Bank of Maharashtra Q3 FY26 Results: PAT up 27%, FY26 Guidance on Track

Solid execution in 9M FY26 with ROA and NIM above guidance. Strong execution against FY26 guidance. Valuations leaves room for re-rating.

1. Public Sector Bank

bankofmaharashtra.in | NSE: MAHABANK

Products & Services

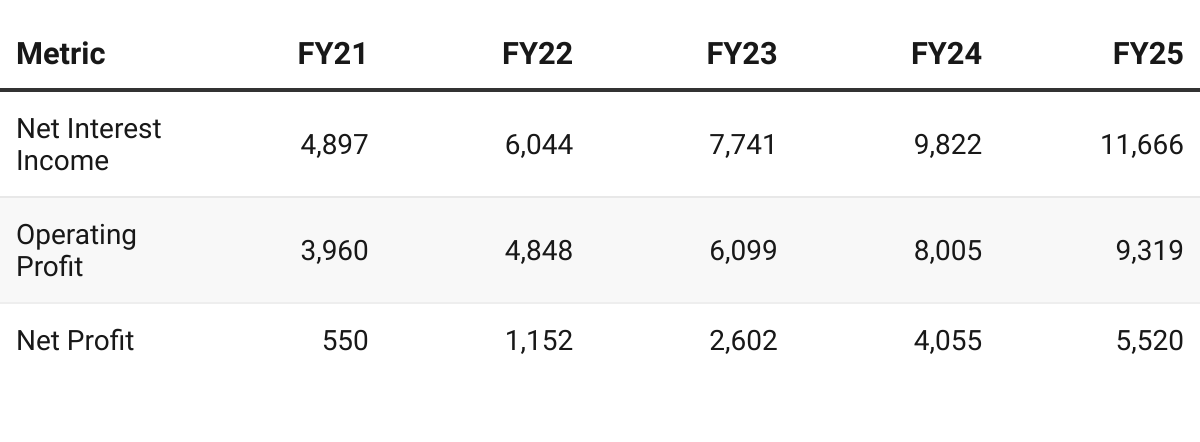

2. FY21-25: PAT CAGR of 96% & Net Interest Income CAGR of 24%

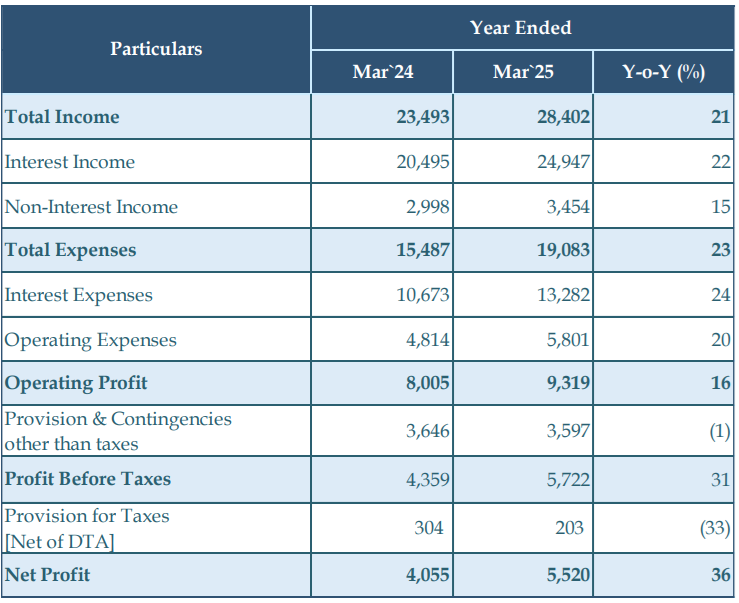

3. FY25: PAT up 36% & Net Interest Income up 19% YoY

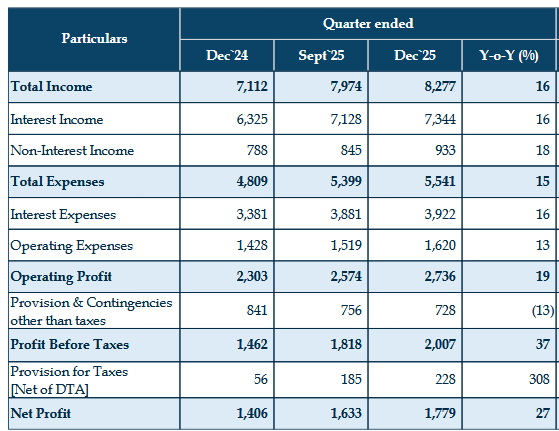

4. Q3-27: PAT up 27% & Net Interest Income up 16% YoY

PAT up 9% & Net Interest Income up 5% QoQ

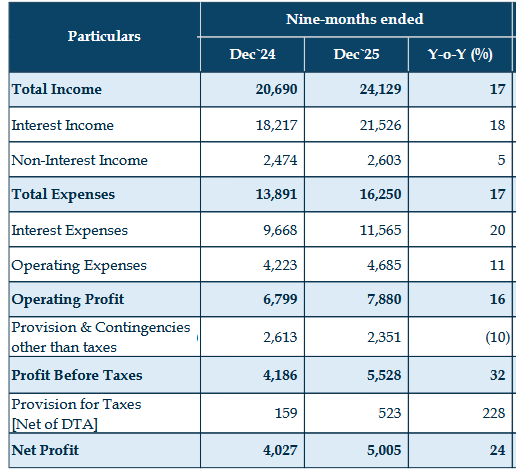

5. 9M-26: PAT up 24% & Net Interest Income up 17% YoY

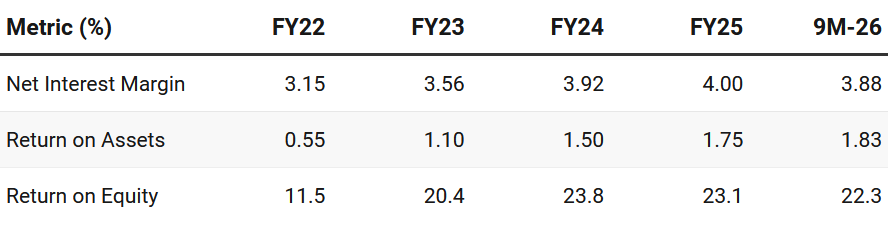

6. Business metrics: Strong Return ratios

ROE consistently above 20% — rare for PSU banks

7. Outlook: Mid-teen growth

7.1 Management Guidance

We are again going to keep a conservative guidance for NIM for the next year at 3.75%

For advances, we are keeping a guidance at around 17%. For deposits, we are keeping around 14%.

CASA will be maintained above 50%.

My guidance for ROA is 1.75%, which we would like to maintain for the next year.

GNPA has again seen a reduction, and has come down to 1.74%, but guidance is to maintain it below 2% and the credit cost to maintain below 1%.

The guidance, again for cost to income is to maintain it below 40%.

We have kept the guidance to maintain CRAR at around 18%.There is no immediate case for me to go and raise capital, number one

Overall share of RAM is 62:38 and our guidance has been to maintain it at 60:40 plus/minus 2%.

7.2 9M FY26 Performance vs FY26 Guidance

Maintaining guidance quarter-on-quarter

I am satisfied as a bank, as a management that whatever guidance at the beginning of the year for the last 12 to 15 months we have been talking about, we are maintaining and beating our own guidance quarter-on-quarter.

NIM — Outperformed — 3.88% vs 3.75 guidance

ROA — Outperformed — 1.83% vs 1.75 guidance

Advances Growth — Outperformed — 19.62% vs 17 guidance

Deposit Growth — Outperformed — 15% vs 14 guidance

Cost-to-Income — On-track — 37.29 vs below 40 guidance

Credit Cost — On-track — 0.97 vs below 1 guidance

GNPA — On-track — 1.6% vs below 2 guidance

CASA — Marginally behind — 49.54 vs above 50 guidance

CRAR — Below — 17.06 vs about 18 guidance

8. Valuation Analysis

8.1 Valuation Snapshot — Bank of Maharashtra

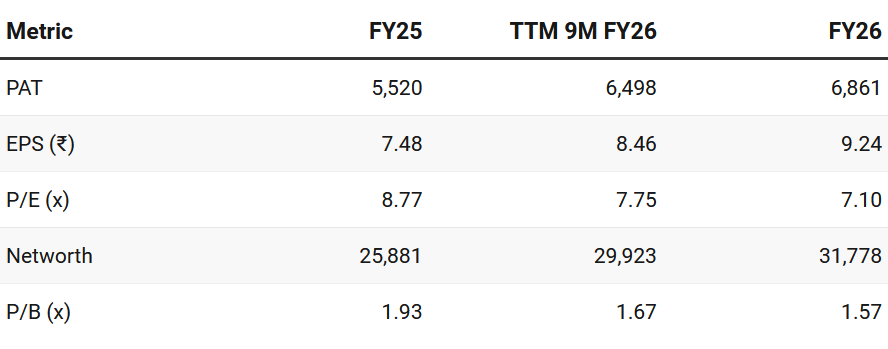

Current Market Price — ₹65.6

Market cap — ₹50,046.9 Cr

PAT growth of 24% in FY26 sustaining the growth of 9M-26

FY26E Net Worth = 9M-26 Net Worth + Q4 FY26E PAT

FY26E = 7.1× P/E & 1.6× P/B

Earnings Yield (1/PE) = ~14% — significantly above cost of equity, indicating undervaluation.

If FY26 guidance is delivered, there is scope for multiple re-rating based on FY26E numbers:

P/B of 1.75-2× (if the business of performance of FY26 continues into FY27)

This would imply valuation upside without requiring redefinition of fundamentals.

8.2 Opportunity at Current Valuation

NIM’s guidance is conservative — Profitability could surprise

Profitability could surprise on the upside as 3.75% NIM guidance is conservative and it has delivered NIM of 3.88 for 9M-26.

we are keeping a conservative number of 3.75% in terms of the NIM guidance.

Optionality from Re-rating

If current metrics hold, P/B could re-rate to ~1.75-2×.

Re-rating does not require exceptional performance —- continuity of 9M FY26 into FY27

Optionality from Sectoral Re-rating

PSU banks as a basket trade at a discount to intrinsic profitability.

Limited Downside

Valuations are undemanding — provide protection against a weak quarter

8.3 Risk at Current Valuation

Execution Dependence in H2

Loan & Advance growth slightly below run-rate in H1.

FY26 PAT assumption of ₹6,790 Cr requires no slippage on NIM or operating cost — though trajectory so far is solid.

Rate Cycle & Margin Sensitivity

NIM has held at 3.9%+ so far, but rate cuts and deposit repricing could reduce margins.

MAHABANK is confident of delivering on its 3.75% NIM guidance

This quarter also, we have, despite the rate cut impact coming in completeness in this quarter, we have been able to maintain our NIM above the guidance that we had shared in the beginning. And the Q3 and Q4, we have seen that with most of our deposit maturity profile, seeing the deposits getting repriced, we should see that further NIM contraction should not be.

PSU Discount May Persist

Despite strong metrics, PSU label may cap valuation multiples.

Previous coverage of MAHABANK

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

Hi,

Good to connect. I’m new to Substack after trading in my PPE and tools, and I now write about markets, risk, and the stories we tell ourselves to stay comfortable.

After the Close is less about prediction and more about process. Discipline over drama. Thinking clearly when the screens go dark. The writing is partly a way for me to slow things down and stay honest, especially in a space that rewards noise.

If you ever have a moment to look through it, I’d genuinely appreciate any feedback on the process. Good or bad is fine. I can handle it.

Cheers, Andrew