Karur Vysya Bank: PAT growth of 26% & Total Income growth of 19% in H1-25 at a PE of 10

Strong outlook based on loan growth of 14%+, stable NIMs and ROA of 1.6-1.65% in FY25 for KARURVYSYA. H1-25 in line with guidance. P/B of 1.61 makes valuations quite reasonable

1. A private sector bank

kvb.co.in | NSE: KARURVYSYA

2. FY20-24: PAT CAGR of 62% & Total Income CAGR of 12%

3. Strong FY24: PAT up 45% & Total Income up 21% YoY

Operating profit growth grew by 14% in FY24. This is an indicator of the PAT growth for FY25 when the impact of lower provisioning would have played out within FY24.

4. Strong Q2-25: PAT up 25% & Total Income up 22% YoY

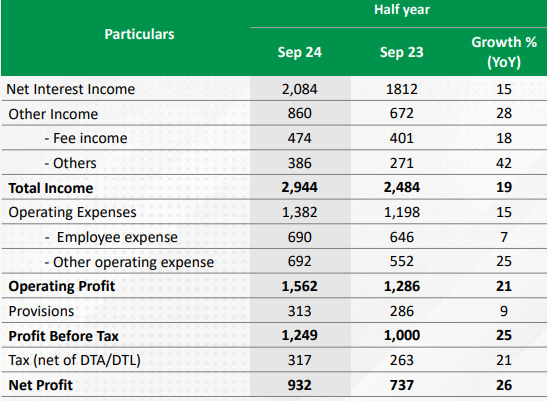

5. Strong H1-25: PAT up 26% & Total Income up 19% YoY

6. Business metrics: Strong return ratios

7. Outlook: Loan growth to be at 14%+

i. FY25: Loan growth at 14%+

Loan Growth: Overall loan growth to be at 14% plus

Net Interest Margins (NIMs): With respect to the margins, we expect that to be at and around 4% levels till first half of the current year

Gross NPA: down to 1.4%, and we expect that we will continue to maintain at below 2% levels.

Net NPA: down to 0.4%, and we would continue to maintain net NPA at less than 1% of our loan book.

ROA: We have achieved ROA of 1.63% in financial year '24. Our effort would be to ensure that our ROA is above 1.6% or 1.65% levels at all times

8. PAT growth of 26% & Total Income growth of 19% in H1-25 at a PE of 10

9. Hold?

If I hold the stock then one may continue holding on to KARURVYSYA

Coverage of KARURVYSYA was initiated after Q3-24 results. The investment thesis has not changed after a strong FY24 and strong H1-25 . The delivery of a Q1-25 in-line with the FY25 guidance has increased confidence in the management

Based on H1-25 performance, KARURVYSYA looks on track to deliver the on the FY25 guidance.

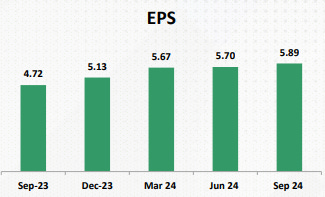

KARURVYSYA is in the middle of a strong run and has delivered sequential QoQ EPS growth since Q1-22

10. Buy?

If I am looking to enter KARURVYSYA then

KARURVYSYA has delivered PAT growth of 26% and total income growth of 19% in H1-25 at a PE of 10 which makes the valuations quite reasonable.

At a H1-25 end net-worth of Rs 10,818.18 cr on a current market cap of Rs 17,440 cr implies that KARURVYSYA is trading a price to book of 1.61 which makes the valuations reasonable.

FY25 loan growth estimate of around 14% at PE of 10 is nothing exciting but we are looking at a re-rating based on the price to book multiple as the provisions reduce and the quality of the book improves. There will be an opportunity in the stock till a price to book of closer to 2 based on outlook for FY25.

One needs to keep a watch on asset quality of KARURVYSYA even though NPA’s are trending down with 96%+ of GNPA covered by provisioning

Previous coverage of KARURVYSYA

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer