GE Shipping FY26 Results: PAT up 26%, Trades at a Discount to NAV

Offers solid value — 1.3× P/B, 5.8% FCF yield, 25%+ of market cap in cash—providing re-rating potential given a strong FY26. Cyclicality in shipping business is the key risk

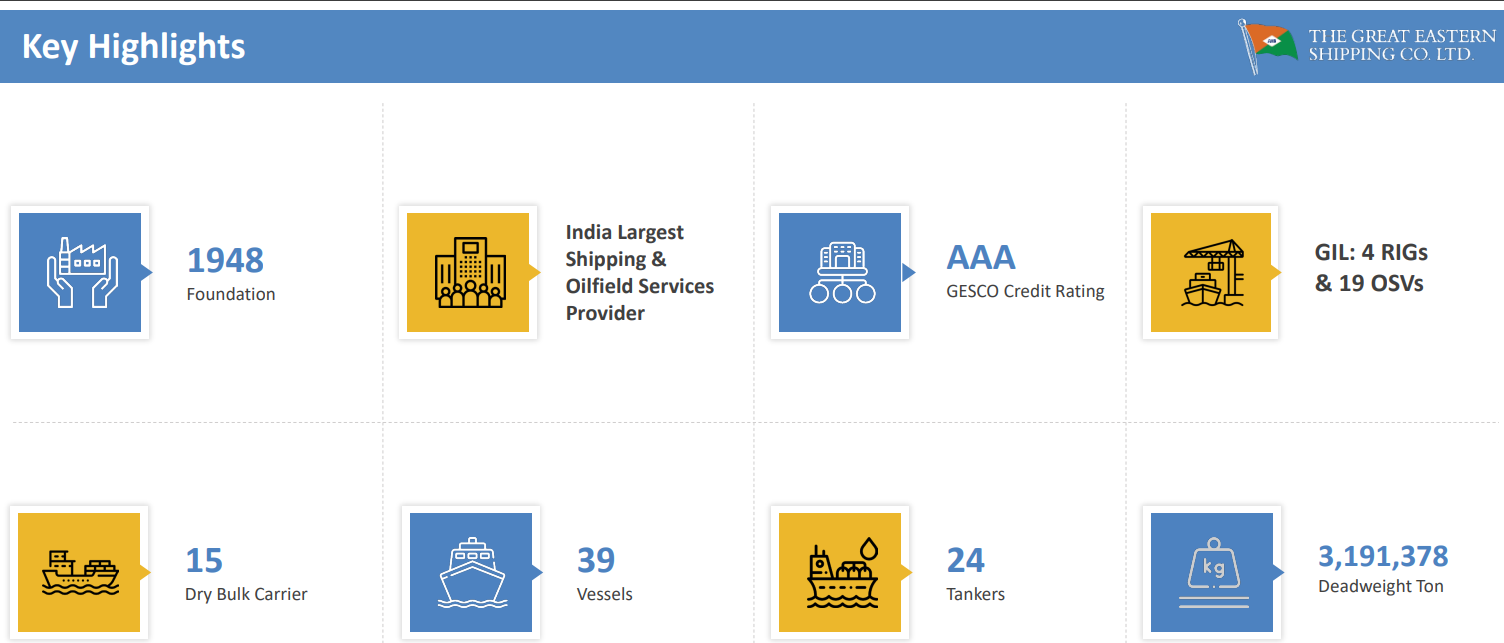

1. Shipping & Oilfield Services Provider

greatship.com | NSE: GESHIP

GE Shipping is India’s largest private-sector shipping and offshore oilfield services company. It operates through two major segments:

Shipping Business

GE Shipping operates a diversified fleet of 39 vessels with total deadweight tonnage of 3.19 million DWT.

Crude carriers — 5 vessels — 15.25 years average age

Product carriers — 15 vessels — 15.39 years

Gas carriers — 4 vessels — 17.27 years

Dry bulk carriers — 15 vessels — 11.62 years

Offshore Business

The offshore business is housed under Greatship India Ltd. It has:

Jack-up rigs — 4

Platform supply vessels — 4

Anchor Handling Tugs AHTSVs — 9

Multipurpose support vessels — 2

ROV support vessels — 4

This gives GE Shipping exposure to both global freight cycles and offshore oil & gas activity

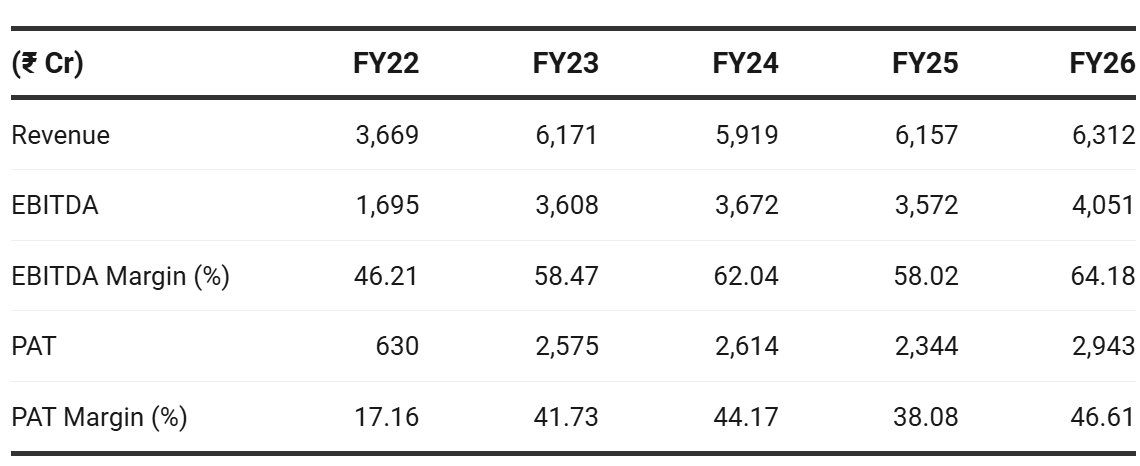

2. FY22-26: PAT CAGR 47% & Revenue CAGR 15%

GE Shipping’s last five years have been strong.

NAV rose from ₹538/share in FY21 to ₹1,796/share in FY26, implying a strong NAV compounding cycle.

NAV growth was not only due to fleet-value mark-to-market gains; a large part came from cash profits generated by ships over the cycle.

That matters because shipping companies are often valued by NAV.

If NAV growth is only due to asset-price inflation, it can reverse quickly.

But if ships are generating cash and converting that NAV into cash flow, the valuation base becomes more credible.

Still, the business remains cyclical. GE Shipping’s earnings are strongly linked to:

tanker freight rates,

dry bulk rates,

LPG rates,

offshore rig/vessel utilisation,

second-hand vessel prices,

forex movement,

ship sale gains.

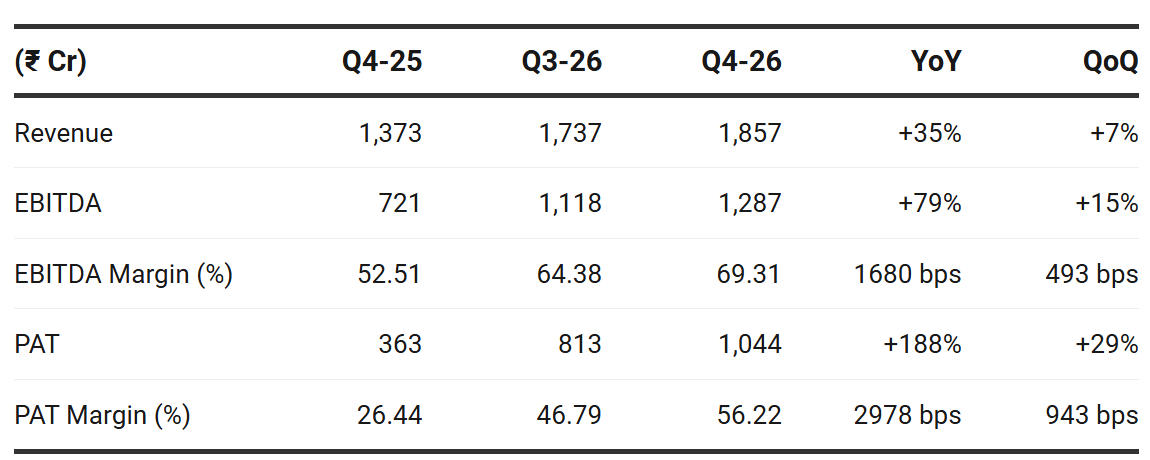

3. Q4-26: PAT up 188% & Revenue up 35% YoY

PAT up 29% & Revenue up 7% QoQ

Q4 was also helped by unusual market conditions.

Middle East disruption changed trade patterns, increased long-haul sourcing, tightened tanker and LPG markets, and caused a freight-rate spike in March and April.

Asset prices also rose by 10–20% during the quarter.

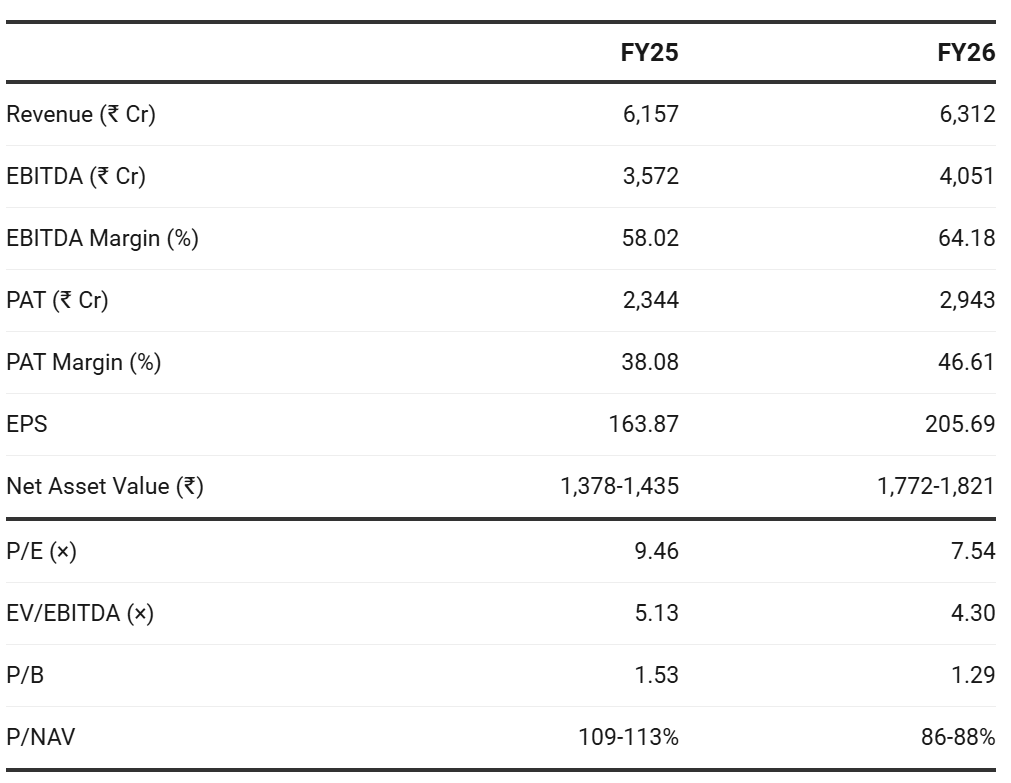

4. FY-26: PAT up 26% & Revenue up 3%

Profit grew much faster than revenue driven by strong margins, asset sale gains, forex gains, lower finance costs and favourable freight-market conditions.

Results are excellent — but it also means FY26 earnings should not be blindly treated as normalised earnings.

Normalised PAT grew from ₹2,437 Cr to ₹2,688 Cr, a much more modest increase of 10% than reported PAT.

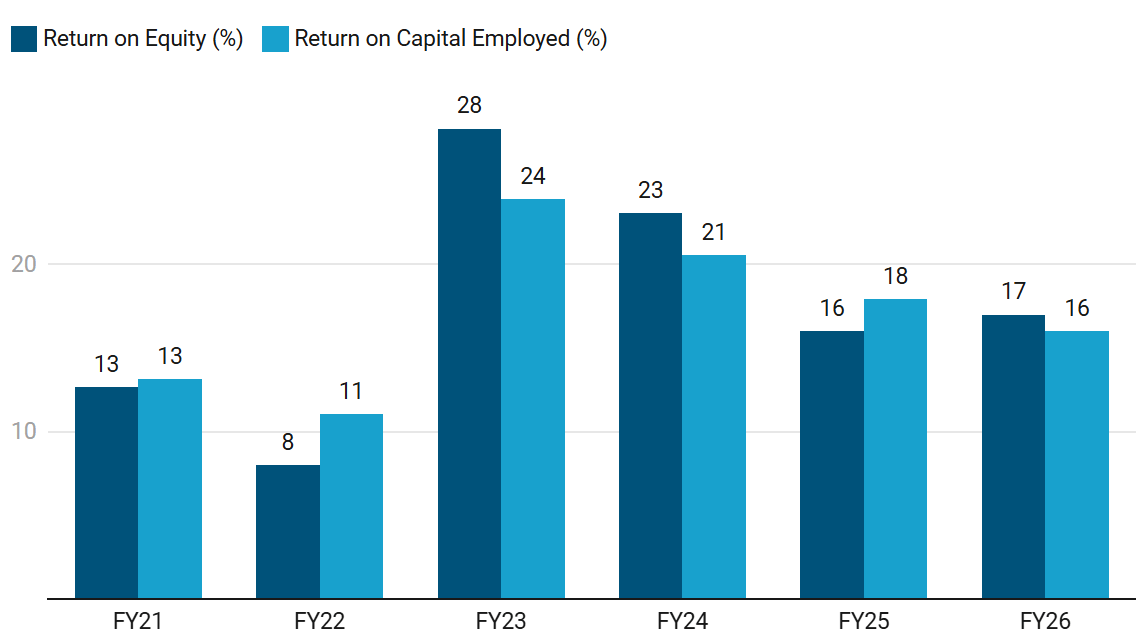

5. Business Metrics: Return Ratios Muted by Cash on Balance Sheet

Strong capital discipline and fleet optimization strategy

ROCE is especially useful here because GESHIP has large cash on books.

ROE can be diluted by excess cash sitting in equity. Despite that, the company delivered normalised ROCE of 17%.

That means the operating asset base — shipping fleet plus offshore assets — is earning strong returns in the current cycle.

But, shipping ROCE is not stable. It can fall sharply when freight rates fall or vessel values correct.

6. Outlook — Great Eastern Shipping Company

6.1 FY27 Outlook

GE Shipping enters FY27 with reasonable near-term coverage of capacity — Q1 FY27 operating-day coverage

Crude carriers 52%

Product carriers 66%

LPG carriers 100%

Dry bulk 76%

Offshore category Q1 FY27 operating-day coverage

Jack-up rigs 79%

AHTSV 89%

MPSVV 84%

PSV / ROVSV 97%

Management also said offshore vessel capacity is largely locked in for FY27, with about 80–85% of offshore vessel days covered.

This reduces near-term earnings risk.

Management is not giving formal earnings guidance because a large part of the fleet remains exposed to spot markets. That is deliberate.

GE Shipping prefers spot exposure because management believes spot markets outperform time-charter markets over long periods. The reason is simple: shipping markets can move violently during disruptions, and long-term charters often cap upside.

Management’s most important comment from the earnings call:

Current yield is a trap.

It means the company itself does not want to buy vessels only because today’s freight rates look attractive. Management said some of its best historical purchases happened when current yield was close to zero — in other words, when the market was weak and assets were cheap.

Capital allocation: disciplined, but asset prices are high

GE Shipping is selling older ships and replacing them with newer ships. Management calls these “switch transactions.” That is different from aggressive fleet expansion because the company is selling high and buying high, rather than only buying high.

The global orderbook is now rising. BIMCO says the global shipping orderbook reached a 17-year high by the end of Q1 2026, equivalent to 17% of the global fleet, boosted recently by record crude tanker contracting.

Management also said crude tanker supply risk is more relevant in CY27/CY28 and that it does not see major shipyard slippages yet.

So the correct view is:

FY27 macro is supportive, but FY28 supply risk is rising.

7. Valuation Analysis — GE Shipping

7.1 Valuation Snapshot

Current Market Price= ₹1550.7; Market Cap = ₹21,886.5 Cr

At a P/E of 7.4x Reported PAT vs a P/E of of 8.1x on Normalised PAT is is optically cheap. But GESHIP is a cyclical shipping company, so 7–8x earnings is not automatically cheap as FY26 is a favourable-cycle earnings year.

At 1.3x P/B , GESHIP is not deep value. This valuation is justified only if GESHIP can sustain mid-teens ROE. The company delivered normalised consolidated ROE of 17% and ROCE of 16% in FY26.

For shipping companies, P/NAV is more relevant than P/B, because ships are carried at depreciated historical cost in accounting books, while NAV reflects market value of fleet assets.

Current price is below consolidated NAV, so there is still NAV upside. But the discount is not huge. If vessel values fall 15–20%, this NAV cushion can disappear quickly.

GESHIP has large net cash. That makes EV-based valuation more attractive than market-cap-based valuation.

The operating business is not expensive on EV/core EBITDA.

Cash on balance sheet angle — This is the most interesting valuation lens.

The balance sheet shows cash & cash equivalents of ₹4,336.90 Cr, bank balances of ₹1,174.44 Cr, current investments of ₹2,391.53 Cr, and total borrowings of roughly ₹1,049 Cr.

That means 25–36% of the market cap is backed by cash / liquid treasury assets.

You are paying roughly ₹14,000–16,400 Cr for the operating shipping + offshore business, depending on how conservative you are with cash.

On ex-cash P/E, the operating business is available at ~5–6x normalised earnings. — That is attractive.

Free cash flow after asset sales in FY26 was ~₹1,276 Cr . GESHIP is available at a free cash flow yield of 5.83% which makes valuations quite attractive

But it is still a cyclical shipping stock.

At current levels current holders of the stock can keep riding the momentum seen in the stock price — till the sipping cycle supports

For new entrants — the cash-adjusted valuation makes the risk-reward attractive, but the stock is not cheap enough to ignore shipping-cycle risk.

7.2 Opportunity at Current Valuation

The biggest opportunity: cash-backed valuation

This is the strongest argument at current price.

The market is not giving full value to the cash-rich balance sheet. The stock looks fair on P/B, but attractive on ex-cash earnings.

NAV rerating opportunity

If FY27 earnings remain strong and vessel values do not correct sharply, the stock can rerate toward NAV.

FY27 earnings visibility is better than it looks — GESHIP enters Q1-27 with meaningful operating-day coverage:

The stock is not only trading cheap on past earnings; there is reasonable near-term visibility for Q1 FY27.

Spot-market upside remains open

Management prefers spot exposure because shipping rates can move sharply during disruptions. This is important because FY27 starts in a favourable macro environment:

tanker markets are benefiting from longer routes,

LPG remains strong,

dry bulk has been better than seasonal expectations,

offshore vessels are well-covered,

geopolitical disruption has created tonne-mile demand.

If disruption continues and spot rates stay strong, GESHIP can earn more than what fixed-charter companies can capture.

Offshore upside is underappreciated

The offshore business is not the main reason most investors buy GESHIP, but it is becoming more relevant.

Management said the offshore vessels business delivered its best profit since FY2016, and most vessel-side days for FY27 are already covered. It also noted that three rigs come up for repricing in FY27.

If rig repricing is favourable, offshore can add another earnings lever beyond shipping.

Capital allocation optionality

GESHIP has a net-cash balance sheet. Management said it remains prepared for both outcomes: if markets stay strong, spot exposure helps; if markets weaken, cash can be used to invest.

GESHIP is positioned to buy assets when weaker players are stressed. This is the long-term opportunity beyond FY27 earnings.

GESHIP is still an opportunity at current valuations, but not a screaming bargain. The stock is attractive on ex-cash valuation and P/NAV, fair on P/B, and risky on shipping-cycle normalisation. For a fresh investor, the right approach is staggered entry, not aggressive buying.

7.3 Risks at Current Valuations — GESHIP

NAV risk: current discount can vanish if vessel values correct

The strongest valuation support is consolidated NAV of around ₹1,796/share. At ₹1,550, the stock trades at about 0.86x NAV.

But shipping NAV is linked to vessel values. Management said asset prices rose 10–20% during Q4 because of tight markets and Middle East disruption.

A 15–20% correction in vessel values can wipe out the apparent NAV discount.

“Current yield is a trap” risk

Management’s most important warning was that current yield can be a trap. They said the company has historically done best on purchases when current yield was close to zero, not when freight rates were already strong.

This applies to investors too.

At current price, GESHIP looks cheap on FY26 earnings. But FY26 was a favourable cycle year.

Investors may be buying a low P/E that is based on unusually high earnings.

Orderbook risk rises in CY27/CY28

Management said the orderbook has built up, especially in crude tankers, and supply risk is mainly a CY27/CY28 issue. It also said scrapping is low because markets are strong.

GESHIP also highlights high orderbook levels across key vessel categories, especially LPG.

FY27 may remain strong, but FY28 can become more difficult if new vessel supply arrives while disruption-led demand fades.

Cash on balance sheet is a cushion, not fully surplus cash

The cash-backed valuation is attractive. GESHIP has strong cash + bank balances and around ₹7,903 Cr including current investments. This makes ex-cash valuation look cheap. But all cash is not surplus. Shipping companies need cash for:

fleet replacement,

dry-docking,

downturn survival,

offshore asset deployment,

opportunistic vessel purchases,

dividends and possible buybacks.

Deducting all cash from market cap may overstate the margin of safety. Some cash is strategic operating capital.

Offshore repricing risk

The offshore business is a positive, but it has specific FY27 risks. Management said three rigs come up for repricing in FY27: one has completed a short-term contract and is awaiting next business, while two come off in the second half. It also discussed ONGC tender uncertainty.

If rig repricing is weaker than expected or tender delays continue, offshore profitability may not improve as much as the market expects.

Q1 FY27 coverage helps, but does not remove cycle risk

GESHIP has good near-term coverage for Q1 FY27 — this protects near-term revenue visibility.

But it does not protect full-cycle valuation.

Q1 FY27 can be strong while FY28 still weakens due to freight normalisation or new supply.

The real risk is valuation-cycle risk: investors may be valuing FY26/FY27 earnings and NAV as if they are sustainable mid-cycle numbers.

At current valuations, GESHIP is still attractive on ex-cash valuation and P/NAV, but the margin of safety is not deep enough to ignore cyclicality.

The downside risk comes from freight-rate normalisation, vessel-value correction.

Previous Coverage of GESHIP

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer