Freshara Agro FY26 Results: PAT up 30%, Up to 50% Growth in FY27

Guidance of up to 50% FY27 revenue growth. Even though quality of earnings were weak in terms of cash-flow. Freshara Agro is available at attractive valuations

1. Exporting Preserved Gherkins & Pickled Vegetables

fresharaagroexports.com | NSE - SME: FRESHARA

3rd Largest Gherkin Exporter

Specializes in procurement, processing, and exporting preserved gherkins and pickled vegetables.

2 facilities in Tirupattur, Tamil Nadu

Exports to 40+ countries, including Europe, USA & Russia.

FY26:

Completed the acquisition of Aceitunas Sarasa, S.A.U., a Spanish company with expertise in the B2C segment of table olives and gherkins in Spain.

Acquisition is expected to strengthen Freshara’s presence in the Spanish olive market while also enhancing the European and global footprint for gherkins exported from India.

Acquisition enables Freshara to unlock value as it seeks to establish a stronger presence in countries where olives are a preferred consumer product and where gherkins are expected to gain increased traction through access to a broader customer base and established distribution network.

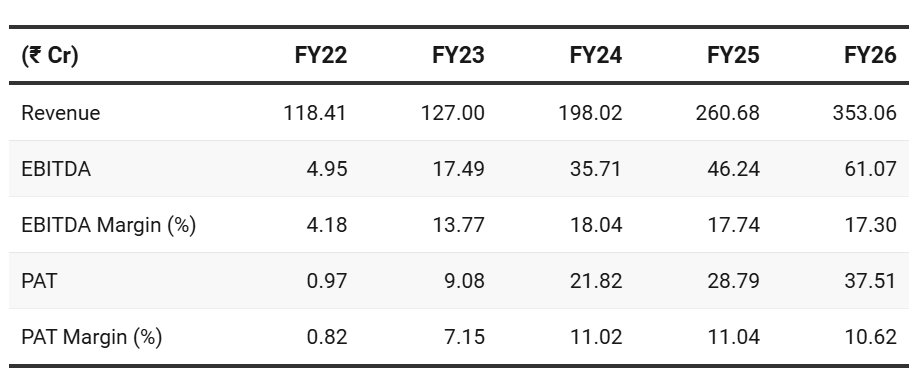

2. FY22–26: PAT CAGR of 149% & Revenue CAGR of 31%

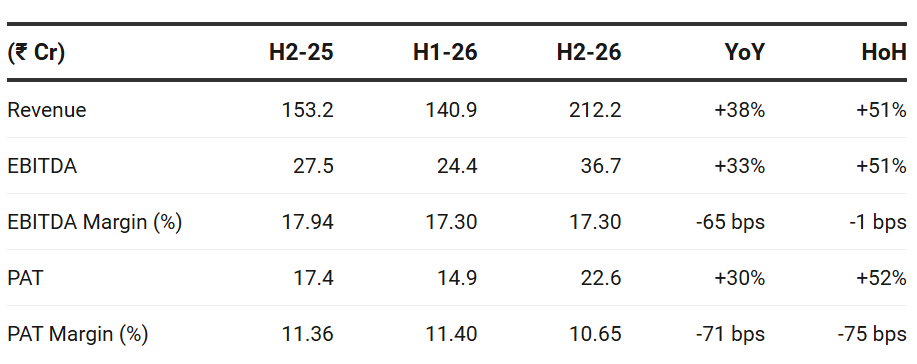

3. H2 FY26: PAT up 30% & Revenue up 38% YoY

PAT up 51% & Revenue up 51% HoH

4. FY26: PAT up 30% & Revenue up 35% YoY

The weakening margin story has a counterintuitive structure

Gross margin— consolidated wins

Spain’s branded olive business, selling 97% B2C directly to supermarkets, has an implied gross margin of 46.5% — more than double India’s 22.3%.

This pulls the consolidated gross margin up to 24.3%. Olives as a product command structurally better gross economics than bulk gherkin exports.

This is the long-term case for the acquisition.

The weaker consolidated margin is not only because Spanish numbers were included for the last 10 weeks of Q4-26. It is because the Spain business, during the included period, added revenue but at lower operating/PAT margin after overheads, finance cost and integration costs.

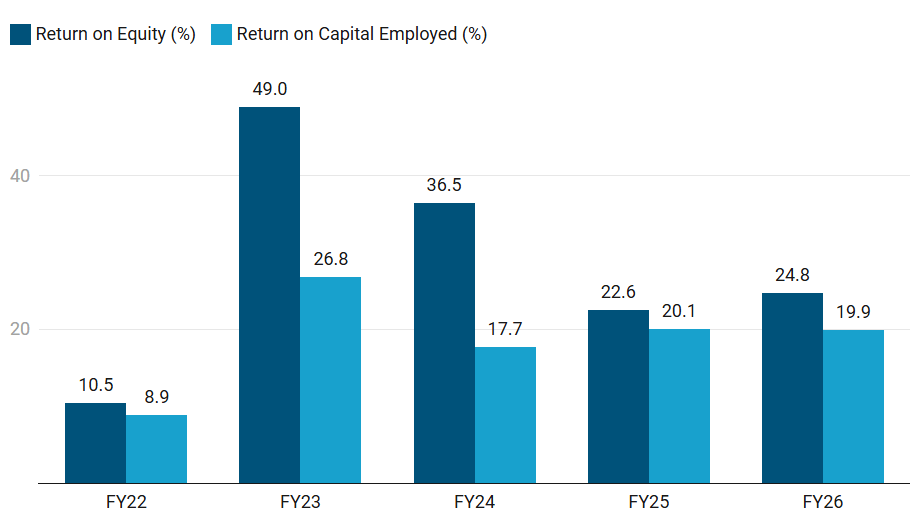

5. Business Metrics: Strong Return Ratios

6. Outlook: Revenue growth of upto 50% for FY27

6.1 Management Guidance — Freshara Agro Exports

Highly optimistic about the revenue growth prospects.

Combined business operations could contribute to growth of up to 50%

Driven by increasing exports to global markets and expectations of improved margins during the current year

Implemented the Jar Packing operations at its second production unit, thereby enhancing its production capabilities and strengthening its operational infrastructure

6.2 Performance vs FY26 Guidance

Partially delivered FY26 guidance

Revenue: growth of 35% in FY26 vs guidance of 30% growth

supported by inorganic growth due to the Spanish acquisition

Weaker Margins: Spanish acquisition impacted consolidated margins while the the standalone margins remained strong

Capacity Expansion delivered — will support growth till FY27

7. Valuation Analysis

7.1 Valuation Snapshot — Freshara Agro Exports

CMP ₹214; Mcap ₹502.88 Cr;

Assumptions:

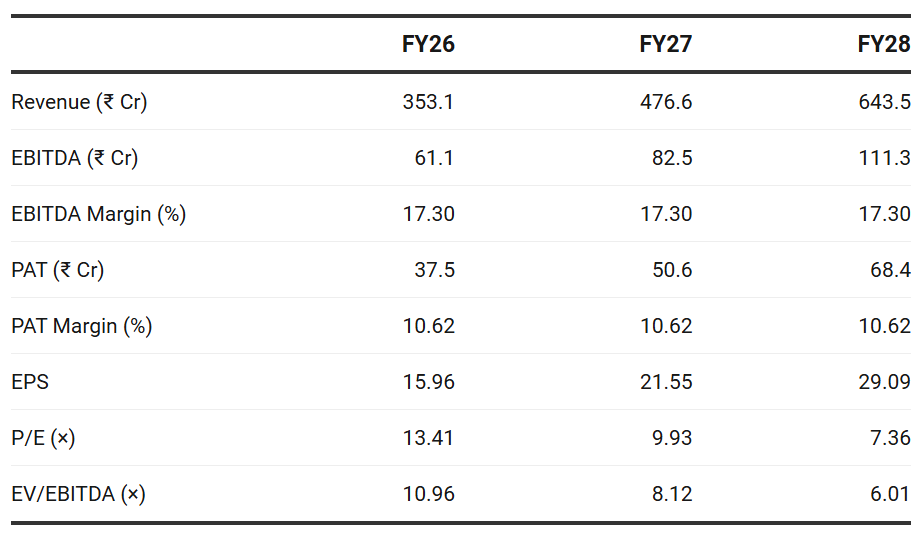

Conservative growth of 35% on consolidated basis against the management guidance of up to 50% growth in FY26

Growth is conservative given the FY22-26 track-record of delivering ~30% revenue CAGR in-line with the 35% growth in FY26

Conservative assumption of stable margins even though management is guiding for stronger margins

Attractive Valuations:

Freshara looks attractive on FY26 multiples, and also at forward valuations multiples given the business is expected to growth at 35%.

Scope for valuation re-rating if FY26 guidance is delivered

Valuations are undemanding — provide flexibility to sustain periods where performance is not as per guidance

Freshara, is trading at a discount

reflecting its smaller scale

question marks on its ability to deliver a smooth integration on the Spanish acquisition

limited track record as listed company

Looking undervalued on FY26 and FY27E basis provided execution stays on track. Multiples leave significant room for re-rating. — opportunity of a serious upside.

7.2 Opportunities at Current Valuation

FY27 growth can make current valuation look cheap: Trading at a discount for a company guiding to grow ~50% till FY27 with margin expansion

Management guidance for margin expansion

Margin expansion opportunity from jar packing + B2C Spain

Freshara implemented jar-packing operations at its second production unit in FY26. Management says this strengthened production capability and operational infrastructure. It also acquired the business of Aceitunas Sarasa, which gives access to Spain’s B2C table olives and gherkins market.

Significant runway for growth and margin expansion if it leverages the olives brand to transition from a B2B supplier of gherkins to a B2C brand

7.3 Risks at Current Valuation

Negative operating cash flow

Massive working capital build-up (inventory +receivables) is consuming cash.

Profit is on paper, not in the bank.

Cash erosion

The company is fully reliant on debt to fund operations, creating refinancing exposure.

Inventory concentration risk:

Inventories went up 2.7x to ₹144 Cr in FY26 from ₹54 Cr in FY25.

Management attributes this to proactive stockpiling against crude oil & geopolitical risk — but this is a drag on working capital

In February 2026, Management made a strategic decision to proactively increase inventory levels for raw and packaging materials This conscious stockpiling was executed to hedge against polentiaJ supply chain disruptions and anticipated hikes in crude oil prices stemming from geopolitical tensions between the US and Iran. Consequently, this short-term investment in safety stock is reflected as an increase in working capital on the Balance Sheet

Integration risk — Spanish acquisitions

Two Spanish entities (Conservas Selectas Españolas, Gandin Invest) acquired Jan–Feb 2026.

First-ever consolidated financials — no prior year comparison.

Integration, culture, and regulatory complexity is high.

High leverage & borrowings

Consolidated short-term and long-term borrowings: ₹14,121L. LT borrowings jumped up.

Total debt to equity is stretched.

Finance costs more than doubled in FY26 over FY25.

Receivables concentration

Trade receivables — FY26 at ₹149.92 Cr.

At 42% of revenues, collection risk and debtor days have worsened.

Equity dilution

23.16L fully convertible warrants at ₹168/share issued Mar 2026. On conversion, equity base expands. Full dilution impact not yet reflected.

Previous Coverage of Freshara Agro Exports Ltd

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer