D.P. Abhushan FY25: PAT Up 82%, Expansion & Premium Product Mix to Drive FY26 Growth

To double stores via QIP, expand in Tier-2/3 cities, push diamond sales and higher margin jewelry to sustain margins. Sustained high prices could damped demand

1. Jeweler

dpjewellers.com | NSE: DPABHUSHAN

2. FY21–25: PAT CAGR of 42% & Revenue CAGR of 29%

Revenue Growth: Driven by retail expansion, higher gold prices, and consistent demand across urban and semi-urban regions.

Margin Expansion: Cost optimization and rising contribution from higher-margin segments (e.g., diamonds).

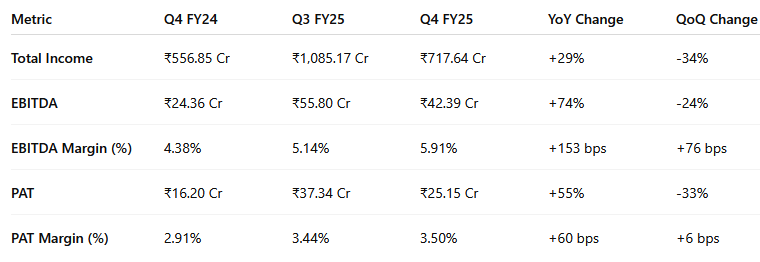

3. Q4-25: PAT up 55% & Revenue up 29% YoY

Strong Year-on-Year Performance: PAT surged 55% YoY despite a sequential dip post festive demand normalization.

Margin Momentum Holds: PAT margin improved steadily to 3.50%, sustaining gains from Q3 and signaling resilient core profitability.

QoQ Decline is Seasonal: Operational strength reflected in margin expansion and YoY outperformance.

4. FY25: PAT up 82% & Revenue up 42%

Accelerated Growth Across the Board: Outpacing prior years on the back of both volume and value growth.

Margin Resilience Despite Volatility: The company held margins even amid high gold price volatility and macro headwinds — a testament to operational discipline and pricing power.

5. Business Metrics: Steady Return Ratios with Capital Efficiency Intact

Capital Productivity Reaffirmed: Both ROCE and ROE have remained consistently strong over FY21–25

FY25 Surge in Returns:

ROCE expanded to 36.1%, driven by sharp improvement in operating profit (EBIT up 64%) and disciplined capital deployment.

ROE jumped to 35.1%, aided by robust PAT growth (+82%) and limited equity dilution — signaling superior shareholder value creation.

Leverage Used Efficiently: Capital employed rose due to higher inventory and expansion capex, but profit growth outpaced asset growth — boosting return ratios.

6. Strong outlook: Rising gold prices, store expansion & higher margin categories

6.1 D.P. Abhushan – FY25: Expectations vs. Performance

Strategic Wins:

Delivered far beyond guided growth while maintaining financial discipline.

Store-level scale benefits and product mix shift (toward diamonds, Polki, wedding sets) supported margin expansion.

Inventory accounting policy (WAC) creates a built-in cost advantage vs market price volatility.

Monitor in FY26:

Execution of 10-store rollout from QIP proceeds

Early traction in franchise model

Stability in discretionary demand amidst persistent gold price elevation

6.2 Future Outlook: Scaling with Discipline Amid Price Volatility

A. Revenue Growth Outlook

Management is targeting 20–25% CAGR over the next 2–3 years.

This is underpinned by:

Continued store expansion across Central and Western India.

Strategic shift toward higher-value product categories like diamonds, Polki, and bridal collections.

Rising demand for premium formats (18-carat, rose gold, white gold) among urban millennials.

B. Store Expansion Pipeline

₹600 Cr QIP proceeds will fund 10 new stores (5 large format, 5 small), and support ongoing inventory buildup.

Plan to double store count in 2–3 years.

Early-stage franchise model being tested with 2–3 stores expected in next 24 months.

C. Margin & Profitability

Gross margins expected to improve further as diamond share rises from 6% → 15%.

Weighted average inventory accounting offers built-in buffer during periods of gold price inflation.

Operating leverage from new stores expected to sustain EBITDA margin >5% even with rising costs.

D. Key Risks

Sustained high gold prices may depress volumes in value-conscious segments.

Working capital cycles may tighten in FY26 due to elevated inventory if demand softens.

Execution risk from aggressive expansion and franchise integration needs to be closely monitored.

E. Overall Strategic Positioning

D.P. Abhushan is well-positioned to transition from a high-growth regional player to a national jewellery retail brand, with strong brand equity in purity, design, and transparency. The next phase of growth will depend on disciplined execution, margin defense, and how effectively it scales its omnichannel and franchise strategy.

7. Valuation Analysis

7.1 Valuation Snapshot

D.P. Abhushan’s current valuations—though rich on traditional multiples—are justified by:

Strong return ratios (ROE/ROCE above 35%)

Strong execution track record with 42% revenue and 82% PAT growth in FY25

A well-defined growth pipeline: 10 new stores, early franchise rollout, and margin expansion from premium jewellery categories

The ₹600 Cr QIP will further strengthen its balance sheet and fund capital-light expansion, reducing risk and enhancing return potential. If store ramp-up and diamond share increase as planned, valuation multiples could sustain or even expand.

7.2 What’s Priced In

Strong execution + category leadership: The company has delivered consistent double-digit PAT growth and stable margins while expanding into premium product categories like diamond, Polki, and wedding jewellery.

High return ratios: Sustained ROE of 35.1% and ROCE of 36.1% reflect strong operational efficiency, justifying premium valuation multiples.

Inventory and pricing strategy: Use of weighted average inventory accounting helps maintain inventory cost below market during gold price surges, offering a built-in margin cushion — this is reflected in investor expectations for margin stability.

Growth visibility: Market is likely pricing in the 20–25% CAGR revenue guidance, supported by internal accruals, QIP-funded store rollout, and demand momentum in wedding jewellery.

Balance sheet strength: A Net Debt/Equity of 0.41x pre-QIP indicates ample headroom for expansion without balance sheet stress.

Network expansion: Execution of flagship store in Ratlam and new launches in Neemuch and Ajmer validate the company’s ability to scale physical presence efficiently.

7.3 What’s Not Priced In

Diamond Jewellery Scaling: The planned increase in diamond jewellery share from 6% to 15% could materially enhance margins and elevate ASPs, especially in urban stores.

QIP-Driven Acceleration: The ₹600 Cr QIP is expected to fund 10 new stores over the next 2–3 years. Early execution success could lead to earnings surprise and faster store-level breakeven.

Franchise Model Upside: The company is piloting a franchise model (2–3 stores planned). If successful, it could unlock a capital-light growth engine not yet factored into valuations.

Premiumization Demand Shift: Rising urban preference for 18-carat, rose gold, and white gold jewellery is still an evolving trend. Increased traction could expand gross margins and reduce working capital intensity.

Omnichannel Scaling: Digital initiatives and branding efforts haven’t been monetized yet. Stronger online presence could complement store productivity and attract younger consumers.

Potential Re-rating: If PAT continues compounding above 30% in FY26 with stable margins, the stock could see a P/E re-rating toward 35–38x, particularly if new store productivity surprises on the upside.

8. Implications for Investors: What to Watch

8.1 Bull, Base & Bear Case Scenarios

8.2 Reasons to Stay Invested or Add

Strong Earnings Momentum

PAT grew 82% YoY in FY25, with scope for further compounding as new stores scale and higher-margin products gain traction.Capital-Efficient Growth

ROE and ROCE at 35.1% and 36.1%, respectively — among the highest in retail — reflect disciplined execution and margin-led expansion.Clear Growth Visibility

Management aims to double store count in 2–3 years, backed by a ₹600 Cr QIP. This is expected to fuel sustained 20–25% CAGR topline growth.Product Mix Transformation

Strategic focus on diamonds, Polki, designer jewellery, and 18-carat formats to lift gross margins and enhance brand stickiness.Structural Demand Tailwinds

Increasing disposable incomes, urban weddings, and aspirational gold demand support a secular growth trend in organized jewellery retail.Inventory Advantage

Use of weighted average cost (WAC) accounting creates a natural hedge during gold price surges, preserving margin stability.

8.3 Key Risks & What to Monitor

Gold Price Volatility

Sustained high bullion prices could suppress mass-market demand, especially in entry-level wedding jewellery — watch for Q1FY26 trends.Execution Risk from Expansion

Timely launch and ramp-up of 10 new stores (company-owned and franchise) will be crucial. Any delay may compress FY26 revenue visibility.Inventory Build-Up

FY25 saw a 59% YoY rise in inventory; liquidation pace and working capital management will be key to protecting cash flow in FY26.Franchise Rollout Uncertainty

The franchise model is in its infancy. Poor partner selection, operational inconsistency, or weak branding control may impact scale-up.Demand Sensitivity

Jewellery demand remains discretionary and sentiment-driven. Macroeconomic pressure or a muted festive season could derail quarterly momentum.Valuation Compression

At ~30x P/E, valuation leaves limited room for error. Any earnings miss, execution hiccup, or slowdown in premium mix adoption may trigger a de-rating.

Watch out for

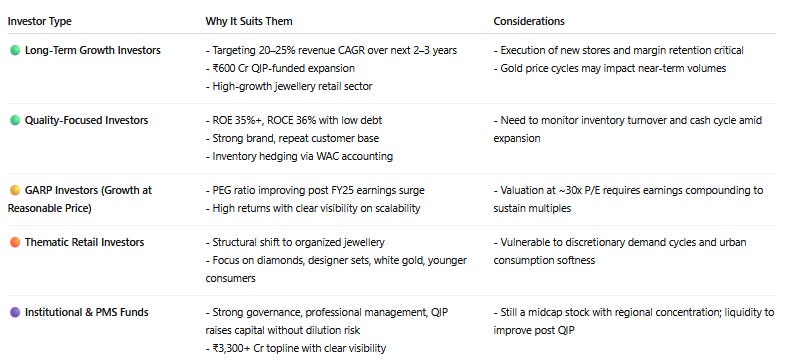

8.4 Investor Segmentation Outlook – D.P. Abhushan

Previous coverage of DPABHUSHAN

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer