Interglobe Aviation: 27% revenue growth in FY24 and back to profits at PE of 17

Free cash flow yield of 11.3% makes INDIGO attractive. Capacity growth at early double digits with inflationary pressures, similar revenue environment in Q1-25 as compared to Q1-24

1. Amongst the fastest-growing low-cost carriers in the world

goindigo.in | NSE: INDIGO

2. FY20-24: Profit in FY24 after 4 years of losses

3. FY23: Strong recovery since Q3-23, operational & financial

A year of recovery and growth as the demand remained robust, and we continued to serve the lion-share of this demand. Our revenues for the financial year 2023 more than doubled as compared to last year and we also reported the highest ever annual revenues of 558.8 billion rupees.

4. 9M-24: Back to profits and revenue up 27% YoY

5. Q4-24: PAT up 106% and revenue up 26% YoY

PAT down 37% and revenue down 8% QoQ

6. FY24: Back to profits and revenue up 27% YoY

7. Business metrics: Generating free cash flow while making losses

Liquidity has further improved as we ended the March quarter with free cash of 208.2 billion rupees. This translates to an increase of 16.2 billion rupees as compared to the December quarter end.

Free cash flow (FCF) is the money a company has left over after paying its operating expenses (OpEx) and capital expenditures (CapEx). The more free cash flow a company has, the more it can allocate to dividends, paying down debt, and growth opportunities.

8. Outlook: Capacity expansion of 10-12%

i. FY24: Capacity expansion of 10-12%

We will broadly grow our capacity at early double digits in the financial year 2025 as compared to financial year 2024.

For the first quarter of financial year 2025, we are expecting to add around 10 to 12% capacity as compared to same period last year which translates to around 3 to 5% capacity growth on a sequential basis.

With this growth projection for the first quarter of financial year 2025, we are likely to be back to the quarterly capacity which we had prior to the accelerated inspection of engines due to the powder metal issue.

We are currently experiencing similar revenue environment in Q1FY25 as compared to Q1FY24.

ii. Margin pressure expected in FY25

There are inflationary pressures in certain cost line items that we are foreseeing in next financial year.

iii. Strong tailwinds

For many years to come, we will receive a minimum of one new plane every week. And this speaks a lot about India, probably, being the last frontier of aviation growth of such a high magnitude and the part IndiGo is poised to play in it.

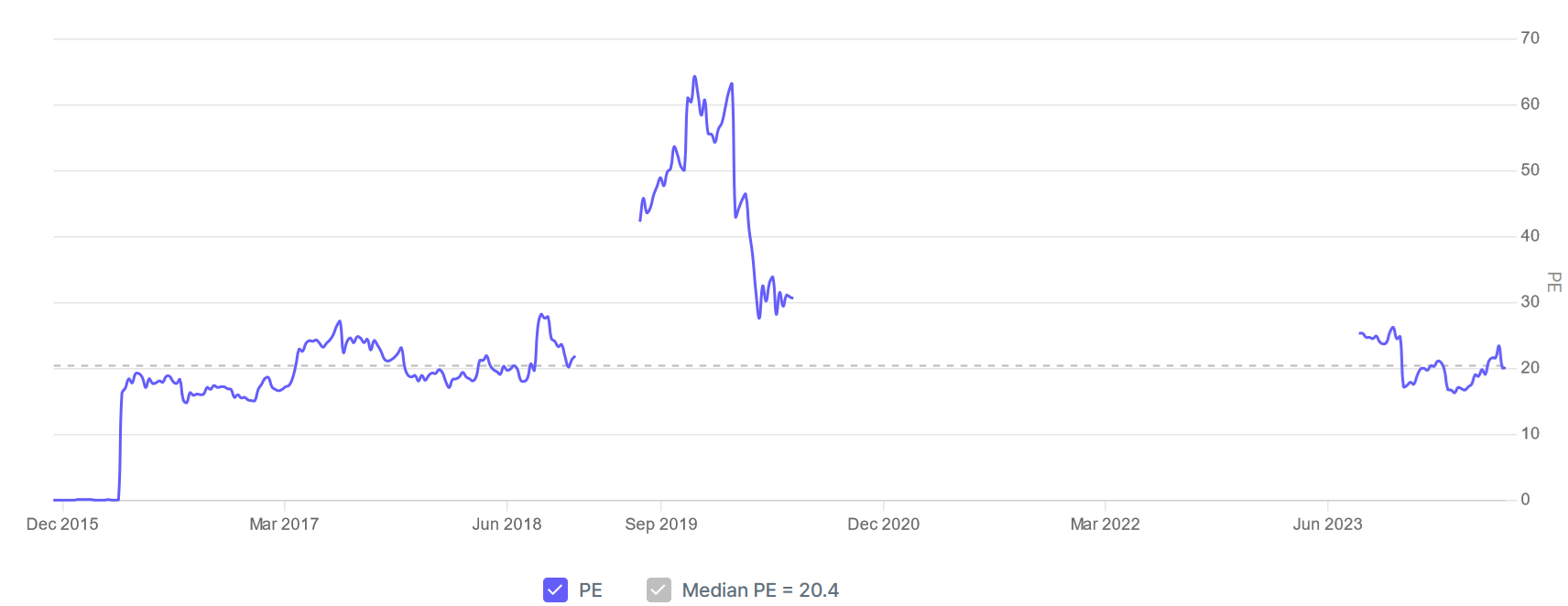

9. Revenue up 27% in FY24 and back into profits at a PE of 20

10. So Wait and Watch

If I hold the stock then one may continue holding on to INDIGO

Coverage of INDIGO was initiated after Q1-24 results. The investment thesis based on industry tailwinds has not changed after a strong FY24. There is confidence in the management to deliver a strong FY25 based on guidance of early double digits increase in capacity.

Outlook for 10-12% capacity growth with inflationary pressures in certain cost line item and similar revenue environment in Q1FY25 as compared to Q1FY24 indicates for some margin pressure in FY25, slowing down bottom-line growth.

The opportunity from getting back into profitability after 4 years of losses has played out. One needs to watch out for the growth momentum sustaining on a quarter to quarter basis.

11. Or, join the ride

If I am looking to enter INDIGO then

27% revenue growth and back into profits in FY24 at a PE of 20 makes valuations fairly priced for the short term.

For FY24, INDIGO generated Rs 19,196 cr of free cash flow and is available for a market cap of Rs 164,041 cr. Its free cash flow yield of 11.1% makes the valuations look very attractive.

Of the Rs 164,041 cr market cap of INDIGO, Rs 20,823 cr is in free cash. This implies that 13% of the market cap is in cash which provides a margin of safety given a history of losses.

Strong liquidity position ring-fences against external shocks

INDIGO is trading close to its long term median PE of 20. Hence opportunities on account of re-rating of multiples will be limited.

Previous coverage of INDIGO

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer