Zaggle Prepaid Ocean Services: PAT up 123% & Revenue up 77% in 9M-25 at a PE of 58

Guidance of 58-63% revenue growth in FY26. Margin from 9-11% to 15-16% in next 3-4 years. 50% revenue CAGR guidance for next 3 years. Acquisitions to add to the organic growth in FY26.

1. Why is ZAGGLE interesting

zaggle.in | NSE: ZAGGLE

ZAGGLE sees strong tailwinds and 50% organic revenue CAGR for the next 2-3 years with strong margin expansion. Inorganic growth on top of the organic growth expected. Rich valuations in the short term, do not fully capture the opportunity over the longer term. 2. SaaS-based fintech: Spend Management company

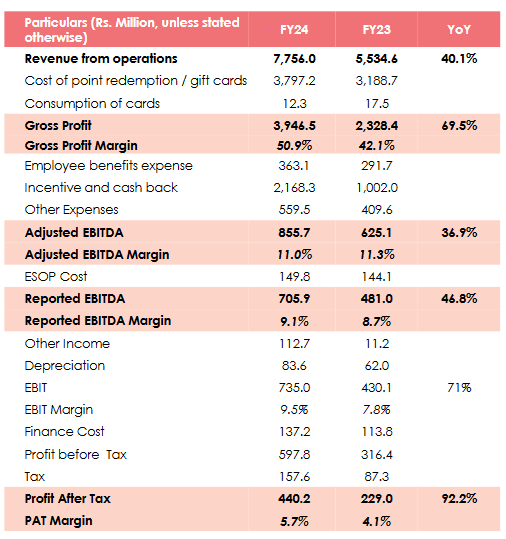

3. FY20-24: PAT CAGR of 9% & Revenue CAGR of 52%

4. FY24: PAT up 92% & Revenue up 40%

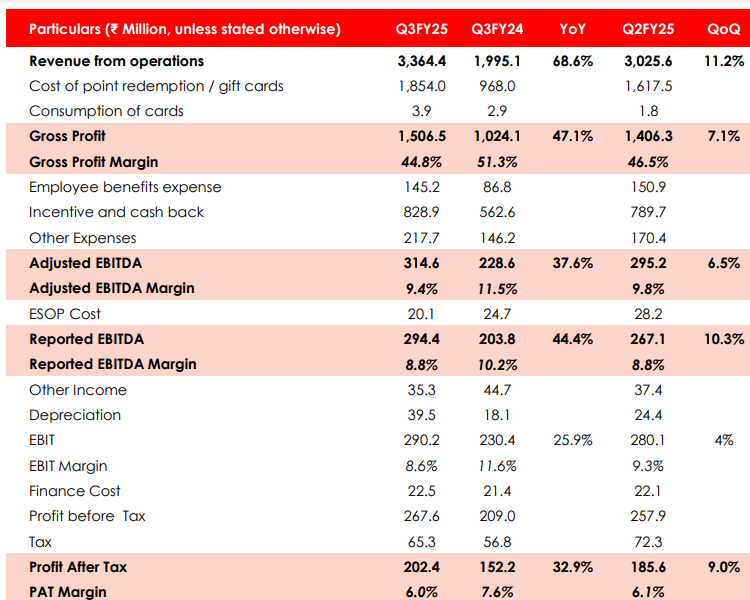

5. Strong Q3-25: PAT up 33% & Revenue up 69% YoY

PAT up 9% & Revenue up 11% QoQ

6. Strong 9M-25: PAT up 123% & Revenue up 77% YoY

7. Strong outlook: Organic growth of 50-55%

See Tremendous Tailwinds And 50% Growth For Next 2 To 3 Years: Zaggle Prepaid Ocean Services

i. FY25: Revenue growth of 58-63%

FY25: We are upping our guidance that we possibly will be able to do in the range of about 58 to 63% and this also may be a little bit outdone if the trends are to be seen.

ii. FY26: Organic Revenue growth of more than 23-27% with additional inorganic growth

FY25 revenue of Rs 1225-1264 cr based on 58-63% revenue growth will grow to Rs 1550 cr by FY26. This implies a revenue growth of 23-27% in FY26. However ZAGGLE is claiming it will more than double on FY24 base in FY26 with details expected in the coming quarter.

Old guidance FY24-26: We remain very confident of doubling our FY24 revenues, which were Rs. 775 crores, to double in the next two years.

Latest indications: More than double of FY24 in FY26. Expecting exact details in in the next quarters

iii. Improvement in margins

FY25: We have guided about 9% to 10% EBITDA margin for this year

FY26: We had said that maybe 10% to 11% next year.

FY27: But post that, there will be significant expansion as both these acquisitions which are in play would come into action and the blended margins

would be much, much more higher.

We will reach about 15 to 16% EBITDA in the next 3 to 4 years.

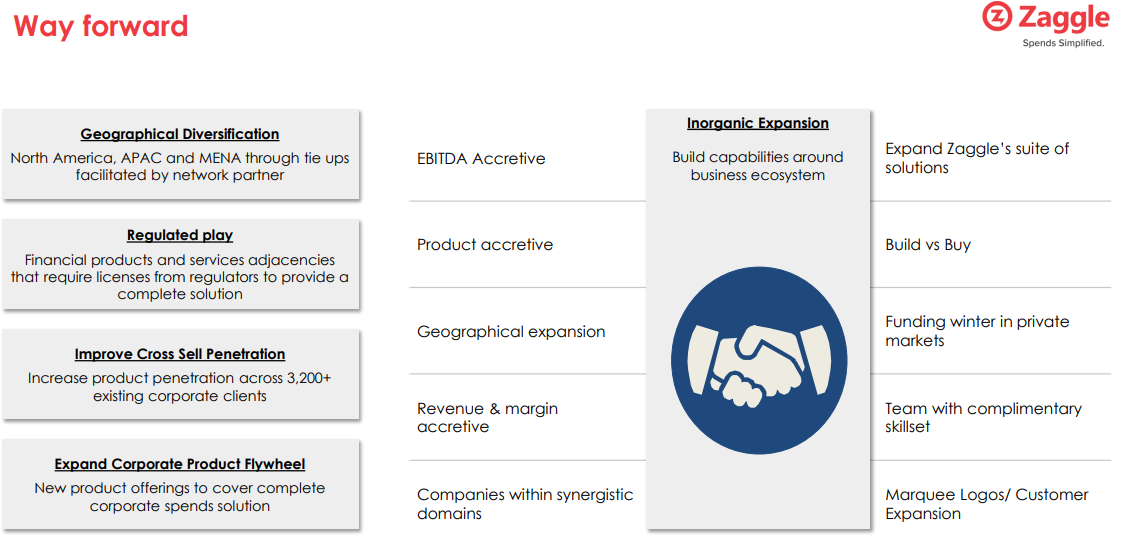

iv. Inorganic growth over and above the organic growth guidance

We are currently very pleased to also inform that we are currently evaluating five targets in the spend management and adjacent space, such as merchant card software, payment infrastructure, etc. Out of this, two are at advanced stages and moving towards completion at a fast pace. We are looking forward to, you know, a closure of all these transactions, you know, in this calendar year.

8. PAT growth of 123% & Revenue growth of 77% in 9M-25 at a PE of 58

9. Hold?

If I hold the stock then one may continue holding on to ZAGGLE

Based on 9M-25 performance, ZAGGLE is on track to deliver as per the FY25 guidance of 58-63% revenue growth and then deliver FY26 ahead of its old guidance of doubling on FY24 base.

EBITDA margin expansion expected from 9-11% to 15-16% in the next 3 to 4 years

Have headroom for growth for next 3-4 years without needing money.

So, sir, we have raised about INR490 crores from the IPO and it is sufficient for our next three years to four years of growth. It would -- if unless and until we go ahead and do an inorganic acquisition, where we might require some external funding. We do not see any signs of needing money in the next two to three to maybe let's say three to four years.

Business momentum is strong and expected to continue into the rest of the year

ZAGGLE management is confident of growth

I think we do not see any specific head winds for our business. We see more and more confidence growing with corporate customers and banks to work with us as a profitable listed entity.

10. Buy?

If I am looking to enter ZAGGLE then

ZAGGLE has delivered PAT growth of 123% and revenue growth of 77% in H1-25 at a PE of 58 which makes the valuations fully valued over the short term.

ZAGGLE is guiding for revenue growth of 58-63% in FY-25 at a PE of 58 which makes the valuations fully valued from a FY25 perspective.

Based on expected improvement of the old guidance of Rs 1550 cr revenue in FY26, opportunity could emerge from an FY26 perspective, but one needs to see the actual guidance given for FY26 in the Q4-25 earnings call.

With an FY24-27 outlook for 50% top-line CAGR supported by organic growth and EBITDA margin expansion from 9-11% to 15-16% in the next 3 to 4 years a PE of 58 can be sustained over the longer term

At a 58 PE, the margin of safety in ZAGGLE is quite low to sustain even a single weak quarter. Additionally, delays in execution of the inorganic growth opportunities will be a big negative for ZAGGLE.

Previous coverage of ZAGGLE

Don’t like what you are reading? Will do better. Let us know at hi@moneymuscle.in

Don’t miss reading our Disclaimer