Hind Rectifiers Q3 FY26 Results: PAT Up 27%, Ahead FY26 Guidance

Guidance of 30%+ revenue CAGR for FY25-29 by Hind Rectifiers. Even after a strong a 9M FY26 the valuations are at a premium and price in the growth till FY27

1. Power Electronics Equipment Manufacturing

hirect.com | NSE: HIRECT

Our core customer is Indian Railways, contributing 90% of our revenues

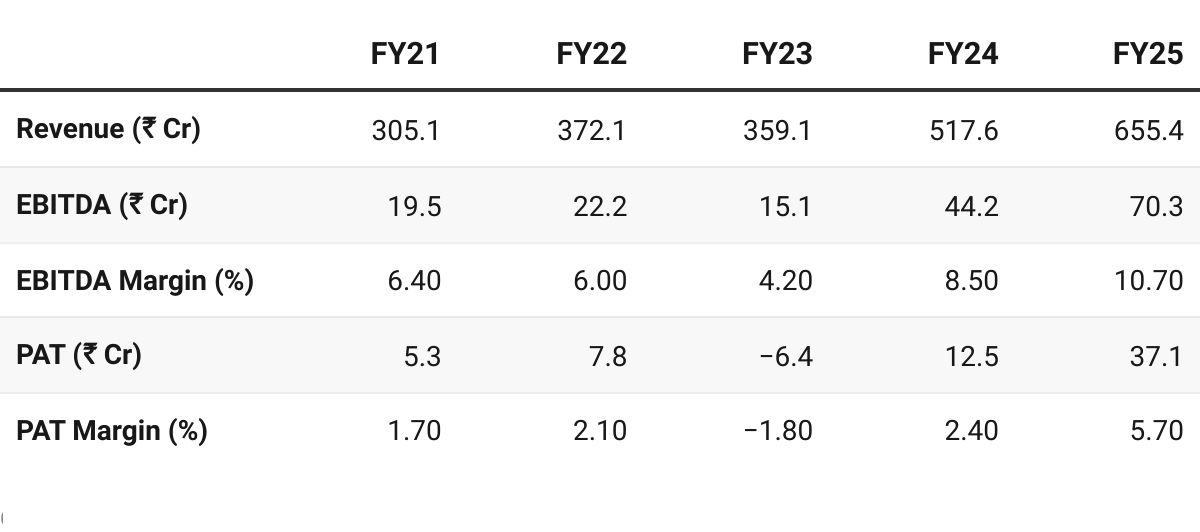

2. FY21–25: PAT CAGR of 63% & Revenue CAGR of 21%

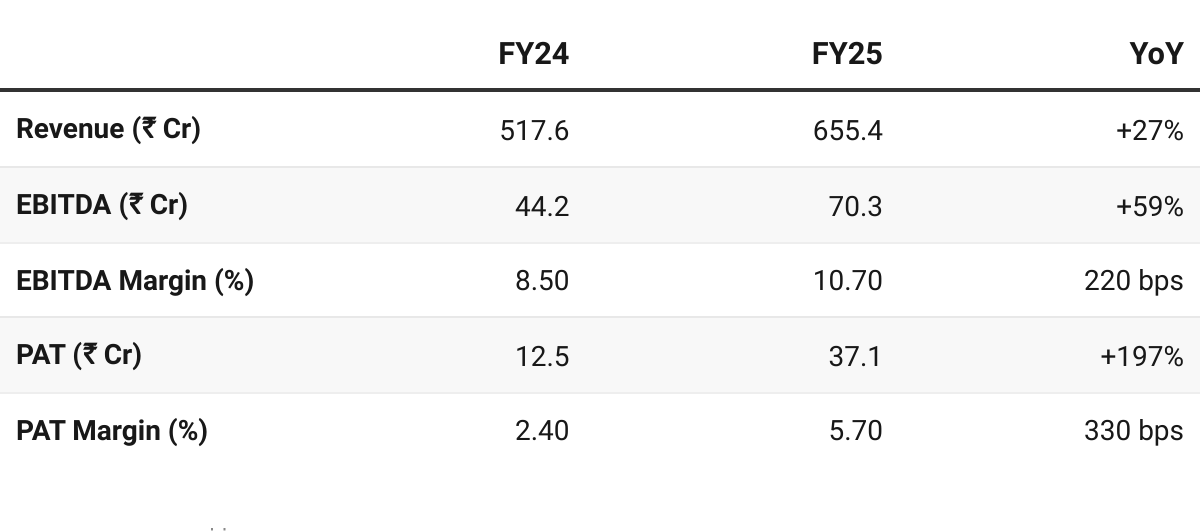

3. FY25: PAT up 197% & Revenue up 27%

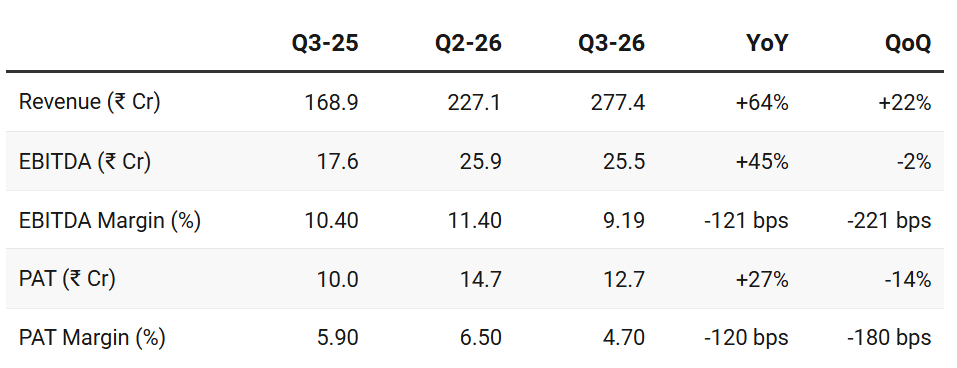

4. Q3-26: PAT up 27% & Revenue up 64% YoY

PAT down 14% & Revenue up 22% QoQ

EBITDA margin moderated by 120 bps year-on-year, primarily due to expansion-led investment in the copper conductors plant at Sinnar and increase in input cost of key raw materials arising from supply chain disruptions.

Strong top-line growth of 64% YoY indicating

Strong execution of the order book

Continued demand from railway electrification projects

Increased traction equipment supply

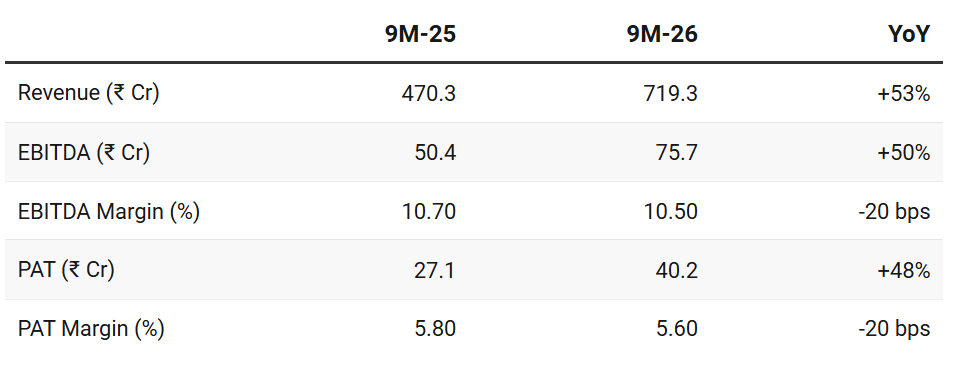

5. 9M-26: PAT up 48% & Revenue up 53% YoY

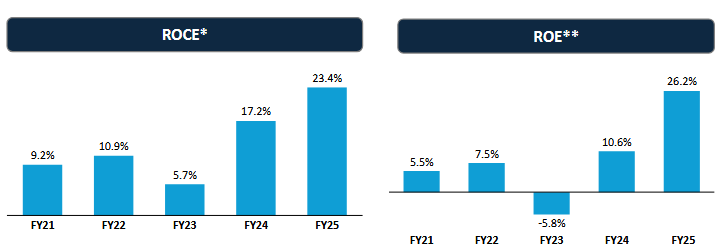

6. Return Metrics: Improving & Strong Return Ratios

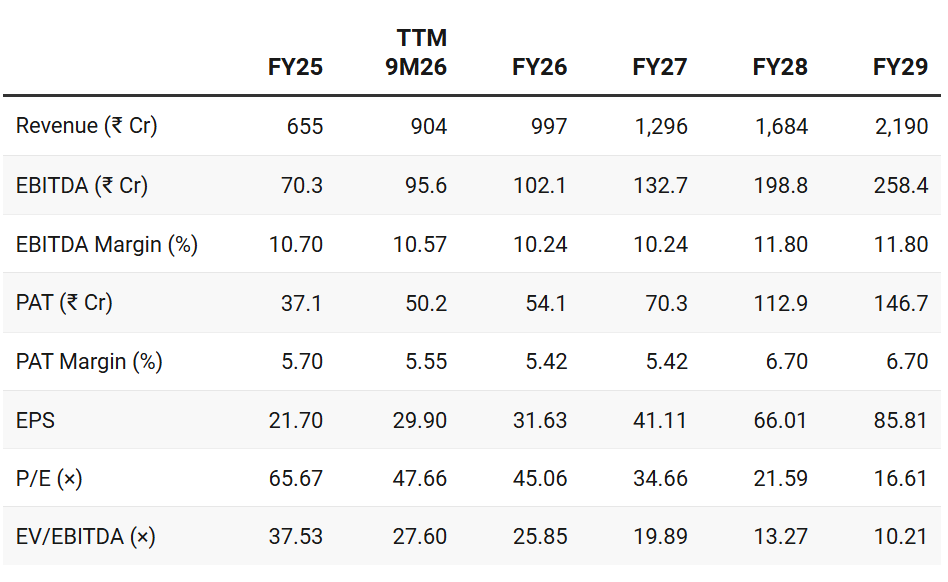

7. Outlook: 30% Revenue CAGR for FY25-29

7.1 Management Guidance

Revenue Growth

FY26 and FY27 growth: And we expect a growth of 30% year-on-year, and we continue to maintain that going into the next year as well.

We will be crossing that 30% on the year to year basis at least for next three years

30% growth is from existing business, existing product lines, products that have already been released into the market, and we expect to get a larger share. It's from existing business.

Anything that is in R&D today, which adds value next year will be on top of that.

7.2 9M FY26 Performance vs FY26 Guidance

Revenue: We don't provide any guidance, but Q4 is looking upwards. It's going very well, going as per the plan that we had set out originally.

Margin Guidance: In fact, it will be better for Q4. And be even better than Q4, which will be in Q1. But the real upside will come from Q2 onwards and the CTC factory will be in full swing

HIRECT H1 FY26 Performance Ahead of FY26 Guidance

Revenue: 9M revenue ahead of the 30% revenue growth guidance.

Margins: Weak performance on margins — Improvement from Q4 onwards. Stronger margins once in-house copper conductor facility reaches full scale in Q2-27

Order-Book: HIRECT indicated that railway tenders expected in Q3 were delayed by a quarter, but order inflows are expected to pick up in the coming quarters.

Expecting order book growth of 30%

During this quarter, the railway tenders, which were expected to be closed had kind of moved out by a quarter, but the requirements are building up, especially for the transformers that is mainstay of our product line. We are expecting the orders to come in next quarter. So from an order buildup point of view, the trajectory is going to be positive and upward.

We mentioned earlier, we are looking at a 30% growth year-on-year, and we expect a similar kind of growth on the order board

7. Valuation Analysis — Hind Rectifiers

7.1 Valuation Snapshot

Current Market Price: ₹1,425; Market Cap: ₹2,461 Cr

Valuations reflects its high growth and improving margins

Even after the recent correction — multiples already discounts the guidance till FY27.

Suggests limited room for further multiple expansion in the near term

The opportunity emerges over the longer term beyond FY27

7.2 Opportunity at Current Valuation

30% Guidance is in the price

The 30% growth guidance is discounted in the price

Opportunity exists as the R&D pipeline gets commercialized and takes growth above 30%

Propulsion System — A New Revenue Engine

Entered the locomotive propulsion system segment, which is significantly higher value than its traditional component business.

Current status:

Propulsion system installed on locomotives

Trials underway on Western Railway

Expected completion: 3–4 months

Initial order book — ~40 propulsion systems already ordered (~₹50 Cr)

Once the trials are successfully completed, the company could participate in larger propulsion tenders from Indian Railways.

Margin Expansion — Backward Integration in Copper Conductors

Commissioned a copper conductor manufacturing facility at Sinnar.

Benefits:

Lower raw material dependence

Improved supply chain reliability

Higher gross margins

Potential external sales to transformer manufacturers

Full margin benefits from Q2 FY27 onward.

Global Expansion Strategy — Acquisition of BeLink Solutions, Europe

While BeLink is currently loss-making,

HIRECT believes a turnaround could lead to significant profitability over time.

7.3 Risk at Current Valuation

High Execution Bar: Delivering 30%+ revenue CAGR for FY25-29 will need strong execution even though supportive demand tailwinds are in place

Valuations are demanding: Valuations for FY26 and FY27 don’t allow for any margin of safety. Impact of even a single weak quarter will be seen in the stock price

Supply Chain Risks: 9M FY26 has already seen lowered gross margins on account of supply chain issues — margins remain sensitive to copper price fluctuations.

Until the in-house copper conductor facility reaches full scale, this risk remains.

Concentration Risk: Railways accounting for ~90% of revenue of HIRECT

Although railway capex remains strong, order timing can be uneven.

Propulsion System Execution Risk — include trial & approval delays and competition from existing propulsion suppliers

The growth opportunity depends on successful certification and tender wins.

BeLink Integration Risk — BeLink is currently loss-making.

If the turnaround takes longer than expected, it could impact consolidated profitability.

Previous Coverage of HIRECT

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer