DP Abhushan: PAT growth of 92% & revenue growth of 45% in 9M-25 at a PE of 29

Outperforming guidance of 20-25% growth in FY25. QIP to double store count, expand into Tier-2 & Tier-3 cities, push higher-margin diamond jewellery, while maintaining margins & growth

1. Jeweller

dpjewellers.com | NSE: DPABHUSHAN

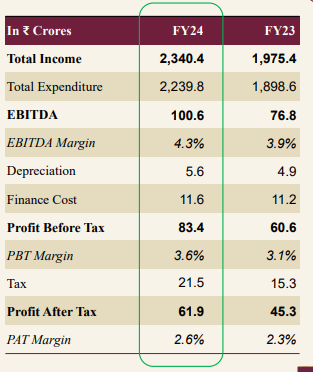

2. FY21-24: PAT CAGR of 33% & Revenue CAGR of 24%

3. FY24: PAT up 44% & Revenue up 61% YoY

4. Q3-25: PAT up 123% & Revenue up 42% YoY

5. 9M-25: PAT up 92% & Revenue up 45% YoY

6. Business metrics: Strong return ratios

7. Outlook: Revenue CAGR of 20-25%

Management Guidance & Strategic Outlook

Growth

Targeting 20–25% annual revenue growth, despite already delivering a 45% YoY growth in 9MFY25.

Management remains conservative in guidance but confident in outperforming targets.

Store Expansion

To double number of stores in the next 2–3 years.

Rs 600 cr is being raised via QIP (Qualified Institutional Placement):

Primarily for inventory financing and store CAPEX.

Expected to fund 10 new stores (5 large and 5 small).

Franchise Model

Early-stage rollout: planning 2–3 franchise stores in the next 2 years.

Focus is initially on company-owned stores; franchises are an additional leg of growth.

Product Mix Optimization

Strategic push into higher-margin jewellery categories:

Wedding jewellery (contributing 50–55% of sales)

Diamond-studded, Polki, and designer jewellery

Increasing revenue share from diamond jewellery from 6% to 15%

Growing demand for 18-carat, rose gold, and white gold jewellery from younger consumers.

Margin Improvement

Gross margin improved due to:

Focus on higher-margin products

Economies of scale in newer stores

Use of weighted average inventory accounting provides natural hedging, keeping inventory cost ~8–10% lower than market price.

8. PAT growth of 92% & Revenue growth of 45% in 9M-25 at a PE of 29

9. Hold?

If I hold the stock then one may continue holding on to DPABHUSHAN.

Based on 9M-25 performance one can look forward to a strong FY25 with DPABHUSHAN outperforming the guidance of 20-25% growth.

Guidance of 20–25% sustained growth looks achievable with new stores and higher-margin products.

DPABHUSHAN has a strong outlook for growth given its plan to double store count in 2–3 years with Rs 600 cr QIP-funded rollout for expansion in Tier 2/3 cities (MP, Rajasthan, Gujarat, Chhattisgarh) with low competition from national brands.

One needs to keep a watch out for delays in store rollouts, especially in Tier 3 towns. New stores take 6–9 months to break even and heavy inventory investment is needed.

QIP could dilute EPS temporarily and cap near-term upside. However, the longer term growth momentum should cover the temporary dilution of EPS.

Growth is to be supported by improving EBITDA margins as the product mix is improved with a higher diamond/studded jewellery mix

Sectoral tail winds are supporting DPABHUSHAN

Shift from unorganised to organised retail: expected 50% market share by FY29.

Gold/jewellery demand supported by weddings, culture, rising income.

One must watch out for higher prices suppressing discretionary demand.

Before the current pull back in DPABHUSHAN, the stock was up 2x in 12 months and hence one should be ready for some time of consolidation

Things to watch out for in DPABHUSHAN

10. Buy?

If I am looking to enter DPABHUSHAN then

DPABHUSHAN has delivered PAT growth of 92% & Revenue growth of 45% in 9M-25 at a PE of 29 which makes valuations acceptable in the short term.

DPABHUSHAN is guiding for 20-25% revenue CAGR which at a PE of 29 which makes valuations attractive over the longer term.

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

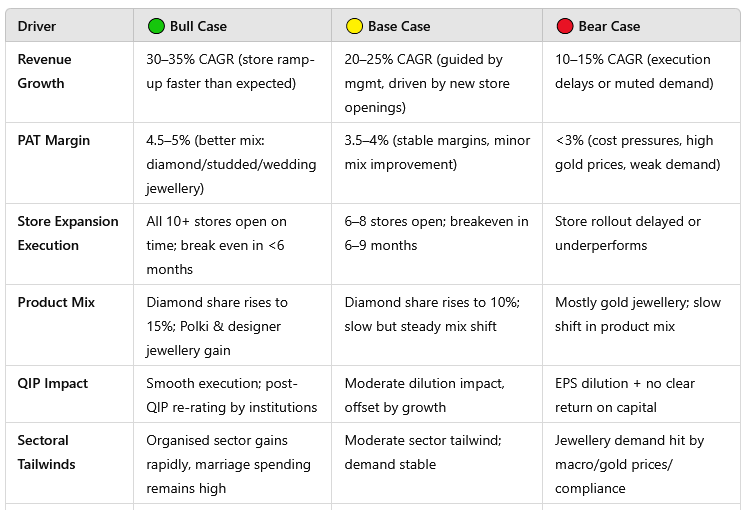

Loved the table showing Bull, Bear and Bass Case.