Angel One: PAT up 26% & Revenue up 42% in FY24 at a PE of 21

FY24 results impacted by margin contraction despite strong top-line growth. The outlook for FY25 will continue with a strong top-line growth and margin contraction to dent the bottom-line growth

1. Largest listed broking house in India

angelone.in | NSE: ANGELONE

23.1% share in India’s incremental demat accounts in Q4 ‘24.

Angel One held a 14.7 percent share of demat accounts in India in the Jan-March compared with 12 percent a year earlier.

Q4:24: we clocked our highest ever quarterly gross client acquisition at 2.9 million

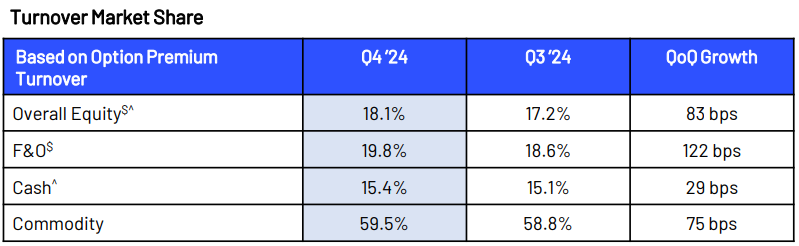

Business Segments

2. FY19-24: PAT CAGR of 90% & Revenue CAGR of 56%

3. 9M-24: PAT up 26% & Revenue up 33% YoY

4. Q3-24: PAT up 27% & Revenue up 63% YoY

PAT up 31% & Revenue up 28% YoY

5. FY-24: PAT up 26% & Revenue up 42% YoY

Improvement in top-line growth

A year of margin contraction

6. Strong and consistent return ratios

7. Outlook: PAT growth slow down to continue from FY24 into FY25

i. FY25: Top-line growth to remain strong

continue to see very strong growth coming ahead for the company but that also means that the working capital requirements for Angel one have now shot

ANGELONE is undertaking a change in its business model, which will incrementally drive the focus towards gaining market share in the cash segment, along with strong growth in distribution revenues, over the next 2-3 years. Growth in the distribution segment will be driven by loans, insurance and a few other products

ii. FY25: Bottom line to lag top-line growth. Margin pressure to continue

IPL sponsorship expenses of nearly 120 crores is what the company expects to recognize in the first quarter and as a result there could be an impact on the margins in the first quarter

Guided for an EBITDA margin of almost 45 to 47% but additionally they expect one and a half percent impact to come through on the margins for from scaling up of their AMC as well as the wealth management business and therefore the management has now guided for EBITDA margins between 42 to 45%

Angel Q4FY24 Results: Management Expects 1.5% Impact From Scaling UP AMC & Wealth Management

8. PAT growth of 26% & revenue growth of 42% in FY-24 for a PE of 21

9. So Wait and Watch

If I hold the stock then one may evaluate holding on to ANGELONE

Coverage of ANGELONE was initiated after Q4-23 results. The investment thesis for top-line has not changed in FY24. However, concerns have started emerging on the bottom line growth, due to margin contraction seen in FY24.

From an underlying business perspective ANGELONE is gaining market share which is a big positive for the business

The bottom-line performance in FY-24 is a big red flag which one needs to watch out for. If the bottom-line growth does not keep pace with top-line then it would be difficult to justify holding on to ANGELONE

10. Or, join the ride

If I am looking to enter ANGELONE then

ANGELONE has delivered 42% growth in top-line and 26% growth in PAT in FY24 at a PE of 21 which makes the valuations fair from a short term perspective and does not provide opportunities in the short term.

The outlook for margin contraction in Q1-25 followed by weaker margin profile in FY25 does not make ANGELONE look interesting in the short term. If the margin contraction is handled well in FY25, then the top-line growth could create interesting opportunities in ANGELONE.

Previous coverage of ANGELONE

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer

Any views on impact of Sebi transaction charge guidelines from Oct 1

https://www.cnbctv18.com/market/sebi-circular-transaction-charges-blow-discount-broking-angel-one-motilal-oswal-bse-share-price-19436704.htm