Balu Forge Industries: PAT growth of 171% & revenue growth of 71% for FY24 at a PE of 40

Guidance of 40-45% revenue growth in FY25 while maintaining EBIDTA margins of 23-24% with capex of 1.77X in place to support growth. BALUFORGE delivered ahead of its FY24 guidance of 40-45% revenue.

1. Manufacturing of crankshafts & forged components

baluindustries.com | NSE: BALUFORGE

Balu Forge Industries Ltd (BFIL) is one of the prominent companies in India for producing precision machined components.

It is engaged in the manufacturing of finished and semi-finished crankshafts and various other forged components and has a strong clientele comprising of 25+ OEM’s.

The Company boasts of a precision machining unit with a comprehensive product range which caters to customers across various industries such as automobiles, ships, locomotives, aerospace, defence, oil and gas, railway, marine, prototypes and others

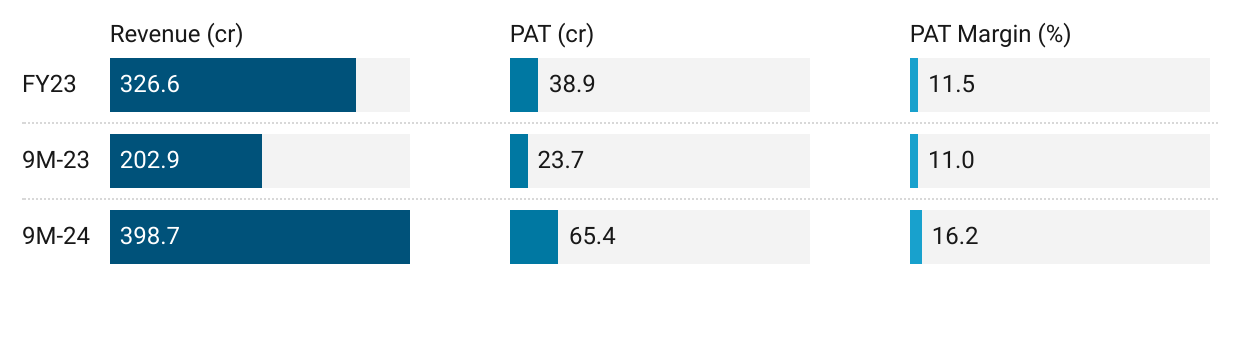

2. FY21-24: PAT CAGR of 131% & Revenue CAGR of 58%

3. FY23: PAT up 30% & Revenue up 14%

4. Strong 9M-24: PAT up 176% & Revenue up 97% YoY

5. Strong Q4-24: PAT up 86% & Revenue up 30% YoY

PAT up 148% & Revenue up 10% QoQ

6. Strong FY24: PAT up 141% & Revenue up 71% YoY

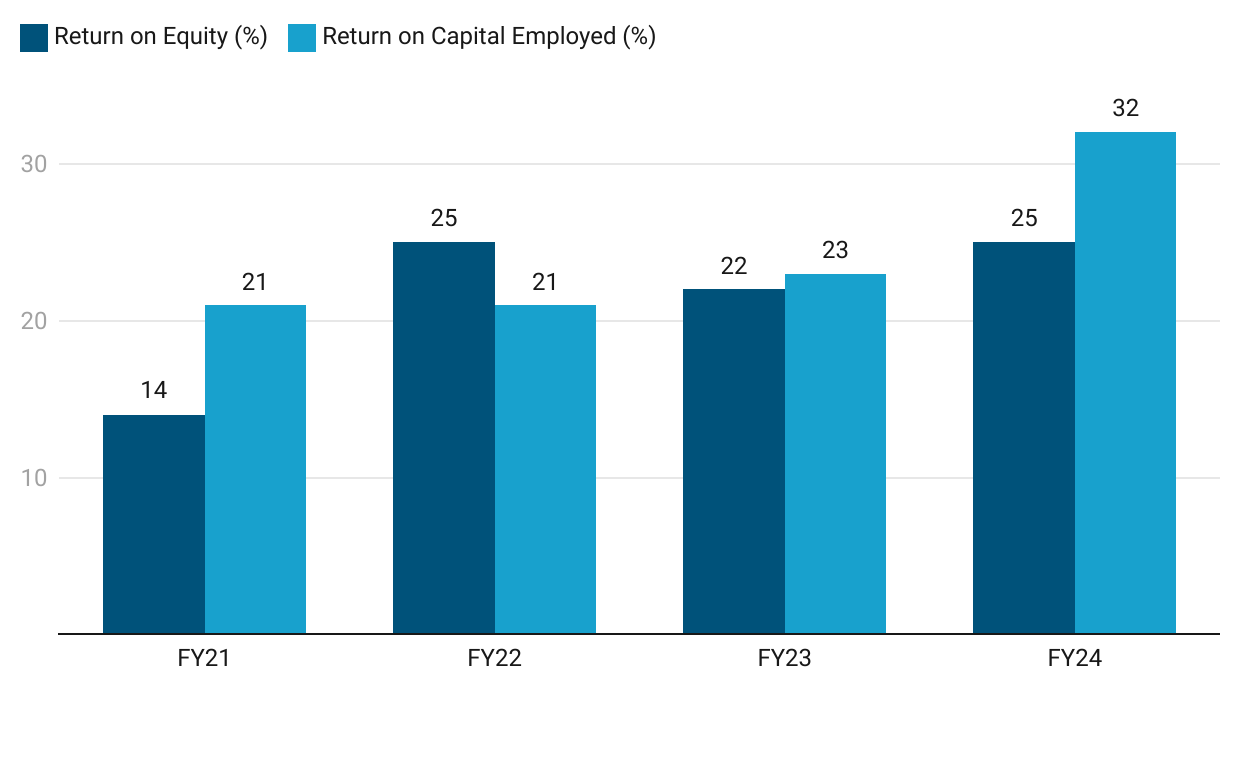

7. Business metrics: Strong & improving return ratios

8. Strong outlook: Revenue growth of 40-45%

i. FY25: Revenue growth of 40-45%

ii. FY25: EBITDA margin 23-24%

FY25 EBITDA margins to be sustained against the FY24 EBITDA margin of 23%

EBITDA margins are expected to be in the corridor of 23.0%-24.0% in the upcoming quarter on the back of increasing scale of operations and efficiencies thereon.

iii. FY25: Capacity expansion (1.8X) in place to support growth

On capability augmentation front, the development of our newly acquired Mercedes Benz unit is progressing well on expected timelines and commercialization from said plant are expected to commence from Q2 FY25.

The manufacturing capacity is poised to rise from 18,000 TPA to 32,000 TPA with the commencement of Mercedes Benz's machining plant.

9. PAT growth of 141% & Revenue growth of 71% in FY24 at a PE of 40

10. So Wait and Watch

If I hold the stock then one may continue holding on to BALUFORGE

Coverage of BALUFORGE was initiated after Q3-24 results. The investment thesis has not changed after a strong FY24. The delivery of a strong FY24 has increased confidence in the management to deliver a FY25 as per the guidance

FY24 Guidance: Revenue is expected to conservatively grow in the range of 40.0%-45.0% in FY24 over FY23, led by new customer addition in sectors like railway and defence.

BALUFORGE is in the middle of a strong run and has delivered sequential QoQ growth in PAT for the last six quarters starting from Q3-23

The capex coming online Q2-25 provides a roadmap for growth till FY26. The capacity expanding to 1.77X times FY24 capacity provides potential for the scale of the business to double.

11. Join the ride

If I am looking to enter BALUFORGE then

BALUFORGE has delivered PAT growth of 141% and revenue growth of 71% in FY24 at a PE of 40 which makes the valuations fully priced in the short term.

FY25 guidance of 40% revenue growth with 23-24% EBITDA margins at a PE of 40 which makes the valuations reasonable from a FY25 perspective

Previous coverage of BALUFORGE

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer