Karur Vysya Bank: PAT growth of 24% & Total Income growth of 17% in 9M-25 at a PE of 10

Strong outlook based on loan growth of 14%+, stable NIMs and ROA of 1.6-1.65% in FY25 for KARURVYSYA. 9M-25 in line with FY25 guidance. P/B of 1.61 makes valuations quite reasonable

1. A private sector bank

kvb.co.in | NSE: KARURVYSYA

2. FY20-24: PAT CAGR of 62% & Total Income CAGR of 12%

3. Strong FY24: PAT up 45% & Total Income up 21% YoY

Operating profit growth grew by 14% in FY24. This is an indicator of the PAT growth for FY25 when the impact of lower provisioning would have played out within FY24.

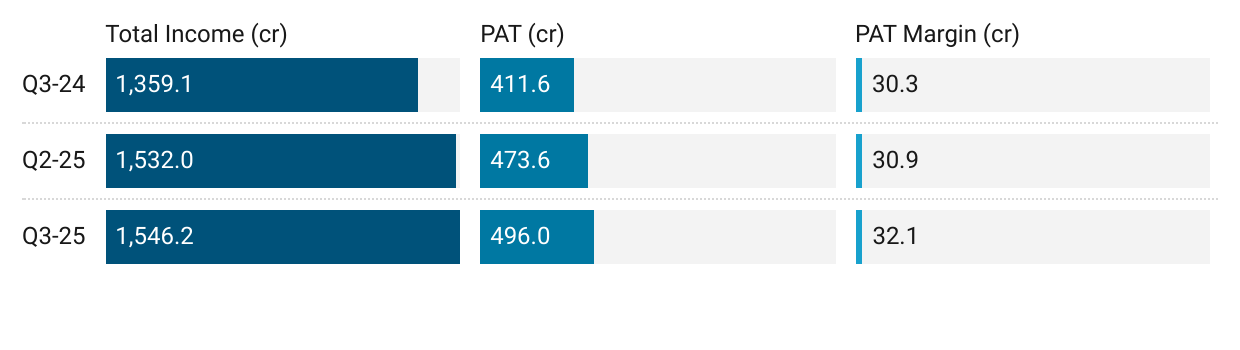

4. Strong Q3-25: PAT up 20% & Total Income up 14% YoY

5. Strong 9M-25: PAT up 24% & Total Income up 17% YoY

6. Business metrics: Strong return ratios

Aims to keep ROA above 1.65%. They achieved 1.74% in the current quarter and are confident about maintaining this level going forward.

7. Outlook: Loan growth to be at 14%+

Growth: 14%+ credit growth & deposit growth.

Net Interest Margin (NIM): NIM of around 3.85% for the next quarter. While they have maintained a NIM above 4% in the current quarter, the management anticipates a slight decrease due to factors such as potential policy rate changes and deposit cost increases. Rates on deposits are not likely to come down.

Cost of deposits is expected to increase by 10 basis points in the next quarter.

Yield on advances may fluctuate depending on policy rate changes, which are expected next month.

Asset Quality: Focused on maintaining a gross NPA of less than 2% and a net NPA of less than 1% of their loan book.

Cost to Income Ratio: Focused on maintaining a cost-to-income ratio of below 50%. The bank's current cost to income ratio is 47.27%.

i. Guidance for Q4-25 (Matches Full Year Guidance):

Credit growth: 14% plus

Deposit growth: 14% plus

NIM: 3.85%

Credit cost: 0.75%

Gross NPA: Less than 2%

Net NPA: Less than 1%

ROA: Above 1.65%

Cost to income: Below 50%

8. PAT growth of 24% & Total Income growth of 12% in 9M-25 at a PE of 10

9. Hold?

If I hold the stock then one may continue holding on to KARURVYSYA

Based on 9M-25 performance, KARURVYSYA looks on track to deliver the on the FY25 guidance.

The bank’s performance indicators align with our guidance, demonstrating consistent and inclusive growth.

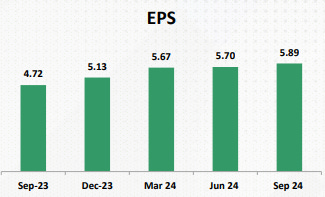

KARURVYSYA is in the middle of a strong run and has delivered sequential QoQ EPS growth since Q1-22 to Q3-25

One can hold KARURVYSYA till Q4-25 end and the see the management guidance for FY26.

The management indicated that it is too early to discuss the outlook for the next financial year (FY26), given the dynamic nature of the market. However, they are focused on leveraging various levers to maintain profitability and growth.

We have maintained strong trajectory of growth in RAM (Retail, Agriculture, and MSME) verticals, continuing the solid start we made at the beginning of the year. I am confident that the same will be maintained going forward.

10. Buy?

If I am looking to enter KARURVYSYA then

KARURVYSYA has delivered PAT growth of 24% and total income growth of 17% in 9M-25 at a PE of 10 which makes the valuations quite reasonable.

At a 9M-25 end net-worth of Rs 11,314 cr on a current market cap of Rs 18,252 cr implies that KARURVYSYA is trading a price to book of 1.6 which makes the valuations reasonable.

FY25 loan growth estimate of around 14% at PE of 10 is nothing exciting but we are looking at a re-rating based on the price to book multiple as the provisions reduce and the quality of the book improves. There will be an opportunity in the stock till a price to book of closer to 2 based on outlook for FY25.

Previous coverage of KARURVYSYA

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer