Gravita India: PAT up 29% & Revenue up 29% in Q1-25 at a PE of 69

Guidance of PAT CAGR of 35% & volume CAGR of 25% for FY24-28. Outlook of tripling PAT to Rs 750-800 cr by FY28 supported by regulatory tailwinds. Capex in place to support the growth outlook.

1. Why is GRAVITA interesting

gravitaindia.com | NSE: GRAVITA

GRAVITA coming out of an ordinary FY24 has started with a strong Q1-25. GRAVITA is expected to triple its PAT by FY28 as a part of its Vision 2028. The Vision 2028 is supported by regulatory tailwinds supporting the recycling industry. While GRAVITA is at premium valuations in the short term, the opportunity exists over the longer term. 2. Recycling of Lead, Aluminium, Plastic and Rubber

Gravita India Limited is a prominent player in the global recycling industry, specializing in the recycling of Lead, Aluminium, Plastic and Rubber

3. FY20-24: PAT CAGR of 64% & Revenue CAGR of 24%

4. Weak FY24: PAT up 19% & Revenue up 13%

5. Q1-25: PAT up 29% & Revenue up 29% YoY

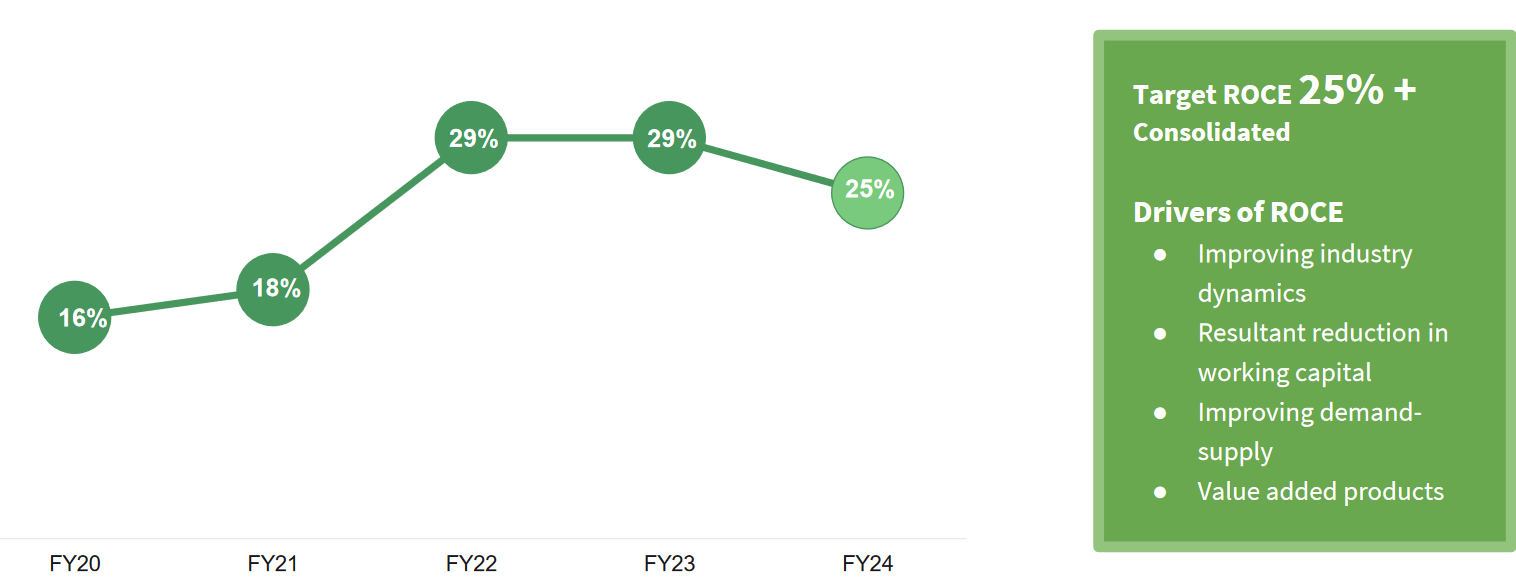

6. Return Ratios

7. Strong outlook: 35% PAT CAGR for FY24-28

GRAVITA guiding for tripling of PAT to Rs 750-800 cr in FY28 from Rs 242 cr in FY24

The company aims for a volume and profitability growth of over 25% and 35%, respectively on CAGR basis, ROCE of over 25%, and an increase in value-added products and non-lead business to over 50% and 30%, respectively.

When we mentioned this 25% CAGR, it’s a long-term guidance and it’s not a short-term guidance. So, there would be years when we would grow faster than 25%, and then there would be years when the growth would not be in line with 25%.

FY28 PAT: It would be around INR750 crores to INR800 crores -- if we achieve our targets.

8. PAT growth of 29% & Revenue growth of 29% in Q1-25 at a PE of 69

9. Do I stay?

If I hold the stock then one may continue holding on to GRAVITA

Following a weak FY24, Q1-25 performance has been strong and GRAVITA looks to be on track to deliver as per the FY28 Vision

FY24: Was also affected by some logistic issues in quarter 3, which has impacted the growth rate to some extent.

FY25: And we are very confident that going forward, our Vision of 2028 of long-term CAGR growth of 25% and PAT growth of 35% is achievable.

Capex is in place to support the FY28 Vision

Regulatory tailwinds to support growth over the longer term. The changes made in the 54th Meeting of the GST Council 9th September, 2024 are a strong long term positive for GRAVITA.

Business momentum is strong and expected to continue into the rest of the year

FY25 Top-line growth: It’s between 20% to 30% throughout the year, unless something strange happens again. I mean like if everything remains normal, you can expect a 20% to 30% growth rate

10. Do I enter?

If I am looking to enter GRAVITA then

GRAVITA has delivered PAT growth of 29% and revenue growth of 29% in Q1-25 at a PE of 69 which makes the valuations quite rich in the short term.

With an FY24-28 outlook of PAT tripling to Rs 750-800 cr at a CAGR of 35% a PE of 69 can be sustained as the opportunity will emerge in GRAVITA from a medium to a longer term perspective

While GRAVITA has a strong record of delivering growth, the stock may have run ahead of the business in the short term. Margin of safety in GRAVITA is limited. Entry in GRAVITA can be made over a period of time when the stock may give some opportunities with a correction.

Previous coverage of GRAVITA

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer