Kilburn Engineering: 100%+ EBITDA growth & 70% revenue growth in FY24, followed by 25-30% growth in FY25 at a PE of 26

Anticipate substantial revenue growth in the upcoming years, driven by a strong flow of orders and a pending order book. Growth along with margin expansion providing a strong outlook till FY25.

1. Market leader in the manufacture of solid, liquid and gas drying systems

kilburnengg.com | BOM : 522101

The Company is a market leader in solid, liquid and gas drying systems and provides a comprehensive package of solutions for tea, fertiliser, carbon black, soda ash, pharmaceuticals, dyes and pigments and specialty chemicals among other industries.

2. FY21-23: Recovery in FY23, not a great recent past

Losses in FY21

Break even in FY22

Profitability in FY23

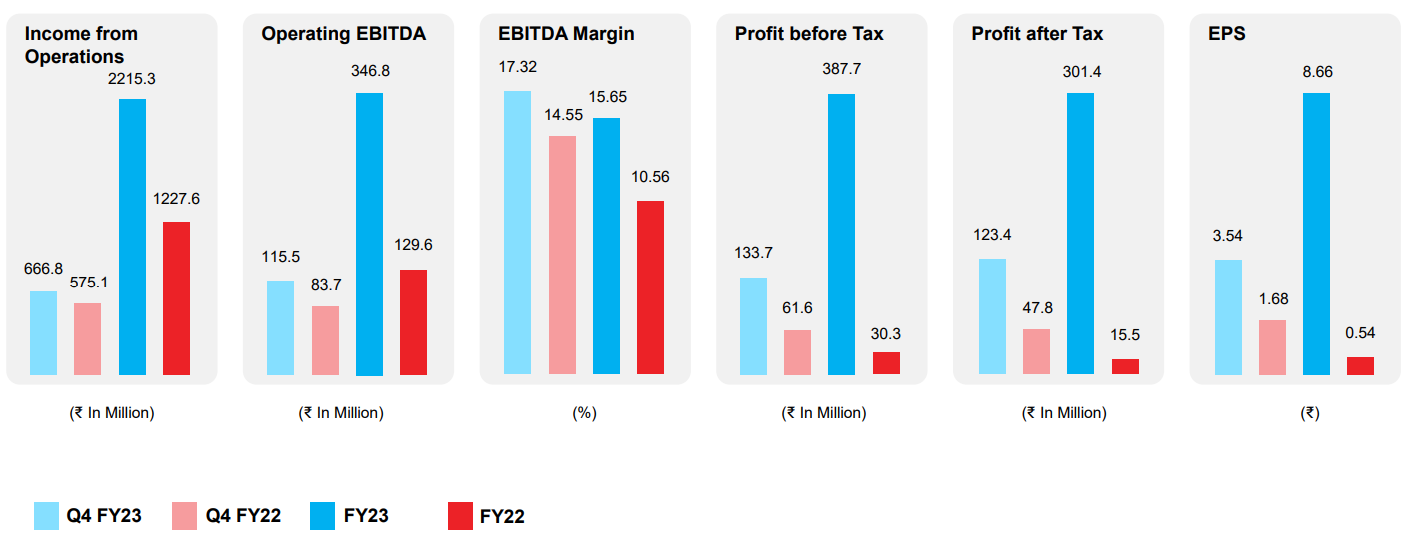

3. Strong FY23: 19x FY22 PAT & Revenue up 80% YoY

Consistent growth in top-line and bottom-line with healthy order inflows

Revenue growth of 80.45% over the previous year

Operating EBITDA margins at 15.65%

Order booking of Rs. 354 cr during the year resulting in a higher Order Backlog of Rs. 246 Crore as on 31.03.2023 , which will be executed during the next fiscal.

Net Debt position of Rs. 49 crs, a reduction of Rs.23 crs

4. Strong Q1-24: PAT up 145% and Revenue up 36% YoY

Consistent growth in topline and EBITDA due to a strong opening order book

Revenue growth of 36.36% over the corresponding previous quarter.

Operating EBITDA margins at 17.59% for the quarter an expansion of 750 bps due to economies of scale and better product mix.

Diversified Order Backlog of Rs. 213 Crore as on 30.06.2023 , which will be executed during the current fiscal.

Rs 32 Crs worth of orders received in the quarter.

Q1-24 Results are strong on a QoQ basis

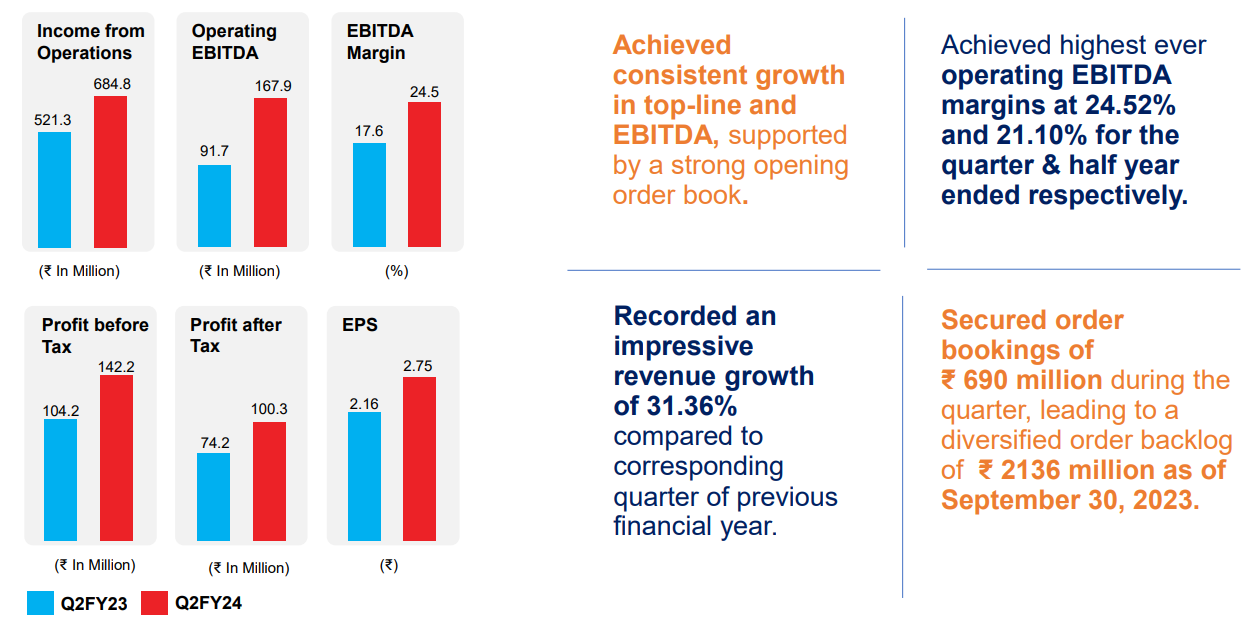

5. Strong Q2-24: PAT up 35% and Revenue up 31% YoY

PAT up 41% and Revenue up 3% QoQ

6. Strong H1-24: PAT up 66% and Revenue up 34% YoY

7. Business metrics: Return ratios improved significantly in FY23

The growth in turnover, EBITDA and PBT should continue resulting in higher free cashflows which should enable the company to become net debt free in the next 12 to 18 months

8. Outlook: 70% revenue CAGR in FY24

i. 70% revenue growth in FY24

Revenue of Rs 236 cr in FY23 to Rs 400 cr in FY24 implies a growth of 70%

For the second half, we expect a very healthy order booking in the range of ₹250 crores to ₹300 crores, which would translate into ₹350 crores to ₹400 crores by the end of the year. The revenue is expected to be in the range of ₹300 plus crores for the current financial year and with the existing orders, we expect to maintain an EBITDA of 20% plus.

About M. E. Energy, we expect the top-line to be in the range of ₹75 crores and their margins would be very much in line with the Kilburn Engineering margins as well.

Including the inorganic numbers we are still guiding for ₹400 CR in FY'24.

ii. 25-30% revenue CAGR in FY25

25-30% growth on expected revenue of Rs 400 cr in FY24 implies a revenue of Rs 500-520 cr in FY25

For the next financial year, we expect our growth to be in the range of 25% to 30%.

iii. FY24 margin expansion: EBITDA growth of 130%

EBITDA margin of 20% on Rs 400 cr implies an EBIDTA of Rs 80 cr in FY24 which is a 130% increase over FY23 EBITDA of Rs 34.68

Well, if you were there in the last investor meeting, we had mentioned that we would be targeting 17% to 18% of margins. But we have now reached 20%. So we expect that we'll maintain that.

iv. Strong Order-book providing revenue visibility

Rs 214 cr order book and the orders expected in Q3 to be executed in FY24 to help it deliver an organic revenue of Rs 300 cr in FY24

We are expecting a number of orders in Q3 and a part of it would definitely be executed in the current year.

9. 100%+ EBITDA growth & 70% revenue growth in FY24 at a PE of 26

10. So Wait and Watch

If I hold the stock then one may continue holding on to Kilburn

Coverage of Kilburn was initiated after Q1-24 results. The investment thesis has not changed after a strong H1-24. The only changes are the delivery of a strong H1-24 and the increased confidence in the management to deliver a stronger FY24

The outlook is strong for both FY24 and FY25 and one can wait and see the execution play out.

The margin expansion to EBITDA of 20% in FY24 is a strong positive and one needs to see if it is maintained in FY25

Kilburn does not have a consistent track record of solid execution. One needs to monitor execution on its guidance quite closely.

11. Or, join the ride

If I am looking to enter the stock then

Kilburn is guiding for 100%+ EBITDA growth & 70% revenue growth in FY24 at a PE of 26 which makes the valuations reasonable.

Outlook of 25-30% growth in FY25 adds to the valuation comfort.

Rs 500-520 cr of FY25 revenue at todays market cap of Rs 954 cr is reasonable. ‘

Previous coverage of Kilburn

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades