenue and 20% growth in PAT

I think we believe that we shall be able to grow top line wise also more than 15% to 20% and even on earnings growth, also, we are looking at about 20% comfortably. We think based on certain assumptions and price erosion assumptions. But yes, again, we will know, but I am optimistic that I think we are able to hold this.

8. PAT growth of 59% & Revenue growth of 22% in Q1-25 at a PE of 16

9. So Wait and Watch

If I hold the stock then one may continue holding on to NATCOPHARM.

Coverage of NATCOPHARM was initiated after Q2-24 results. The management delivering higher than the Rs 4,000 cr revenue and Rs 1,200 cr PAT guided for FY24 adds confidence in its ability to deliver 20% PAT growth in FY25 with 15-25% growth in revenue. The Q1-25 performance also supports the FY25 guidance.

FY24 expectations: We are hoping to go past INR1,200 crores PAT, I mean that's our expectation. And our sales as well, I think, will probably be a little less than INR4,000 crores. I think that's our expectation where things are.

Along with the organic outlook with the FY25 guidance of 15-20% growth in revenue and 20% growth in PAT, there is potential for inorganic growth. The full impact of inorganic could be felt in FY26

Do we have a transaction we're going to close? we're looking hard, I think that's all I can share at this time. But hopefully, we'll be able to consummate something in the next 12 months, that's our expectation.

Quarter1 is the biggest quarter for NATCOPHARM folowed by quarter 4. In Q1 it has delivered PAT growth of 59% & Revenue growth of 22% which gives it a cushion to cover up for the traditionally slower quarters of Q2 and Q3.

10. Or, join the ride

If I am looking to enter NATCOPHARM then

NATCOPHARM has delivered PAT growth of 59% & Revenue growth of 22% in Q1-25 at a PE of 16 which makes valuations reasonable in the short-term.

NATCOPHARM is guiding for PAT growth of 20% & Revenue growth of 15-20% in FY25 at a PE of 16 which makes valuations quite reasonable in the medium term.

NATCOPHARM delivered Rs 854.9 cr of free cash flow in FY24 against a market cap of Rs 26,081 cr. As of FY24 end it is available on a free cash flow yield of 3.3% which makes the valuations quite reasonable. In the absence of significant capex in FY25, once expect larger free cash flow generation.

I don't see any large capex, that’s why you see the cash is increasing in the books because we're not spending so much in capex here.

Previous coverage of NATCOPHARM

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer