Jupiter Wagons: PAT growth of 46% & Revenue growth of 17% in Q1-25 at 64 PE

EBITDA growth of 68% expected in FY25. Revenue growth of 50% expected in FY25. Order book at 1.3X FY25 expected revenue . JWL looking 3X from Rs 3600+ cr in FY24 to Rs 10,000 cr by FY27/ FY28

1. Why is JWL interesting

jupiterwagons.com | NSE: JWL

JWL benefits from tailwinds of railway infrastructure creation. It is expecting the demand flow to be strong driving exciting top-line growth with significant margin expansion. Opportunity will emerge over the longer term as JWL is looking to triple in size over the next 3-4 years to reach Rs 10,000 cr revenue 2. One of the largest player in India’s Railway sector

FY24: Around 76% or 77% is from the wagon and balance is from the other CV business and containers.

FY28: We expect at least more than 50% of our revenues to come from our non-Wagon business. So, the non-Wagon business is going to produce significantly towards our revenues.

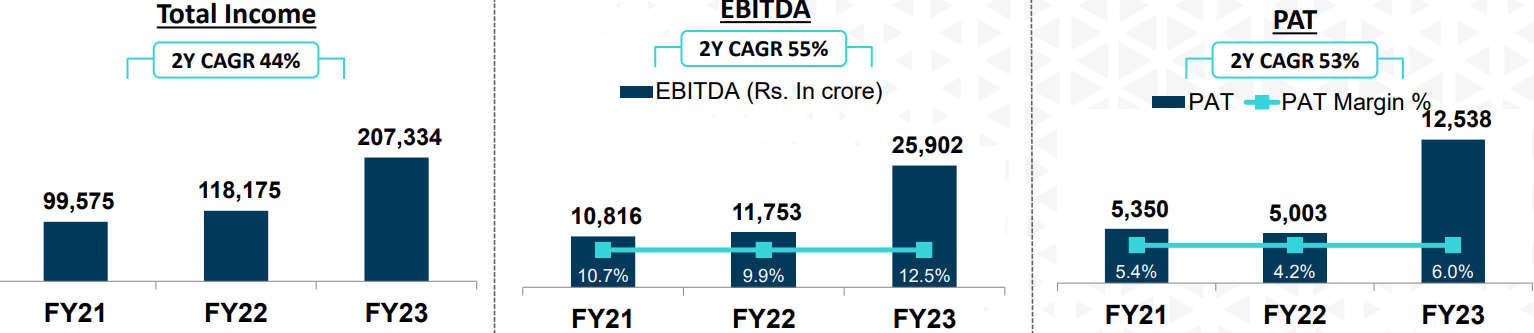

3. FY21-24: PAT CAGR of 84% & Revenue CAGR of 54%

4. Strong FY23: PAT up 151% & Revenue up 76%

5. Strong FY24: PAT up 165% & Revenue up 77%

6. Strong Q1-25: PAT up 46% & Revenue up 17% YoY

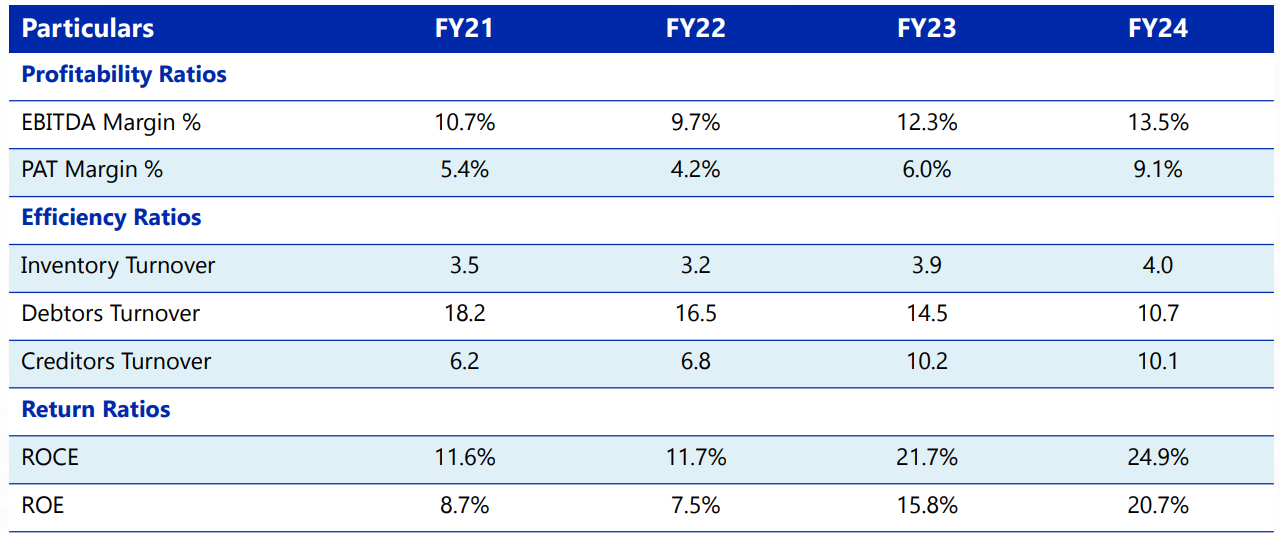

6. Business Metrics: Strong & improving return ratios

7. Outlook: Revenue growth of 50% & EBITDA growth of 68%

i. FY25: Revenue growth of 50%

Revenue expectation of Rs 5,500-5,600 cr in FY25 implies a 50% growth in FY25

ii. FY25: EBITDA growth of 68%

EBITDA margin of 13.5% in FY24 expected to expand to 15% in FY25. On Rs 5,500 cr of FY25 expected revenue it implies 68% EBITDA growth over the FY24 EBITDA of Rs 493 cr

We are confident that these margins are sustainable. It will be around the 15% kind of margins because as I mentioned that as the other businesses start contributing significantly, so they will start having a positive impact on the margins. Going forward as we achieve better backward integration, as the wheel business becomes bigger, as the braking business becomes bigger, they start contributing. We expect the margin profiles to improve.

iii. FY25: Strong revenue visibility. Order book 1.3X FY25 revenue

On Rs 5,500 cr expected revenue in FY25 implies order book in place to support 1.3X FY25 expected revenue.

Order book as of 30th June 2024 stands at ₹ 7,02,834 lakh.

From the private sector, we are continuously adding incremental order books.

We expect Indian Railways also to come out with significant tenders in the coming months.

Order inflow will continue to remain strong.

We are more focused on increasing our capacity, especially our foundry capacity and on the backward integration side in terms of the braking business as well as the wheelset business.

iv. Rs 10,000 cr revenue by FY27 or FY28 - Revenue CAGR of 29-40%

8. PAT growth of 46% & Revenue growth of 17% in Q1-25 at a PE of 64

9. Do I stay?

If I hold the stock then one may continue holding on to JWL.

The JWL management indicating that 15% margin is sustainable, will drive significant bottom-line growth in FY25

Despite challenges from the general election and peak summer, we maintained a strong consolidated EBITDA margin of 15.5%.

We expect the demand flow to be strong and our margins to improve further

JWL management is quite confident about its prospects in FY25 with expectations of 50%+ top-line growth

We anticipate a significant increase in execution and performance throughout fiscal year 2025 and remain confident in the growth trajectory of these businesses.

JWL management indicating that the journey to Rs 10,000 cr of revenue will be completed in the next 3-4 years is a reason to continue with the stock.

We continue to benefit from tailwinds of infrastructure creation across the country. The outlook for business remains robust with a solid order book and all our business lines set for further scaling up given the high visibility of ordering. We are very excited about our prospects.

10. Do I enter?

If I am looking to enter JWL then

JWL has delivered PAT growth of 46% & Revenue growth of 17% in Q1-25 at a PE of 64 which makes valuations fully priced in the short term.

JWL is guiding for 50% revenue growth & EBITDA growth of 68% on the back of a strong order book in FY25 at at a PE of 64 which makes valuations fairly priced from a FY25 perspective

Over the longer term JWL is guiding for revenue CAGR of 29-40% till FY27/FY28 at PE of 64 valuations reasonably priced in the longer term. The opportunity in JWL will emerge from the execution in FY26 & beyond.

There is opportunity in JWL if execution goes as per plan. On the flip side the margin for error is small. One bad quarter and the asking rate to sustain a PE of 64 will become quite high. At a PE of 64, the stock can become expensive quite quickly if execution falters by a little.

Positions need to be built over time over bad days or periods when the stock is not doing well.

Previous coverage of JWL

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer