KPI Green Energy: PAT growth of 100% & revenue growth of 75% in H1-25 at a PE of 48

Guidance of earnings CAGR of 45-50% for the next 2-3 years. H1-25 performance in line with guidance. Strong revenue visibility based on orders in hand at 4X of execution in FY24

1. Renewable power generating company in Gujarat

kpigreenenergy.com | NSE: KPIGREEN

Business Segments

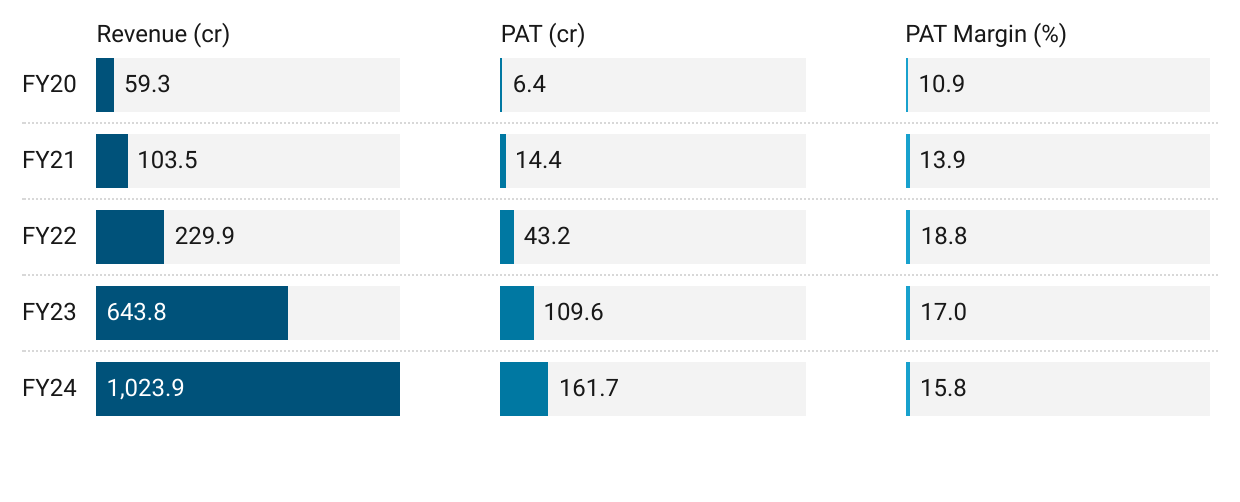

2. FY20-24: Revenue CAGR of 124% & PAT CAGR of 104%

3. Strong FY24: PAT up 48% & Revenue up 59% YoY

4. Strong Q2-25: PAT up 99% & Revenue up 83% YoY

PAT up 6% & Revenue up 3% QoQ

5. Strong H1-25: PAT up 100% & Revenue up 75% YoY

6. Business metrics: Strong return ratios

7. Outlook: Earnings CAGR of 45-50%

i. FY24-26: Earnings CAGR of 45-50%

The management is confident of growing the earnings by 45-50% CAGR over next 2-3 years.

ii. FY25: Strong revenue visibility - Order book at 552 MW

A very strong 62MW capacity energized in H1-25 compared to 133 MW in FY25. The visibility of the order book is 4 times the FY24 run-rate.

8. PAT growth of 100% & revenue growth of 75% in H1-25 at a PE of 48

9. Hold?

If I hold the stock then one may continue holding on to KPIGREEN

The strong business momentum of FY24 continues into an equally strong H1-25. KPIGREEN executed 133 MW in FY24. In H1-25 it has already installed 62MW. With H2 being significantly bigger than H1, one can see early indications of a strong FY25.

Cumulative capacity till FY23: 312+ MW

Installed Capacity till FY24: 445+ MW (IPP 158+ MW | CPP 287+ MW)

Installed Capacity till H1-25: 507+ MW (IPP 171+ MW | CPP 336+ MW)

The growth in H1-25 is in-line with the guidance of 45-50%

Strong order book is providing confidence of a strong FY25 and providing revenue visibility and one can keep riding the business momentum as long as it lasts

10. Buy?

If I am looking to enter KPIGREEN then

KPIGREEN has delivered PAT growth of 100% & Revenue growth of 75% in H1-25 at a PE of 48 which makes valuations fairly priced in the short term.

The outlook for earnings CAGR of 45-50% for the next 2-3 years provides the opportunity in KPIGREEN at PE of 48.

Strong revenue visibility based on orders at hand. Order book at 4X the FY24 execution. The order book creates confidence in the management outlook to deliver the growth in KPIGREEN.

At a PE of 48 margin of safety is not high. One weak quarter and the impact would be clearly seen on the stock price. Strong execution is needed to sustain valuations

Previous coverage of KPIGREEN

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

What’s the revenue proportion of IPP segment ?

For H125 it was 87% from Cpp which is low margin I guesss. Besides earlier high margin was due to land sale. Please comment on this if one intends to invest in this company