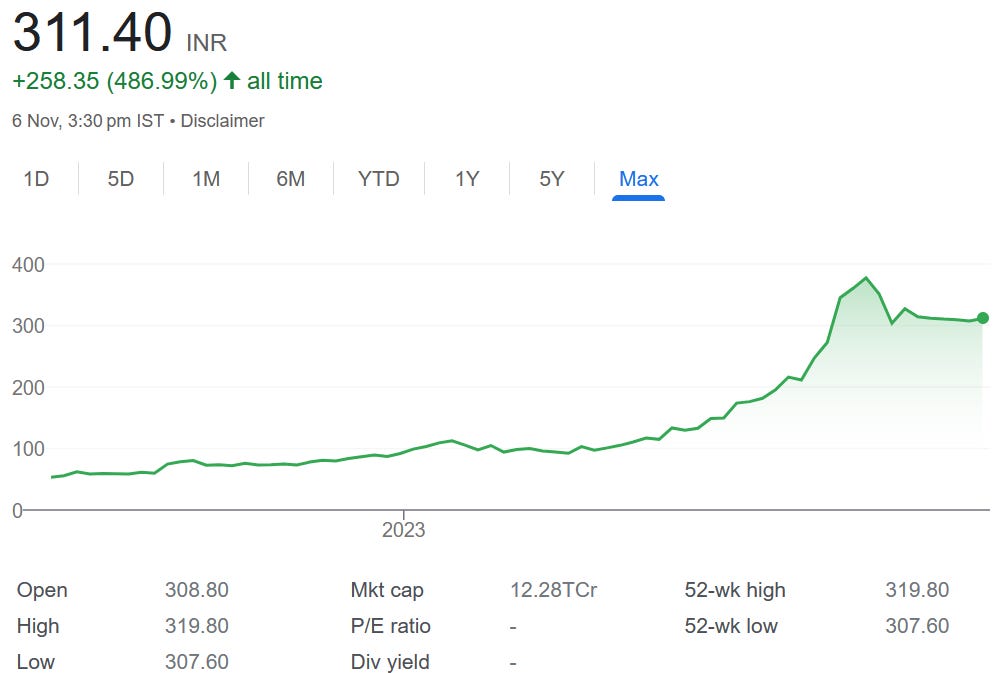

Jupiter Wagons: PAT up 280% & Revenue up 129% in H1-24 with similar trajectory for H2-24 at a PE of 54

The outlook for JWL remains robust with a solid order book and all business lines set for further scaling up given the high visibility of ordering till FY26

1. One of the largest player in India’s Railway sector

jupiterwagons.com | NSE: JWL

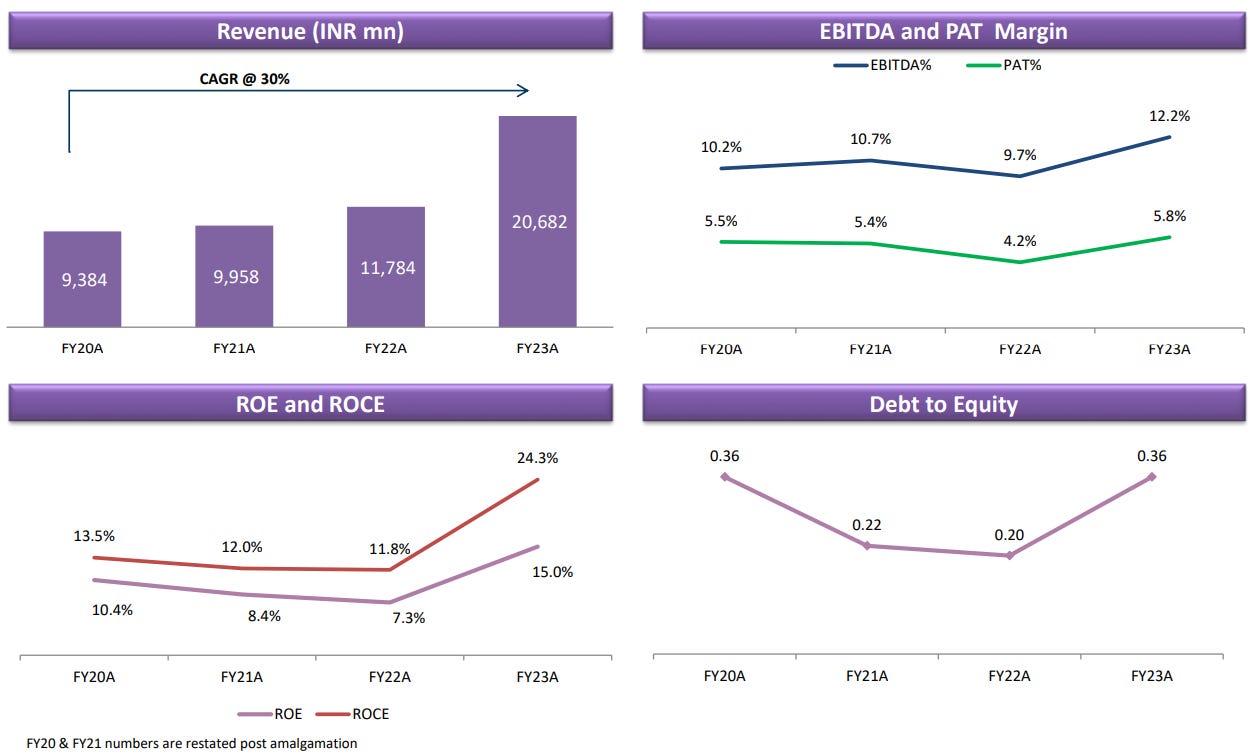

2. Solid growth since FY21: 50%+ CAGR growth in PAT

4. Strong Q1-24: PAT up 374% & Revenue up 155%

Due to an improved product mix and the introduction of value-added products, we reported an EBITDA margin of 13.2%, representing an expansion of 260 bps YoY.

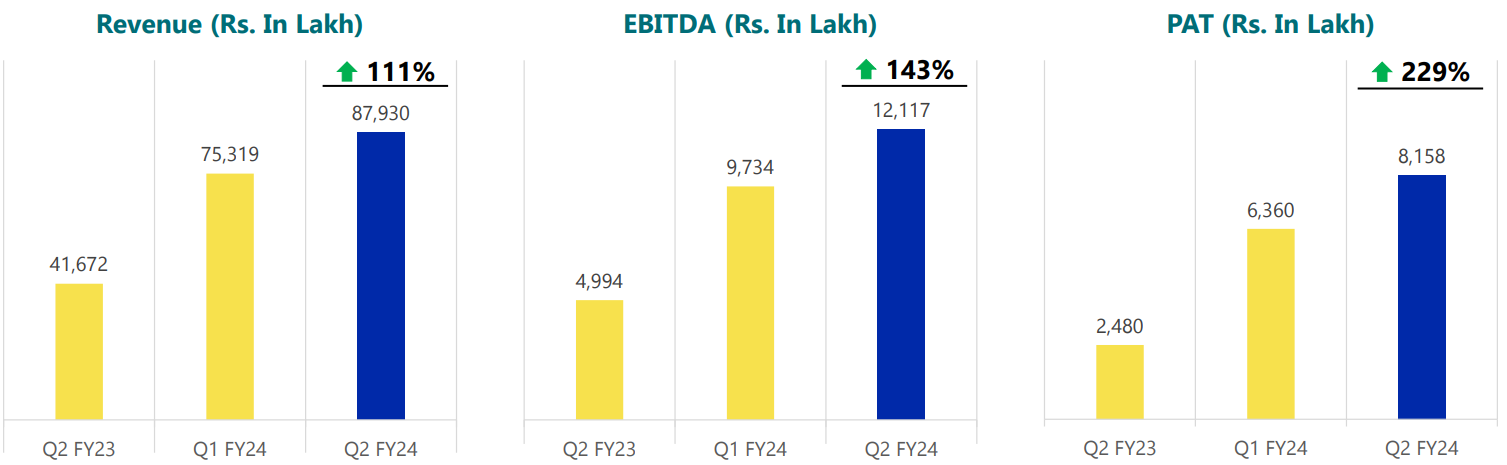

4. Strong Q2-24: PAT up 229% & Revenue up 111%

Revenue from operations for Q2FY24 stood at ₹ 87,930 lakh, up 111% (YoY)

EBITDA for Q2FY24 at ₹ 12,117 lakh higher by 143% (YoY)

Continue to deliver industry leading margin as EBITDA Margin improves to 13.8% in Q2 FY24 from 12.0% in Q2 FY23

PAT for Q2 FY24 stood at ₹ 8,158 lakh, higher by 229% (YoY) with PAT Margin improving to 9.3%

5. Strong H1-24: PAT up 280% & Revenue up 129%

Revenue from operations for H1FY24 stood at ₹ 1,63,248 lakh, up 129.2% (YoY)

EBITDA for H1FY24 at ₹ 21,851 lakh, up 172% (YoY)

Continue to deliver industry leading margin as EBITDA Margin improved to 13.4% in H1 FY24 from 11.3% in H1 FY23

PAT for H1FY24 stood at ₹ 14,518 lakh, higher by 280% (YoY), PAT Margin improves to 8.9%

6. Return Ratios: JWL an efficiently run company

Net of cash is that we are a net zero debt company.

7. Outlook: Revenue growth of 100%+ in FY24

i. Revenue visibility for FY24 & FY25: Order book 3X of FY23 revenue and growing

Our present order book of Rs.5,952 Crores includes Rs.5,355 Crores of order from wagons, and we are confident that this is set to enhance further.

ii. Expecting top-line growth of about 100%+ in FY24

A 119% top-line growth in H1-24 provides confidence for 100% growth in FY24. To deliver 100% growth in FY24, the asking rate of growth for H1-24 is 84% YoY which looks achievable given the H1-24 performance and the fact that H2-23 was around 2/3 of FY23.

iii. Capacity in place to support execution of order book

Growth driven by wagons, Q1-24 capacity of around 570 wagons per month (1713/3) to be increased to 1000 by FY25 start

We exited Q2 with a production run rate of nearly 700 wagons per month and as we increase the capacity of our foundry, we will see a further scale up in wagon production to around 800 units per month by the end of this financial year.

And by next year, we are looking to manufacture about 1,000 wagons per month.

iv. No concerns in terms of order visibility for FY26

8. Outlook for 100% growth in FY24 at a PE of 54

9. So Wait and Watch

If I hold the stock then one may continue holding on to JWL.

Coverage of JWL was initiated after Q1-24 results. The investment thesis has not changed after a strong H1-24. The only changes are the delivery of a strong H1-24 and the increased confidence of management to deliver a stronger FY24

The business is on a growth trajectory and the management expects the momentum to carry on till FY26.

I do not think there is any challenges in terms of order books, so it is more on the execution going forward that we are more focused and obviously on the backward integration part of it so that we can solidify the business as well as better our margins.

One needs to wait and watch the growth unfold till FY26.

FY23 revenue was Rs 2,000 cr and FY24 revenue expected to be around Rs 4,000 cr. But order book is around Rs 6,000 cr. So order book is 1.5X FY24(e) revenue. One needs to see significant order inflow from H2-24 for us to have revenue visibility into FY26 & FY27.

10. Join the ride

If I am looking to enter the stock then

JWL is delivering 100%+ growth in the top-line and bottom-line. JWL at a PE of 54 for 100%+ top-line growth in FY24 makes valuations reasonable as long as the growth momentum sustains till FY26 and beyond.

The medium term story i.e. execution of current order book of Rs 5,952 cr plays out in18 months by FY25 which is not far away

EPS for FY23 was Rs 3.12. Assuming the 100%+ growth and rounding up the EPS to Rs 8, the stock is available for a forward FY24 PE of 39 which would be reasonable if there is visibility for both FY26 and FY27.

On the flip side the margin for error is small. One bad quarter in the 6 remaining quarters and the asking rate will become quite high. At a PE of 54, the stock can become quite expensive quite quickly

Positions need to be built over time over bad days when the stock is not doing well.

Previous coverage of JWL

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Disclaimer

It is an analysis of the company data and not a stock recommendation

My analysis can be completely wrong and can change the next minute based on changes in my understanding of the company

I look to own good companies at prices where there is a path to market beating returns over decades