BLS International Services: PAT up 74% & Revenue up 25% in H1-25 at PE of 38

Guiding 50-60% PAT growth & revenue growth of 20-30% in FY25. EBITDA margin expansion to 25-27%. FY26 growth guidance of 25%. Growth driven by visa & consular business while digital business struggled

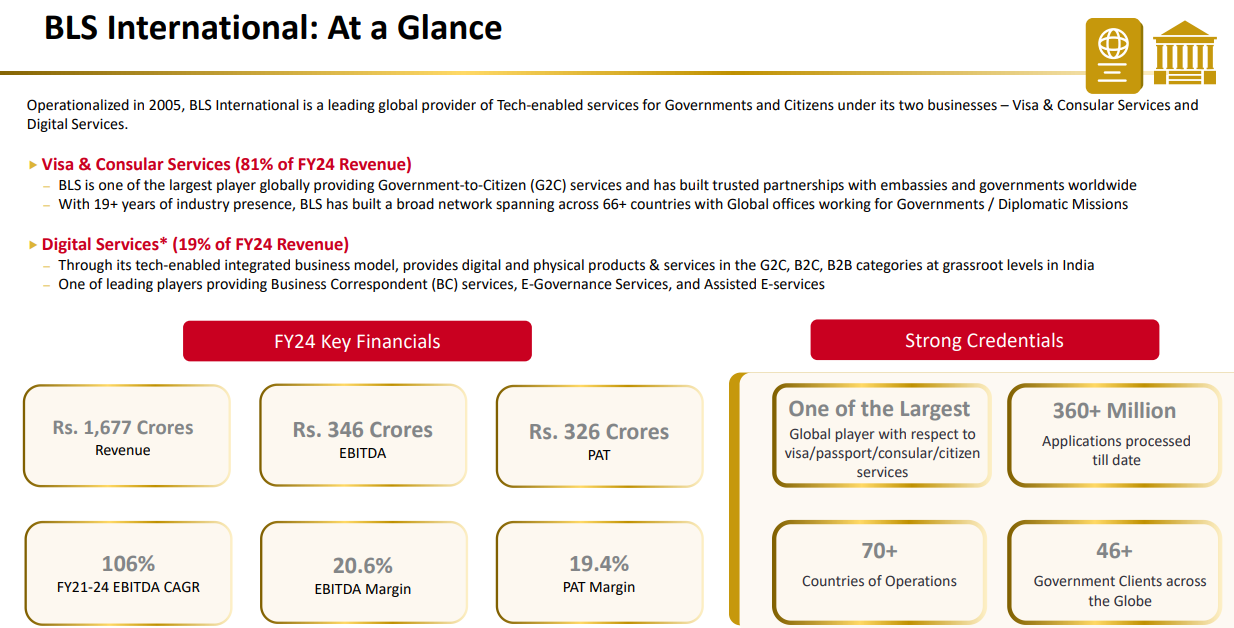

1. Visa & consular services | Digital services

blsinternational.com | NSE: BLS

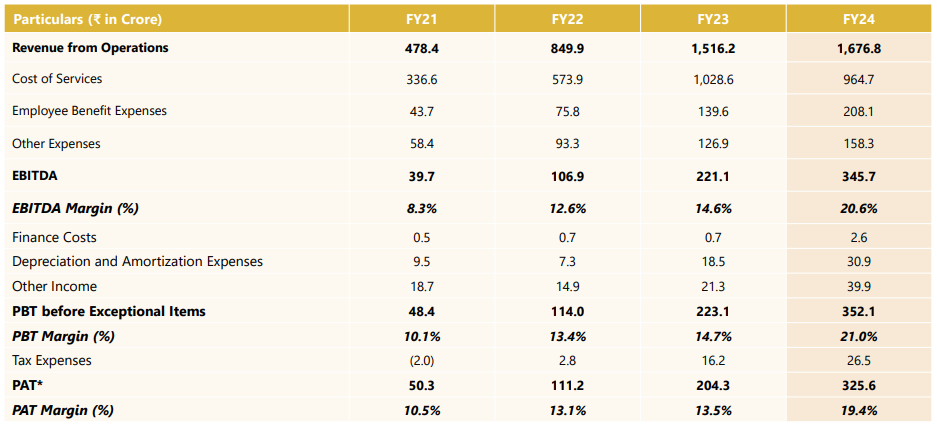

2. FY21-24: PAT growth 86% & Revenue growth 52% CAGR

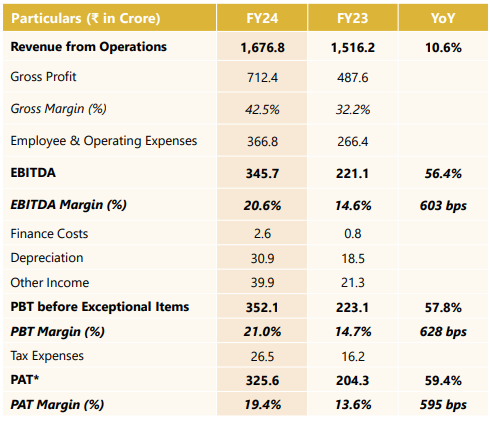

3. FY24: PAT up 59% and Revenue up 11%

4. Q2-25: PAT up 78% and Revenue up 21% YoY

PAT up 21% and Revenue up 0.5% QoQ

5. H1-25: PAT up 74% and Revenue up 25% YoY

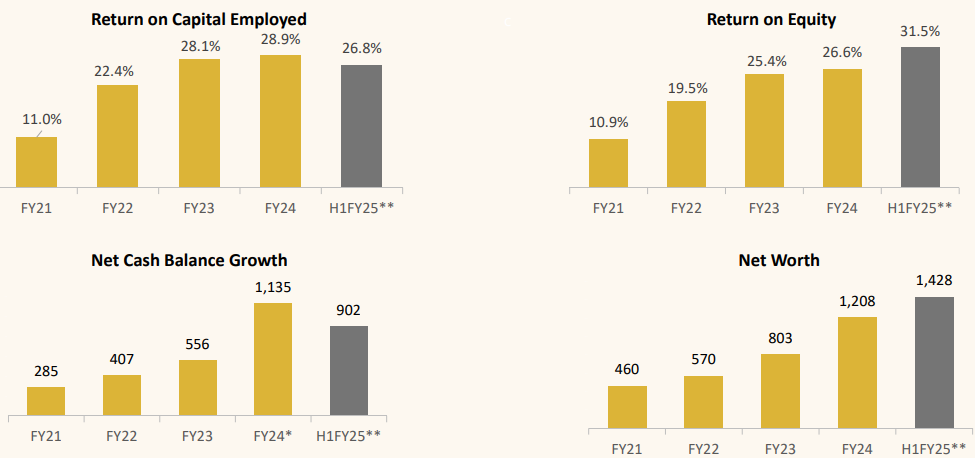

6. Business Metrics: Strong & improving return ratios

Ours is a negative working capital cycle. So we don't need money for the working capital.

7. Outlook: 50-60% PAT growth & 20-30% revenue growth in FY25

i. FY25: Revenue growth of 20-30%

Management expressed confidence in maintaining the growth trajectory observed in the first two quarters of FY25, characterized by a 20-30% revenue increase. This growth is attributed to strong performance in the visa and consular services business, contributions from recent acquisitions, and ongoing operational improvements.

ii. FY25: PAT growth of 50-60%

Will Maintain The Last 3 Year Profit After Tax CAGR Of 50-60% In FY25

For FY24, we closed at INR 325 crores of PAT, so which was a 60% growth compared to last year. So whatever we have achieved last year, our objective will be to maintain that.

First of all, as a company, I personally look at more EBITDA and PAT numbers. I feel we have done a 60% growth at EBITDA level. And a year before that, we also did more than 100% growth in EBITDA. So that is what we are focused on. And I feel definitely this year also, we will surpass the numbers that we achieved last year.

iii. FY25: EBITDA Margin expansion of 25%+

EBITDA margin in FY25 to be maintained at 25-27%+ compared to 20.6% in FY24 and 27% in Q1-25.

Our intention is to be around 25% - 27%. That is our target to reach immediately. And then let's see from there how we can improve it further.

iv. FY26: Revenue growth of 25%

The company aims to maintain a 25% revenue growth rate in FY26, fueled by a combination of organic growth in existing businesses, contributions from acquisitions, and securing new contracts.

8. PAT growth of 74% & Revenue growth of 25% in H1-25 at a PE of 38

9. Hold?

If I hold the stock then one must question holding on to BLS.

H1-25 has been strong and is in line with the guidance given by the BLS management.

Outlook is strong with the BLS management sticking to a 50%+ PAT CAGR with a 25% revenue growth

If you have seen in the last 3-4 years we have given more than 50% CAGR growth, and next year also coming years our objective is obviously to grow the company. We cannot give you any firm numbers or percentages where target to grow, but definitely we have aggressive growth internally set within the company.

The underlying business momentum is strong with the management confirming during the earnings call that the organic growth in terms of visa application volume was 18%.

BLS has a visa outsourcing contract with the Spanish government. As per the management the Spain contract contributes to 25-30% of overall revenues. This contract needs to be watched very closely as it can materially impact the business of BLS

One needs to watch out for the weak performance of the Digital Services business. Digital Services has been a drag on the overall business and can seriously dent overall performance if the trend continues.

10. Buy?

If I am looking to enter BLS then

For a PAT growth of 74% and revenue growth of 25% in H1-25, the PE of 38 looks reasonable.

For a FY25 guidance of 50-60% PAT growth with 25% revenue growth, the PE of 38 looks reasonable.

For a FY24-26 revenue CAGR of about 25%, the PE of 38 looks reasonable.

BLS has generated Rs 328.6 cr of free cash flow as of Q2-25 end and is available at a market cap of Rs 16,062 cr. This translates into a free cash flow yield of 2% (not annualized) which makes the valuations reasonable.

At a 38 PE the margin of safety is limited and a weak quarter can impact the stock price significantly.

Previous coverage of BLS

Don’t like what you are reading? Will do better.` Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

You guys must be congratulated. You spotted and advocated BLS International almost 2 weeks ago. I agreed with your rational and entered the BLS International counter abd pretty happy with it. ET and other reputable stock advisories are recommending BLS International now. In our world today, stock advisories are dime a dozen and if they are doing anything making Indians gamblers. Quality has its own language which tells.