Australian Premium Solar H1 FY26 Results: PAT up 119%, On-track FY26 Guidance

Guidance of 75% FY26 growth. Capacity expansion on-track to support growth. Revenue CAGR of 68% for FY25-27. At very attractive valuations with a margin of safety

1. Solar Manufacturers & Solution Provider

australianpremiumsolar.co.in | NSE - SME: APS

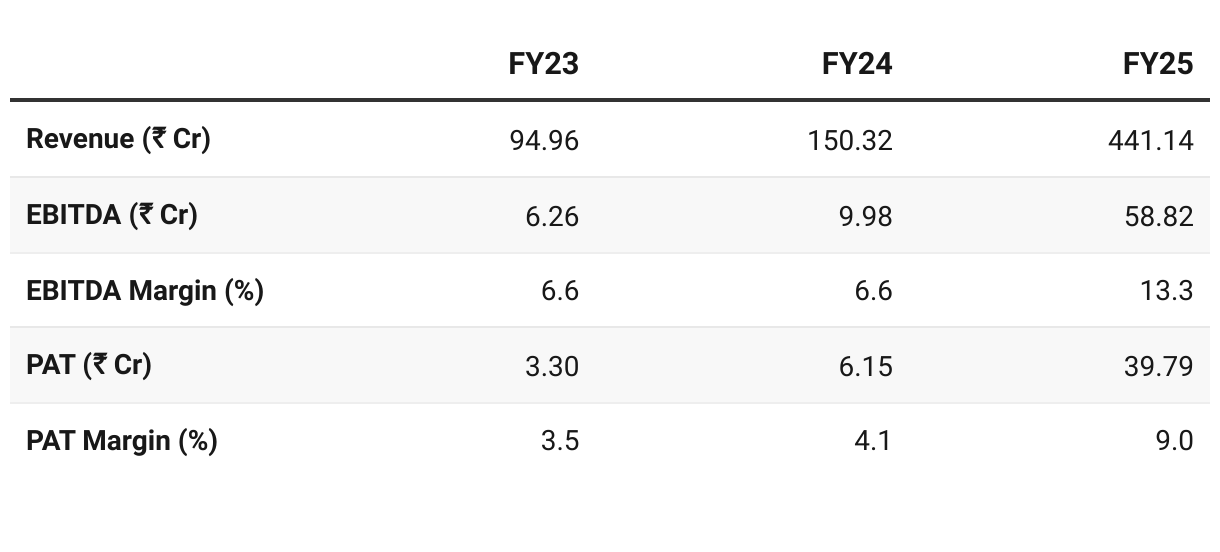

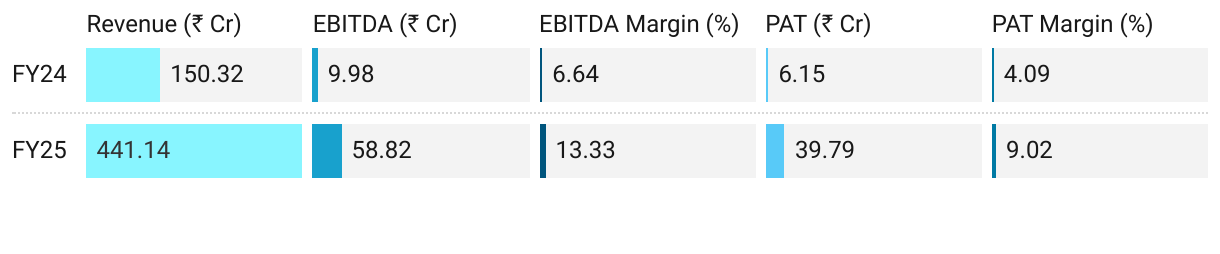

2. FY23–25: PAT CAGR of 247% & Revenue CAGR of 116%

3. FY25: PAT up 547% & Revenue up 193% YoY

Revenue Mix FY25:

Wholesale Distribution: (~52%) — 75+ distributors across 8 states.

Solar Pumps: (~34%)

Wins under PM-KUSUM, now a high-margin, scale driver.

Margins higher than rooftop retail because of subsidy-linked pricing & volumes

Retail Rooftop (Residential + C&I): (~14%)

Intentionally capped due to DCR (Domestic Content Requirement) solar cell supply constraints — management plans renewed focus on C&I rooftop from FY26.

Retail share shrank, which actually lifted blended margins, since retail was DCR-constrained and lower scale

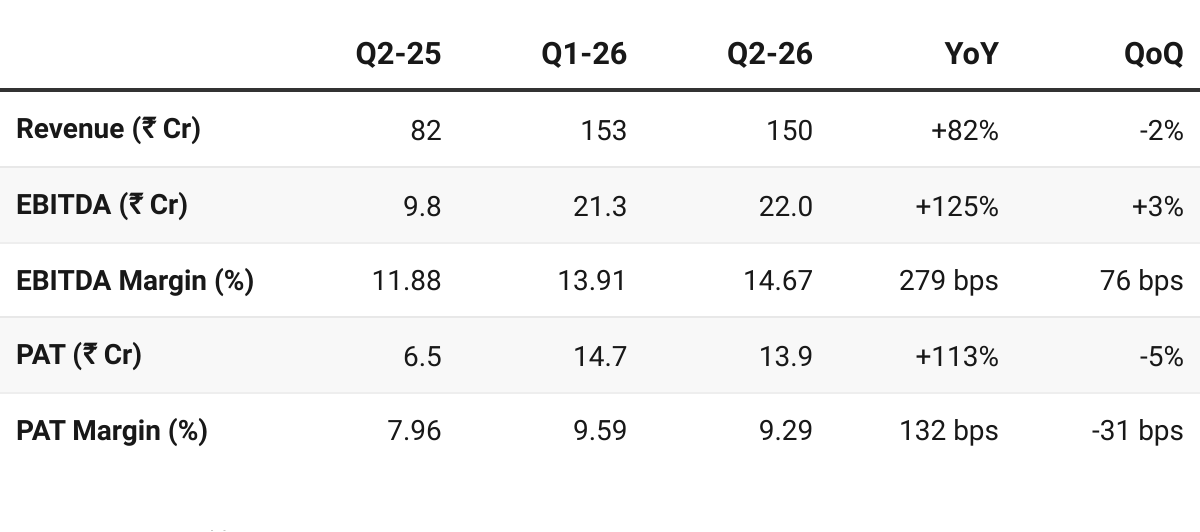

4. Q2 FY26: PAT up 113% & Revenue up 82% YoY

PAT down 5% & Revenue down 2% QoQ

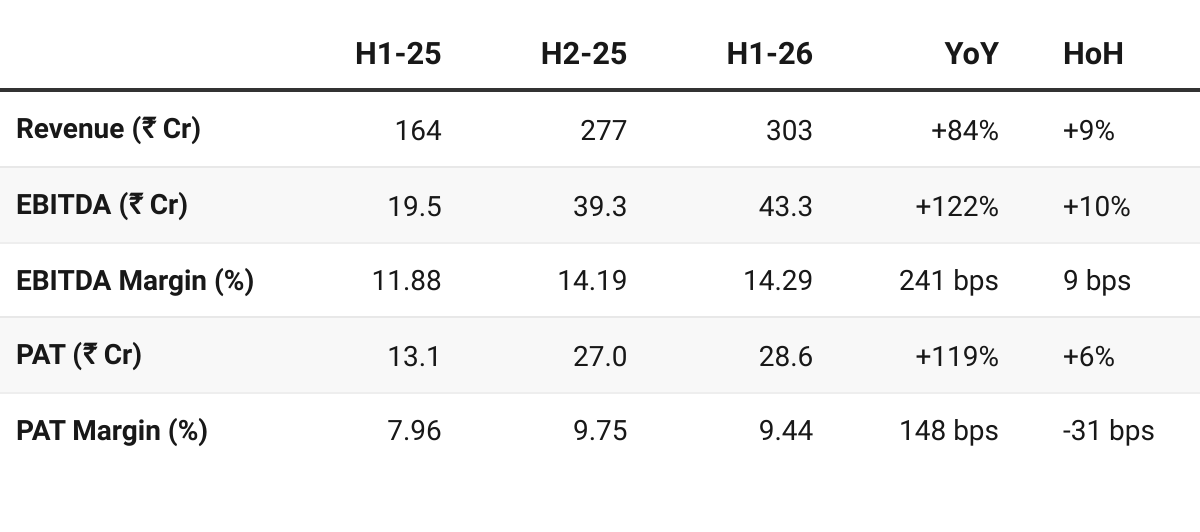

5. H1 FY26: PAT up 119% & Revenue up 84% YoY

PAT up 6% & Revenue up 9% HoH

Strong performance in H1 FY26, marked by consistent growth across our key business segments. Revenue grew 84% year-onyear to ₹302.93 crore, while EBITDA and PAT more than doubled to ₹43.28 crore and ₹28.60 crore respectively, underscoring our operational efficiency and execution excellence.

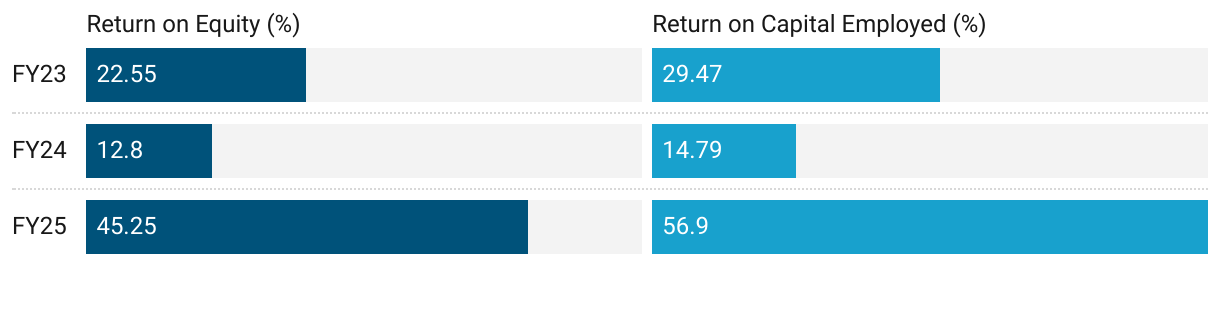

6. Business Metrics: Strong Return Ratios

Funds from IPO in muted FY24 return ratios

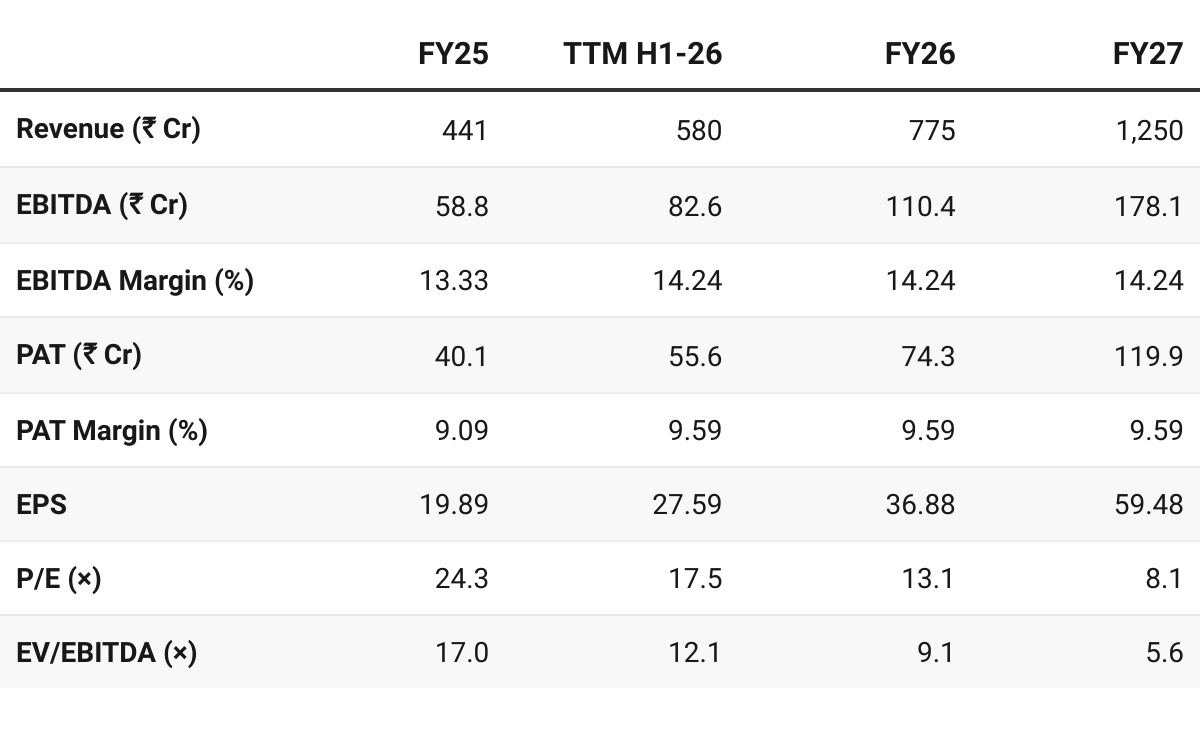

7. Outlook: Revenue Growth of 75% in FY26

7.1 Management Guidance — Australian Premium Solar

We are expecting is about probably 750 to 800 crores by the end of this FY26. And the margins, the EBITDA margin would be around in between probably 12.5 to 14% which will give a PAT of about 9-10% of them.

That's our conservative target, actually, to be precise.

FY2627 I'm talking about we expect turnover of 1,200 to 1,300 from APS then in 2027-2028, probably we expect standalone turnover of APS and its subsidiary like 100% subsidiary. It would be about in the range of 1,700 to 1,800 crore and there would be INR 600 to 700 crores of turnover from A plus solar cell in 2027-2028

APS Growth (as per guidance)

FY26

Expected revenue: ₹750–800 Cr (vs. ₹435 Cr in FY25 → ~75% growth).

Growth mainly from expansion in solar modules, pumps, EPC and retail/wholesale distribution.

No contribution yet from solar cells.

FY27 (2026–27)

Solar cell plant still under construction – so no revenue from solar cell operations.

APS core business (modules, EPC, pumps, inverters, distribution) projected turnover: ₹1,200–1,300 Cr.

FY28 (2027–28)

APS standalone (core business): ₹1,700–1,800 Cr turnover expected.

A+ Solar Cell (subsidiary), the new cell manufacturing vertical, expected to add ₹600–700 Cr.

This would be its first meaningful year of revenue after commissioning.

Total consolidated turnover: ~₹2,300–2,500 Cr.

6.2 H1 FY26 Performance vs FY26 Guidance

The commissioning of our 400 MW TopCon solar module line is a major milestone in our capacity expansion journey, taking our total module capacity to 800 MW.

Additionally, the expansion of our solar water pump portfolio and strengthening of the EPC vertical are expected to further diversify our revenue base and reinforce our growth trajectory.

These combined initiatives position APS to achieve its targeted 75% CAGR in revenue growth during FY25–26, supported by strong demand, product innovation, and our commitment to India’s renewable energy vision.

On-track FY26 guidance

Strong H1 vs FY26 Guidance:

Given pump installations are seasonally H2-heavy, guidance appears achievable.

Confirmation of FY26 guidance post H1-26 earnings: position APS to achieve its targeted 75% CAGR in revenue growth during FY25–26

Strong Margins:

EBITDA 14.3% and PAT 9.4% at upper end of guided bands → no margin pressure visible.

Capacity Expansion on-track

Oct-25: Commences Commercial Production of New 400 MW TopCon Solar Module Line — the first phase of APS’s planned capacity expansion

Additional 400 MW line scheduled to become operational by April 2026.

7. Valuation Analysis

7.1 Valuation Snapshot — Australian Premium Solar

CMP ₹483; Mcap ₹996.41 Cr;

Valuation does not consider FY28 as solar cell plant construction has not yet started

Attractive Forward Valuation:

APS looks attractive on TTM numbers, and multiples compress sharply as earnings scale.

Scope for valuation re-rating if FY26 guidance is delivered

Valuations are undemanding — provide flexibility to sustain periods where performance is not as per guidance

APS, is trading at a discount, reflecting its smaller scale and execution risks (capacity ramp-up, pump order execution, solar cell CapEx).

Looking attractive on FY26E and potentially undervalued on FY27E, provided execution stays on track. Multiples leave room for re-rating as APS transitions from a Gujarat-focused rooftop player to an integrated solar manufacturer.

7.2 Opportunities at Current Valuation

Attractive Forward Valuation: Trading at a discount, well below peers. Scope for re-rating if growth sustains.

Growth Visibility: Pathway to growth is attractive. From ₹435 Cr in FY25 to ₹2,300–2,500 Cr by FY28

Tailwinds — Policy & Government Support

DCR mandates, rooftop subsidies, and PM-KUSUM program create protected domestic market.

Eligible for 25–30% CapEx subsidy on new solar cell line.

7.3 Risks at Current Valuation

Microcap Risk: May not grow into a small-cap; Illiquid, SME-listed; entry/exit difficult

Scale vs Valuation Gap: While valuations look cheap, discount may persist until APS delivers on FY26 and FY27 guidance

Execution Risk: Subsequent 400 MW phase critical to achieving FY26–27 growth.

CapEx Burden: ₹800–900 Cr for solar cell project – funding mix of debt + equity may dilute returns or strain balance sheet if delayed.

Competitive Intensity: Larger peers (Adani, Waaree, Vikram) with 5–10 GW+ capacity could pressure pricing/market share.

Policy Dependence: Heavy reliance on government programs (PM-KUSUM, rooftop subsidies, DCR rules) — policy changes could impact demand/margins.

Previous Coverage of APS

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer