Zelio E-Mobility FY26 Result: PAT up 77%, 75%+ Growth Guidance

Guiding 75-80% structural revenue growth. FY26 delivered ahead of guidance. Zelio looks cheap on forward valuations. Risk if FY27 not delivered as per guidance

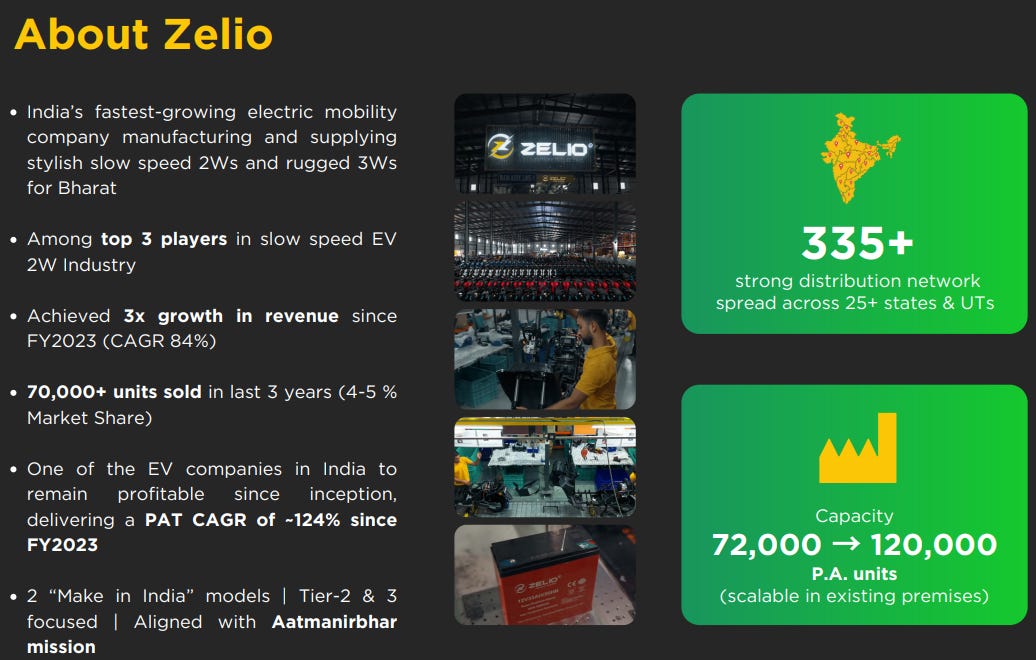

1. EV manufacturer/assembler — 2Ws & 3Ws

zelioebikes.com | BSE - SME: 544563

Core business is low-speed electric scooters

Affordable EVs with no licence, no registration, low maintenance and low running cost.

Low-speed e-scooters are the main revenue driver;

Expanding into high-speed scooters and electric 3-wheelers/e-rickshaws.

Manufacturing footprint: started with Hisar/Ladwa plant;

Expanding through Odisha/Cuttack, Coimbatore and Patan plants to serve East, South and 3W/chassis demand.

Sells through a dealer network across 25+ states, with management targeting 550+ dealers in FY27.

Dealer-led service network supported by company service engineers

Spare-parts availability through Zelio Auto Components, its wholly owned subsidiary.

Business model is profitable growth, not subsidy-led growth

Profitable since inception — growth has come without heavy subsidy dependence.

Strategic focus: become an organized brand in the fragmented low-speed EV segment, increase localization from ~30% toward 80%, and scale nationally while maintaining margins.

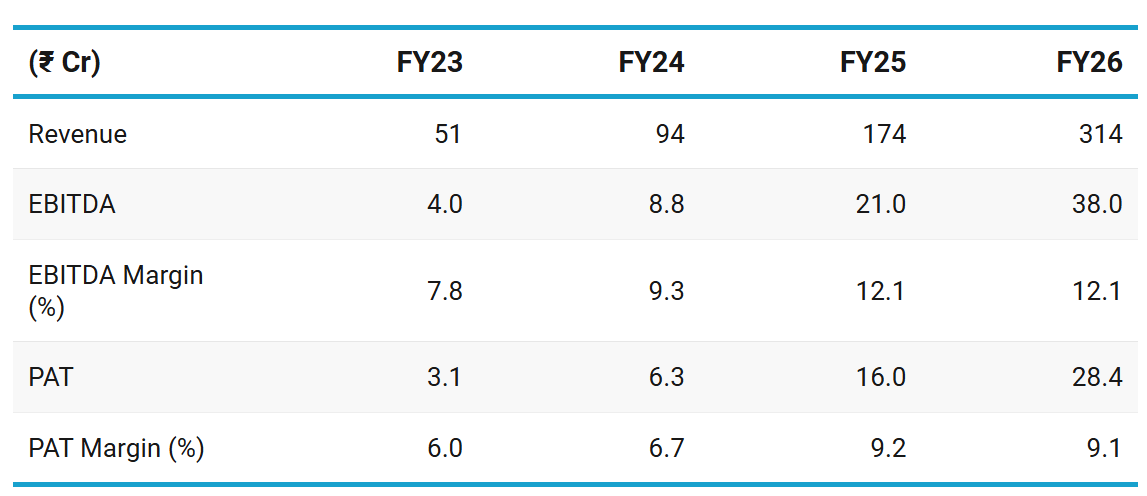

2. FY23-26: PAT up 110% & Revenue up 83% CAGR

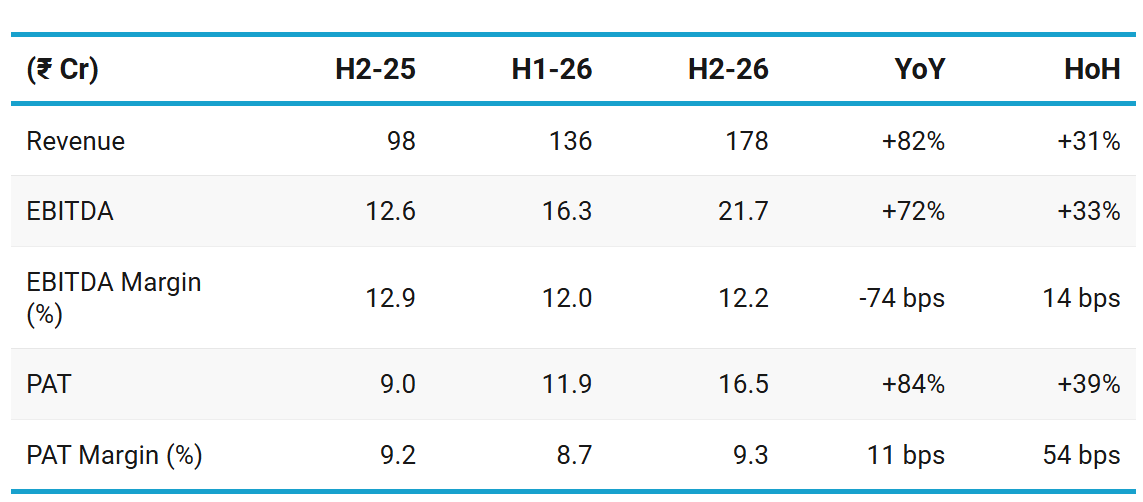

3. H2 FY26: PAT up 84% & Revenue up 82% YoY

PAT up 39% & Revenue up 31% HoH

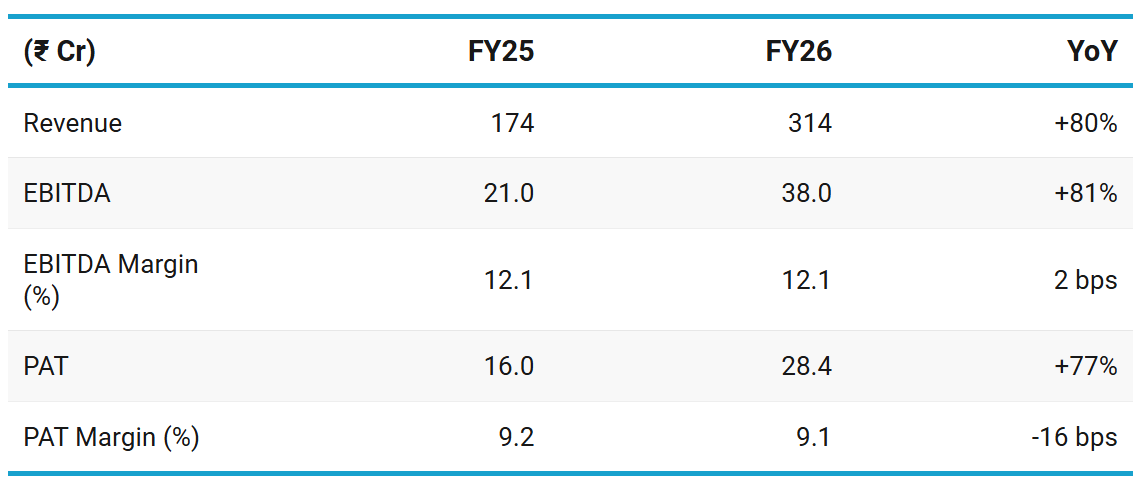

4. FY26: PAT up 77% & Revenue up 80% YoY

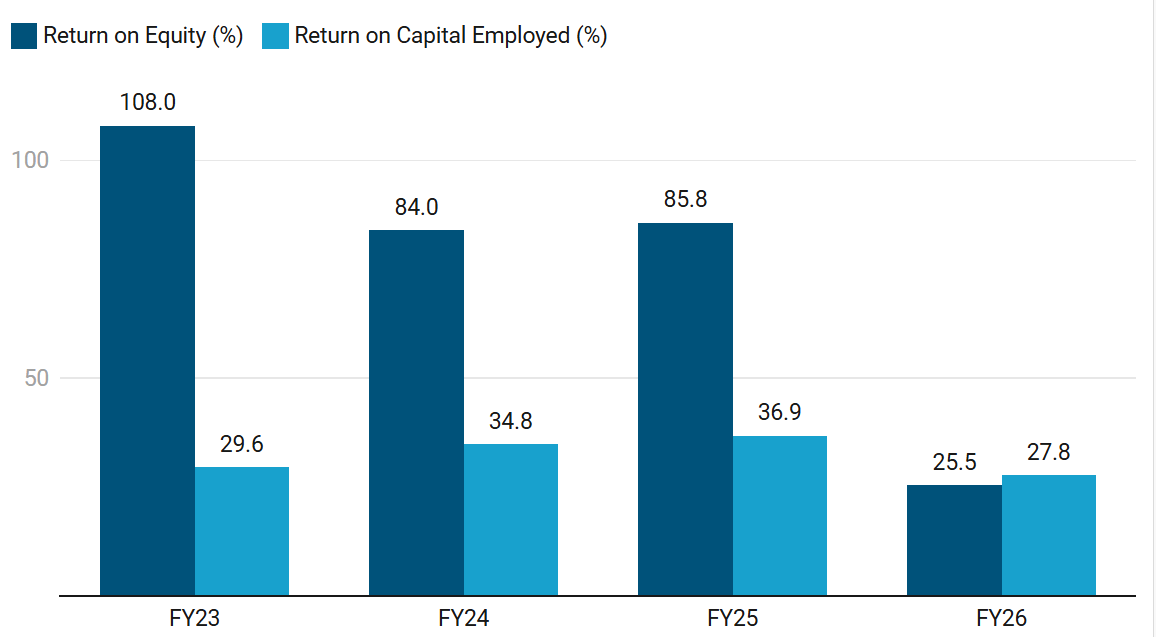

5. Business Metrics: Stable Return Ratios

FY26 ROE fell compared with FY25 because IPO equity increased the equity base.

On an increased capital base FY26 ROCE remained strong at ~28% — business generates attractive operating returns on capital.

6. Outlook: Growing at 75-80%+ CAGR

6.1 FY27 Guidance

I am committed to sustaining 75% to 80% year-on-year revenue growth as our structural trajectory. Not a one-time event, but a repeatable engine.

Sustaining 75% to 80% from here on a larger foundation, wider distribution, and a diversified portfolio is a number grounded in real assets, real capacity, and a market opportunity that is still largely untapped.

This year we will definitely acquire more than 10% share in the market.

Within 2 to 3 years, we will acquire more than 20%-30% of the EV market.

We are launching two high-speed EV models, targeting a 550+ dealer network across 25+ states with focused activation in South India and Northeast.

FY27; is the first full year of simultaneous East India and South India revenue from Cuttack and Coimbatore.

We are targeting more than 125,000 units scale for this year.

6.2 FY26 Performance vs FY26 Guidance

FY26 execution was strong vs guidance — financials beat, 2W volume beat, 3W ramp missed.

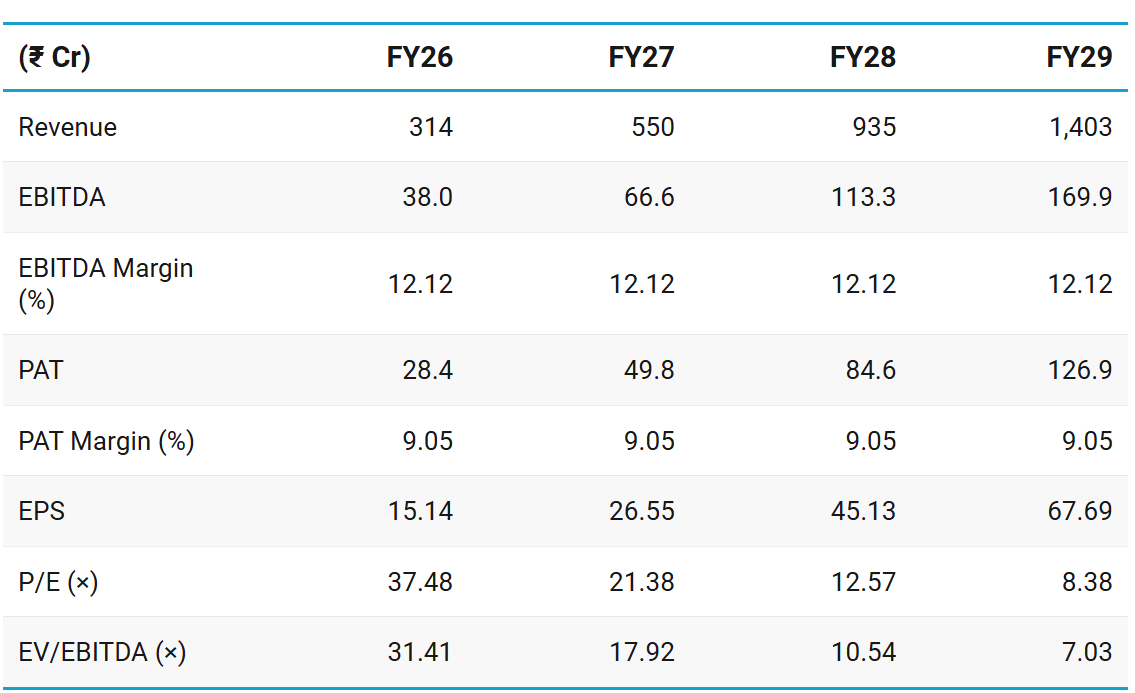

Revenue: ₹313.68 Cr vs ₹260-280 Cr guidance — Beat

Margin: “Constant and same” vs H1 level

FY26 EBITDA & PAT margins ahead of H1 FY26 margins

2W Units: FY26 target >60,000 vs 70,000+ delivered — Beat

3W Units: FY26 target 1,000 units vs 800 units delivered — Miss

7. Valuation Analysis — Zelio E-Mobility

7.1 Valuation Snapshot

Current Market Price — ₹567.45

Market cap — ₹ 1,200.16 Cr

Assumptions

70% growth till FY28

FY29 growth of 50% growth is illustrative to show how the numbers will look if 75%+ structural growth plays out

Its too early to consider FY29 as part of any investment decision

FY26 valuation is rich — 38× trailing P/E is acceptable only if FY27–FY28 growth is very strong and margins hold.

If guidance is met, valuation becomes much more reasonable. The stock moves from expensive on FY26 to fair-to-reasonable on FY27.

The real investment case is not FY27 alone, but FY27 + FY28 compounding.

7.2 Opportunities at Current Valuation

The opportunity is that the market may still be underestimating the size of the FY28 business if FY27 execution is delivered.

Valuation compression

If FY27 guidance is delivered, the stock becomes ~23–24x FY27E PAT; if FY28 growth remains strong, valuation can look cheap in hindsight.

Capacity-led growth without immediate large capex pressure

Capacity increased from 72,000 units to 240,000 units.

FY27 guidance is >125,000 units, which means the company is not yet close to full capacity utilisation.

There is visible capacity headroom till FY28 if the structural growth of 75-80% plays out.

Low-speed EV category leadership

Zelio is focused on low-speed EV scooters: no license, no registration, no mandatory insurance, and pricing around ₹50,000–75,000.

Management says this segment is 8–10 lakh units annually, around 40–45% of EV 2W volumes, and growing 20–25% per annum.

Most EV attention is on Ola, Ather, TVS, Bajaj high-speed scooters. Zelio is playing a different market: Bharat mobility, students, homemakers, senior citizens, gig workers and Tier-2/Tier-3 users.

If Zelio becomes the organized leader in low-speed EVs, it can get a premium. The market may value it not as a small assembler, but as a profitable category leader.

Market-share expansion

H1 FY26 call management spoke of 4–5% market share and a 5–6% target.

In the FY26 call, tone became more aggressive: FY27 volumes are expected to cross 10% market share, with management talking about 20–30% share over 2–3 years.

New geography monetisation

FY27 is the first year where the company expects simultaneous contribution from:

Ladwa / Hisar — North and West India

Cuttack / Odisha East and Northeast India

Coimbatore / Tamil Nadu South India

Patan / Haryana 3W and chassis

Cuttack reduces transportation cost and delivery timelines for East/Northeast,

Coimbatore opens South India as a dedicated revenue corridor.

Product-mix expansion

Zelio is moving from mostly low-speed 2W into:

High-speed EV models — Brand expansion + higher ASP potential

3W / e-rickshaw — Higher ticket size, new dealer category

Auto Components Supply-chain control + spare parts availability

Management said it is launching two high-speed EV models and scaling the 3W business through the Patan plant.

8.3 Risks at Current Valuation

The risk is that the stock is already pricing in very clean FY27 execution.

Valuation risk: FY27 has to deliver

If FY27 revenue comes below guidance, valuation does not leave much protection.

If FY27 lands below ₹500 Cr, the stock remains expensive even after one more year of growth.

Management has raised the bar sharply

Management is now targeting >125,000 units, 550+ dealers, and 75–80% YoY revenue growth as a “structural trajectory.” That is a very high bar after already growing 81.8% in FY26.

They have built capacity, but the market will now demand proof of dealer productivity, service quality, working capital control and repeat demand.

Cash-flow risk: profit did not convert into cash in FY26

FY26 consolidated PAT was ₹28.39 Cr, but consolidated operating cash flow was negative ₹11.20 Cr. The drag came mainly from working capital, increases in inventory, short-term loans and advances and other current assets

If growth requires continued supplier advances and inventory build-up, accounting profits may keep rising while free cash flow remains weak.

3-wheeler ramp risk

3W is being presented as a second growth engine, but actual scale is still low. If 3W ramp is further delayed, FY27/FY28 upside becomes more dependent on low-speed 2W alone.

Low-speed EV data opacity risk

Slow-speed EVs do not appear in Vahan registration data because they do not require registration. Management clarified this when an investor questioned the mismatch between Vahan data and reported sales.

investors have limited independent monthly data to verify volumes. This makes trust in management disclosures more important.

Import/localisation execution risk

Management earlier said the company was around 30% localised and wanted to move toward 80% localisation.

Localisation can improve margins, but execution is not automatic. Until localisation is proven, Zelio remains exposed to imported components, supply-chain disruption, currency movement and quality consistency.

Competition risk

Management argues that low-speed EV is a large Bharat market and that Zelio can gain share.

But the same attractiveness can invite larger OEMs, regional assemblers and aggressive pricing.

Management itself discussed the possibility of larger players like Bajaj, Hero and TVS entering if the market becomes big enough.

Current margins assume Zelio can grow without heavy discounting. If competition intensifies, the company may have to choose between volume growth and margin protection.

Help your group stay ahead. Share now!

Don’t like what you are reading? Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer